PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693722

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693722

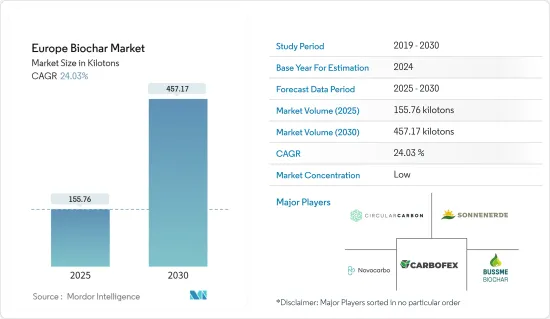

Europe Biochar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe Biochar Market size is estimated at 155.76 kilotons in 2025, and is expected to reach 457.17 kilotons by 2030, at a CAGR of 24.03% during the forecast period (2025-2030).

During the COVID-19 pandemic, the operations of retail sellers were disrupted due to the imposition of lockdowns and other restrictions, while many marketplaces were shut down due to fears of spreading the virus. However, the agricultural sector slowly recovered from the aftermath of the pandemic, with the European biochar market anticipated to register strong growth figures in the next several years.

Key Highlights

- In the long term, the increasing demand for organic farming in the agricultural industry and the rising focus on the waste management industry are expected to serve as the growth engines for the market studied.

- On the flip side, the market growth could be hindered by the production of non-EBC-certified biochar.

- Meanwhile, the potential research and development of biochar in wastewater treatment and as a construction material could present future opportunities for market growth during the forecast period.

- Germany is anticipated to dominate the European biochar market during the forecast period, supported by several ongoing biochar projects spread across the country.

Europe Biochar Market Trends

Increasing Demand from the Agricultural Industry

- Biochar is a charcoal-like substance created by burning organic material from agricultural and forest wastes (also known as biomass) in a controlled process known as pyrolysis. Using biochar as a fertilizer for the soil improves the soil's quality and nutrient-carrying and cycling ability, leading to long-term carbon sequestration.

- Biochar can also remediate contaminated soil while providing environmental benefits. Due to its porous structure, biochar includes a low bulk density that helps to achieve a high specific surface area ranging between 50 and 900 m2 g-1 and a high water-holding capacity.

- Europe includes a sophisticated and highly competitive agro-input market with a large and growing organic industry. The rising consumption of organic food presents potential growth opportunities for the organic farming industry. Therefore, many new producers are now entering the market, meeting the voluntary European Biochar Certificate (EBC) standard.

- While strong market growth is encouraging, organic farmland area must continue to expand faster to meet the European Commission's (2020) Farm to Fork strategy goal of 25% organic area share by 2030. Among European consumers, common reasons for buying organic food include supporting local businesses, health reasons, and not using pesticides or other sprays.

- The organic farming industry is witnessing steady growth across Europe. For instance, Germany is aiming to have a third of all farms organic by 2030 as part of an effort to restructure its agriculture. However, with rising inflation, farmers are asking for more government support.

- Similarly, according to a report published by the European Commission, in France, under the government program, 2023-2027 will see a 36% increase in support for conversion to organic farming, reaching an average of EUR 340 million (USD 376 million) per year. The objective is to double the area covered by organic farming and reach the 18% target of the union agricultural area (UAA) covered by organic farming by 2027.

- Furthermore, as per the SINAB (National Information System on Organic Agriculture), in 2022, approximately 432,000 hectares of Italian land were dedicated to the cultivation of organic forage, while roughly 428,000 hectares were allocated for organic meadows and pastures.

- Thus, owing to the factors above, the demand for biochar in organic farming is anticipated to rise exponentially during the forecast period.

Germany is Anticipated to Dominate the European Market

- Germany is among the top countries actively executing several biochar projects in Europe. For instance, in the German demo site at the Unteres Odertal National Park, low-nutritional grass from the wetlands is converted into biochar through pyrolysis or hydrothermal carbonization (HTC).

- Biochar significantly benefits the agriculture industry by enhancing soil fertility, promoting carbon sequestration, utilizing organic waste, improving microbial activity, and potentially reducing greenhouse gas emissions.

- According to preliminary calculations by the Federal Agricultural Information Center (BZL), German crop production was valued at EUR 37.3 billion (USD 40.5 billion) in 2023, up by 1.4% annually.

- Biochar is also widely used as animal feed in livestock farming in Germany.

- As per the German Feed Association (DVT), animal feed production in Germany reached 16.1 million tons in 2023. According to Statistisches Bundesamt (a federal authority of Germany), the Import value of food and animal feed to Germany was EUR 64.64 billion (USD 70.18 billion) in 2022 and registered growth when compared to EUR 62.79 billion (USD 68.17 billion) in 2021.

- Biochar is linked to water purification through its ability to adsorb contaminants and improve water quality. When added to water treatment systems, biochar acts as a filtration medium, effectively capturing impurities such as heavy metals, organic pollutants, and nutrients. Its porous structure provides a large surface area for adsorption, making it an effective and sustainable method for water purification. This application is valuable in addressing water pollution issues and enhancing the overall quality of water resources.

- Biochar is also being used more extensively in the water treatment industry. The German water treatment industry is the largest in Europe and continues to grow considerably. The country includes the largest market for industrial wastewater treatment (WTP) plants across Europe.

- There are around 3,000 treatment plants spread across the region, with around 12,000 discharging companies. Every year, more than 920 million cubic meters of industrial wastewater is treated before being safely discharged into the environment.

- According to the Statistisches Bundesamt, the industry revenue of water collection, treatment, and supply in Germany was valued at USD 11.41 billion in 2023 and is projected to reach USD 11.73 billion by 2025.

- Thus, the abovementioned factors indicate the growth of end-user applications of biochar in Europe, thereby strengthening demand for biochar during the forecast period.

Europe Biochar Industry Overview

The European biochar market is fragmented, with the top players accounting for a marginal market share. Some of the key companies in the market include (not in any particular order) Carbofex Ltd, Circular Carbon GmbH, Sonnenerde GmbH, Novocarbo GmbH, and BussmeEnergy AB.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Organic Farming in the Agricultural Industry

- 4.1.2 Increasing Focus on the Waste Management Sector

- 4.1.3 Others

- 4.2 Restraints

- 4.2.1 Non-EBC Certified Biochar Production

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Technology

- 5.1.1 Pyrolysis

- 5.1.2 Gasification Systems

- 5.1.3 Other Technologies

- 5.2 Application

- 5.2.1 Agriculture

- 5.2.2 Animal Farming

- 5.2.3 Industrial Uses

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Nordic

- 5.3.7 Turkey

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Bussme Energy AB

- 6.4.2 Circular Carbon Gmbh

- 6.4.3 Carbofex Ltd

- 6.4.4 Carbon Centric

- 6.4.5 Carbon Finland Oy

- 6.4.6 Carbon Gold Ltd

- 6.4.7 Carbuna

- 6.4.8 Charline Gmbh

- 6.4.9 Egos Gmbh

- 6.4.10 Eoc Energy Ocean

- 6.4.11 Lucrat Gmbh

- 6.4.12 Nettenergy BV

- 6.4.13 Novocarbo Gmbh

- 6.4.14 Sonnenerde Gmbh

- 6.4.15 Verora AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential Use in Wastewater Treatment and Construction Material