PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693698

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693698

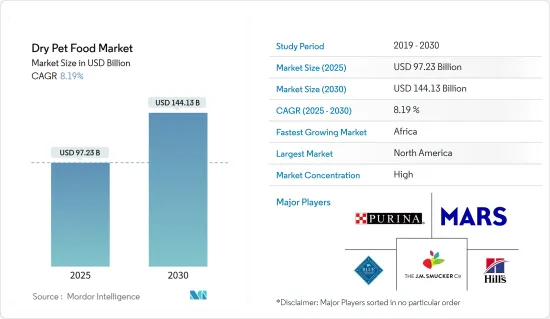

Dry Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Dry Pet Food Market size is estimated at USD 97.23 billion in 2025, and is expected to reach USD 144.13 billion by 2030, at a CAGR of 8.19% during the forecast period (2025-2030).

Globally, pet humanization is on the rise. According to the American Pet Products Association, over 67% of U.S. households (approximately 84.9 million) owned pets in 2020-21, and this number is projected to increase. As a result, pet food manufacturers are rolling out premium products, catering to the evolving trend of pet parenting.

Dry pet foods are increasingly favored over other pet food products. Pet owners appreciate the convenience of dry foods, ensuring they don't compromise on nutrition. This trend is especially pronounced among young, urban, and working pet owners globally, who value the ease of storage and feeding that dry pet foods offer.

Cats and dogs dominate the dry pet food industry. The American Pet Products Association's (APPA) National Pet Owners Survey for 2023-2024 reveals that nearly 67% of U.S. households have a pet. Furthermore, the survey highlights that 58% of these households own a dog, marking a significant increase over the past five years. This rising affinity for cats and dogs is set to boost the demand for a wider variety of pet food supplies, propelling the market forward during the forecast period.

Dry Pet Food Market Trends

Growing Trend of Pet Humanization in All Regions

An increasing number of pet owners are opting for products and experiences that mirror human standards, often identifying more as "pet parents" than mere owners. This trend, particularly pronounced in developed nations, has significantly shaped the market landscape. Consequently, as pet humanization continues to rise, it is poised to propel the growth of the pet food industry.

According to the European Pet Food Federation (FEDIAF), pet ownership in Europe is increasing. It indicates that by the end of 2022, 50% of European households (166 million homes) had pets. Within the EU, 27% of households have at least one cat, and 25% have at least one dog, resulting in over EUR 20 billion in related services and products. Germany stands out as the frontrunner, leading in both cat and dog populations. Notably, cats reign as the preferred pet across the EU, with every country reporting a higher cat population than dogs. An exception is Spain, where dogs surpass cats by a notable margin of approximately 6 million.

In 2023, boasting over 200 million pets, China has swiftly ascended to become the world's third-largest pet-owning nation. The younger generations in China, nurtured with a cosmopolitan perspective, increasingly view cats and dogs as valued companions deserving of care. Notably, around 90% of pet owners in China are women, with over 76% being under the age of 30. Data from China's National Bureau of Statistics reveals a staggering 2,000% growth in China's pet economy over the last decade. This trend shows no signs of slowing down as huge portions of the market remain relatively untapped.

As consumers increasingly prioritize health and nutrition for their pets, companies are responding by rolling out a greater number of premium products. For example, MARS Petcare introduced a premium line of cat food under its IAMS brand in India. This line features four distinct dry variants, each crafted to bolster the natural defenses of both adult cats and kittens. With a rising trend in pet adoption, the push towards premium pet food is set to grow, further expanding the market during the forecast period.

North America Dominates the Market

In 2023, pet owners in the U.S. shelled out over USD 147 billion on their furry companions, with a significant USD 64.4 billion going specifically to pet food and treats, as highlighted by a recent survey from the American Pet Products Association. The survey further revealed that the pet industry's contribution to the U.S. economy surged to USD 303 billion in 2023, up from USD 260 billion in 2022.

Kibbles dominate the dry pet food market, favored by pet owners for their convenience and cost-effectiveness. Kibbles can be tailored to address specific health concerns, like kidney support or digestive issues, simply by modifying their ingredient compositions. Beyond kibbles, other dry pet food options have emerged, including dehydrated, air-dried, baked foods, and meal toppers. These alternatives are gaining traction in the region, thanks to their limited ingredient use, enhanced nutrient density, and lack of added preservatives.

In the United States and Canada, specialized pet shops, mass retail stores, pet superstores, online platforms, niche specialists, grocery chains, drugstores, and agricultural supply stores serve as the primary distribution channels for dry pet food. To enhance safety and efficiency, pet food manufacturers are increasingly automating their production processes. By leveraging cutting-edge technologies like automated formulation, batching, drying, coating, and liquid delivery companies are not only achieving cost efficiencies but also ensuring top-notch product quality. Key players in the North American dry pet food market include Nestle Purina Petcare Company, Mars Inc., Hill's Pet Nutrition Inc., and Blue Buffalo Co. Ltd.

Consumers favor both dry dog and cat food due to their affordability and convenience. As a result, rising pet expenditures and heightened customization of pets' nutritional needs have driven substantial market growth in this region.

Dry Pet Food Industry Overview

The dry pet food market is consolidated, and the market players include Mars Inc., Nestle SA (Purina), The J.M. Smucker Company, Colgate-Palmolive Company (Hills Pet Nutrition Inc.), and Blue Buffalo Company Ltd. Major players in the market have extended their product portfolio and broadened their business to maintain their market position. The key players in the market are also expanding their product ranges and plant capacities and introducing their products in new areas to increase their market presence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Trend of Pet Humanization

- 4.2.2 Growing Trend of E-Commerce

- 4.2.3 Increasing Concern over Pet Allergies and Intolerances

- 4.3 Market Restraints

- 4.3.1 High Cost of Dry Pet Food

- 4.3.2 Limited Availability of High Quality Ingredients

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Animal Type

- 5.1.1 Dogs

- 5.1.2 Cats

- 5.1.3 Other Animals

- 5.2 Product Type

- 5.2.1 Kibble

- 5.2.2 Other Product Types

- 5.3 Ingredient Type

- 5.3.1 Protein

- 5.3.1.1 Animal-derived

- 5.3.1.2 Plant-derived

- 5.3.2 Cereals and Cereal Derivatives

- 5.3.3 Other Ingredient Types

- 5.3.1 Protein

- 5.4 Distribution Channel

- 5.4.1 Specialized Pet Shops

- 5.4.2 Online Channels

- 5.4.3 Supermarkets/Hypermarkets

- 5.4.4 Other Distribution Channels

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East & Africa

- 5.5.5.1 South Africa

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Rest of Middle East & Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Mars Inc.

- 6.3.2 Nestle Purina Petcare Company

- 6.3.3 The JM Smucker Company

- 6.3.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.3.5 General Mills Blue Buffalo Pet Products Inc.

- 6.3.6 Clearlake Capital Group L.P. (Wellness Pet Company Inc.)

- 6.3.7 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.3.8 Alltech Inc.

- 6.3.9 Archer Daniels Midland

7 MARKET OPPORTUNITIES AND FUTURE TRENDS