PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911747

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911747

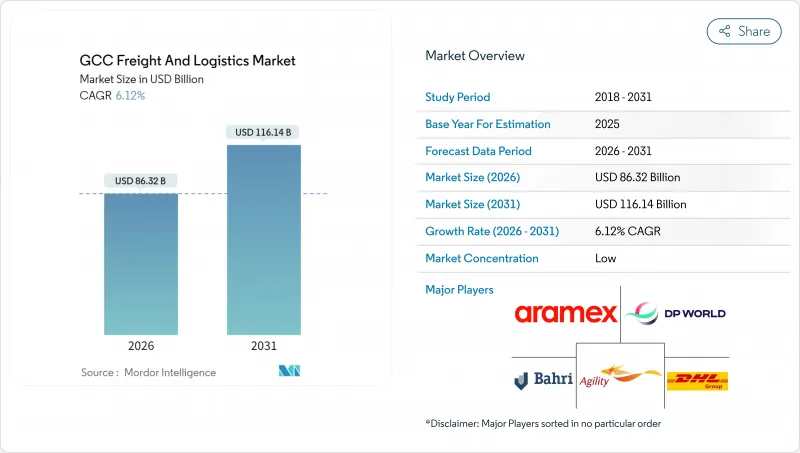

GCC Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The GCC freight and logistics market size in 2026 is estimated at USD 86.32 billion, growing from 2025 value of USD 81.34 billion with 2031 projections showing USD 116.14 billion, growing at 6.12% CAGR over 2026-2031.

Solid public-sector funding for multimodal corridors, widespread digitalization of customs and inventory processes, and voluntary carbon-neutral freight programs are translating national diversification agendas into consistent logistics spending. Deep-water port expansions, airport cargo village upgrades, and warehouse automation projects are widening service portfolios, while the region's geographic midpoint between Asia, Europe, and Africa sustains transshipment demand. At the same time, retail e-commerce growth, free-zone manufacturing relocations, and autonomous delivery pilots are shifting volume mixes toward higher-margin courier, express, and parcel (CEP) activities. Competitive intensity is rising as recent megadeals create integrated one-stop providers, yet fragmentation persists in several specialty niches, leaving room for focused regional operators.

GCC Freight And Logistics Market Trends and Insights

Vision-2030 Infrastructure Corridors Drive Multimodal Connectivity

Saudi Arabia's Vision 2030 blueprint is turning green-field corridors into operational gateways that mesh ports, airports, and logistics zones. Construction of the USD 800 million Port of Neom container terminal, scheduled for 2025, coupled with King Abdulaziz Port's USD 1.86 billion capacity uplift to 7.5 million TEU, introduces direct competition to legacy hubs such as Jebel Ali. The LOGISTI digital single window, launched in March 2024, further compresses dwell times by unifying customs documentation. As shippers reroute intra-Gulf cargo through these corridors, network effects improve back-haul utilization and pull warehouse developers toward adjacent industrial plots. Spillover benefits reach the wider GCC freight and logistics market by lowering total landed costs and enhancing schedule reliability.

E-commerce Boom Accelerates Last-Mile Innovation

Regional e-commerce revenue is poised to touch USD 49 billion in 2025, mandating dense fulfilment footprints and technology-enabled drop-density optimization. Warehouse rents in Dubai Industrial Park and JAFZA have trended upward as operators co-locate near air and seaport clearance points to compress order-to-delivery cycles. FedEx's USD 350 million automated sort hub at Dubai World Central-rated for 9,000 parcels per hour and equipped with cold-chain lanes and on-site EV charging-signals logistics providers' dual focus on scalability and sustainability. Autonomous drones deployed by dnata for cycle-counting and yard surveillance underscore the operational maturity of unmanned systems in desert climates. Cross-border parcel growth outpaces domestic flows, elevating international CEP demand within the GCC freight and logistics market.

Fragmented Addressing Systems Constrain E-commerce Logistics

Inconsistent house-numbering and reliance on landmarks complicate last-mile route planning, elevate failed-delivery ratios, and push per-parcel costs higher. Cash-on-delivery preferences add another layer of friction, forcing CEP operators to manage reverse cash flows and higher non-delivery returns. Each country's digital mapping initiative remains siloed, preventing cross-border harmonization that large marketplaces need for scale. The drag is most acute in the Saudi and Qatari e-commerce corridors, where address validation errors lengthen delivery cycles and inflate customer-service workloads. Progress toward unified geocoding would unlock latent efficiencies across the GCC freight and logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Integrated Free-Zone Value Propositions Attract Manufacturing

- Manufacturing Proximity to Ports Reshapes Freight Flows

- Labor Shortages Drive Automation Investments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing retained 26.74% of 2025 revenue, its dominance fueled by sovereign industrialization funds, tariff-free raw-material access, and proximity to emerging consumer clusters. Automotive assembly lines, modular housing fabrication plants, and biopharma fill-finish suites necessitate synchronized inbound sub-component deliveries and validated outbound documentation, creating sticky multi-year contracts for logistics service providers. Oil, gas, mining, and quarrying remain high-volume clients, though their proportional contribution inches downward as non-hydrocarbon sectors rise. Construction demand stays resilient, with giga-projects such as NEOM, Lusail, and Etihad Railway driving heavy-lift equipment flows and just-in-time cement batching. Agriculture and aquaculture initiatives, anchored by food-security policies, introduce specialized reefer moves and sanitary-phytosanitary protocols into the GCC freight and logistics market.

Wholesale and retail trade, though smaller at baseline, is forecast to post a nimble 6.47% CAGR (2026-2031), mirroring omnichannel store rollouts and a millennial-led shift toward doorstep delivery. Rapid-fire fashion cycles, consumer electronics launches, and grocery dark-store models amplify SKU volatility and compress cut-off windows, advantaging providers that integrate pick-to-light systems and cycle-counting drones. Ford's Dubai parts campus demonstrates how after-sales support centers now function as regional omni-hubs, extending same-day reach across multiple countries via shared air-road corridors. Healthcare and personal-care brands demand GDP-compliant cold chains and validated data loggers, nudging operators toward pharma lane certification. Technology hardware producers value bonded buffers in free zones that let them defer duty and re-export seamlessly. The GCC freight and logistics industry therefore pivots from monolithic bulk flows to fragmented, high-touch consignments that reward agility and data transparency.

Freight transport retained a commanding 56.88% slice of the GCC freight and logistics market in 2025, anchored by bulk petrochemical exports, containerized consumer imports, and contract hauling for mega-projects. Yet CEP revenues, buoyed by double-digit shopping-cart growth and increasingly sophisticated fulfilment promises, are projected to grow at a CAGR of 7.11% between 2026-2031, outstripping every other functional silo. Warehouse and storage services cater to manufacturers and retailers seeking scalable overflow space; fully 85.02% of sites remain ambient, but pharmaceutical regulation and chilled grocery demand are pushing operators to earmark incremental capex for insulated panels, ammonia chillers, and validated temperature sensors. Freight forwarding intermediaries maintain a 53.77% revenue share for sea and inland waterways, leveraging vessel space-procurement leverage and door-to-door documentation competencies, yet are rapidly adopting rate-management APIs and cargo-visibility platforms. Leading providers increasingly market end-to-end bundles that knit transport, storage, and regulatory orchestration into a single fee, raising switching barriers for enterprise shippers.

The GCC freight and logistics market size tied to CEP traffic is set to expand as cross-border checkout modules, low-value-duty exemptions, and automated de minimis calculations make foreign sellers more competitive. Aramex's acquisition spree, highlighted by its purchase of MyUS and CX partnership with Sprinklr, illustrates a pivot from pure transport to customer experience orchestration. Contract renegotiations now hinge on data-sharing portals, real-time delivery proofs, and carbon-intensity dashboards, reflecting shifting shipper expectations. Specialist niches-project cargo for giga-city construction, dangerous-goods handling for battery logistics, and high-security vaulting for jewelry shipments-offer margin-rich lanes but demand multi-discipline certifications. Consequently, mid-tier regional firms partner with global 3PLs, pooling fleet assets and regulatory expertise. Freight transport incumbents respond by launching mini-hub networks that shorten pick-up windows for e-tailers while still servicing heavy-haul obligations. The outcome is a braided service topology where conventional FTL, LTL, and parcel flows co-exist on shared digital control towers, elevating overall asset productivity across the GCC freight and logistics market.

The GCC Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, and More), by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), and by Country (Qatar, United Arab Emirates, Saudi Arabia, and Rest of GCC). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Agility Logistics

- Al Madina Logistics

- Al-Futtaim Logistics

- Almajdouie Group

- Aramex

- Asyad

- Bahri

- Batic Investment & Logistics Company (Including Mubarrad)

- DHL Group

- DP World

- DSV A/S (Including DB Schenker)

- Elite Express Cargo LLC

- FedEx

- Flow Progressive Logistics

- Freight Systems

- Gulf Agency Company (GAC)

- Globelink West Star Shipping

- Gulf Warehousing Company (GWC)

- Hala Supply Chain Services

- JAS Worldwide

- Jenae Logistics LLC

- Kuehne+Nagel

- Mac World Logistics LLC

- Masstrans Freight LLC

- Qatar Navigation Q.P.S.C. (Milaha)

- Noon Logistics

- RAK Logistics

- S.A. TALKE

- Saudi Post- SPL (Including Naqel Express)

- Sharaf Group

- SMSA Express Transportation Co., Ltd.

- Zahid Group (Including Wared Logistics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Logistics Performance

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls and Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 Qatar

- 4.21.2 Saudi Arabia

- 4.21.3 United Arab Emirates

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 Qatar

- 4.22.2 Saudi Arabia

- 4.22.3 United Arab Emirates

- 4.23 Value Chain and Distribution Channel Analysis

- 4.24 Market Drivers

- 4.24.1 Vision-2030 Infrastructure Corridors

- 4.24.2 E-Commerce Boom and Last-Mile Demand

- 4.24.3 Integrated Free-Zone Value Propositions

- 4.24.4 Shift of Manufacturing Near Major Ports (Saudi, UAE)

- 4.24.5 Drone and AV Pilots for Desert Last-Mile

- 4.24.6 Voluntary Carbon-Neutral Freight Programs

- 4.25 Market Restraints

- 4.25.1 Fragmented Postal Addressing and COD Culture

- 4.25.2 Driver and Warehouse-Staff Shortages

- 4.25.3 Limited Rail Interoperability Across GCC Borders

- 4.25.4 High Insurance Premia for Red Sea Piracy Risk

- 4.26 Technology Innovations in the Market

- 4.27 Porter's Five Forces Analysis

- 4.27.1 Threat of New Entrants

- 4.27.2 Bargaining Power of Suppliers

- 4.27.3 Bargaining Power of Buyers

- 4.27.4 Threat of Substitutes

- 4.27.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Qatar

- 5.3.2 Saudi Arabia

- 5.3.3 United Arab Emirates

- 5.3.4 Rest of GCC

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Agility Logistics

- 6.4.2 Al Madina Logistics

- 6.4.3 Al-Futtaim Logistics

- 6.4.4 Almajdouie Group

- 6.4.5 Aramex

- 6.4.6 Asyad

- 6.4.7 Bahri

- 6.4.8 Batic Investment & Logistics Company (Including Mubarrad)

- 6.4.9 DHL Group

- 6.4.10 DP World

- 6.4.11 DSV A/S (Including DB Schenker)

- 6.4.12 Elite Express Cargo LLC

- 6.4.13 FedEx

- 6.4.14 Flow Progressive Logistics

- 6.4.15 Freight Systems

- 6.4.16 Gulf Agency Company (GAC)

- 6.4.17 Globelink West Star Shipping

- 6.4.18 Gulf Warehousing Company (GWC)

- 6.4.19 Hala Supply Chain Services

- 6.4.20 JAS Worldwide

- 6.4.21 Jenae Logistics LLC

- 6.4.22 Kuehne+Nagel

- 6.4.23 Mac World Logistics LLC

- 6.4.24 Masstrans Freight LLC

- 6.4.25 Qatar Navigation Q.P.S.C. (Milaha)

- 6.4.26 Noon Logistics

- 6.4.27 RAK Logistics

- 6.4.28 S.A. TALKE

- 6.4.29 Saudi Post- SPL (Including Naqel Express)

- 6.4.30 Sharaf Group

- 6.4.31 SMSA Express Transportation Co., Ltd.

- 6.4.32 Zahid Group (Including Wared Logistics)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment