Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693656

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693656

Electric Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 399 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

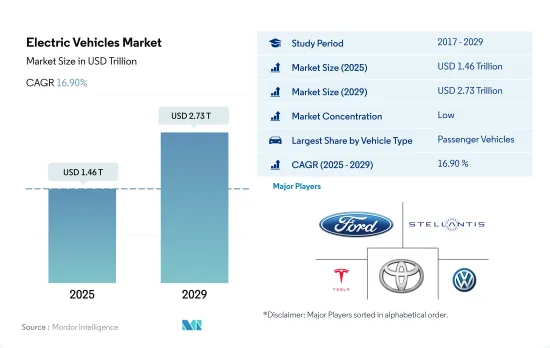

The Electric Vehicles Market size is estimated at 1.46 trillion USD in 2025, and is expected to reach 2.73 trillion USD by 2029, growing at a CAGR of 16.90% during the forecast period (2025-2029).

EV market is witnessing growth driven by rising environmental concerns, government initiatives, increased awareness of EV benefits, and government subsidies

- The global market for electric vehicles (EVs) has experienced substantial growth in recent years, driven by rising environmental concerns, government initiatives, increased awareness of EV benefits, and government subsidies. Notably, passenger cars dominate the EV market, accounting for 67% of total sales. This is attributed to a wider range of models, higher usage rates, and competitive pricing. Thus, the global demand for EVs increased by a remarkable 758.44% during the historic period.

- Various governments worldwide are actively promoting electric mobility. In 2022, the French government expanded its EV incentives, offering private owners up to EUR 6000 and business customers up to EUR 4000 on purchases of electric vehicles priced at EUR 45,000 or below. Such initiatives, seen in multiple countries, contributed to a 55.07% global increase in EV demand in 2022 compared to the previous year.

- Globally, governments are continually revising their subsidy programs to bolster electric and sustainable transportation. For instance, in May 2023, France introduced updated subsidy requirements, providing a EUR 5000 incentive for purchasing a fully electric car priced at EUR 47,000 or less. These ongoing efforts by governments worldwide are expected to propel the global electric vehicle market during 2024-2030.

The rising demand for clean energy in the automotive industry is a key driver of the EV market's growth

- Several governments worldwide have proactively implemented policies to incentivize the adoption of electric vehicles (EVs). Notably, China, India, France, and the United Kingdom set targets to phase out the petrol and diesel vehicle sector entirely by 2040.

- The rising demand for clean energy in the automotive industry is a key driver of the EV market's growth. Original equipment manufacturers (OEMs) are reshaping their strategies for EVs. For instance, in March 2022, Kia Motors unveiled plans to enter the electric pickup truck segment, with two models slated for release by 2027. One of these models will directly compete with established players like Tesla's Cybertruck, Ford's F-150 Lightning, Rivian's R1T, and GMC's Hummer EV. In the same month, Ford announced its commitment to launch a new lineup of four electric commercial vehicles by 2024. This lineup includes the all-new Transit Custom one-ton van and Tourneo Custom multi-purpose vehicle in 2023, followed by the next-generation Transit Courier van and Tourneo Courier multi-purpose vehicle in 2024.

- North America, with its high internet and smartphone penetration, presents significant opportunities for e-commerce companies to tap into the retail e-commerce market. This digital landscape not only aids in expanding their business but also plays a pivotal role in the global EV market's growth. This surge in demand has prompted automakers to ramp up their R&D investments in the electric truck segment, further bolstering the EV market's expansion.

Global Electric Vehicles Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Electric Vehicles Industry Overview

The Electric Vehicles Market is fragmented, with the top five companies occupying 27.50%. The major players in this market are Ford Motor Company, Stellantis N.V., Tesla Inc., Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 93049

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.9.1 Africa

- 4.9.2 Asia-Pacific

- 4.9.3 Europe

- 4.9.4 Middle East

- 4.9.5 North America

- 4.9.6 South America

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Heavy-duty Commercial Trucks

- 5.1.1.2 Medium-duty Commercial Trucks

- 5.1.2 Passenger Vehicles

- 5.1.2.1 Multi-purpose Vehicle

- 5.1.3 Two-Wheelers

- 5.1.1 Commercial Vehicles

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Region

- 5.3.1 Africa

- 5.3.2 Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 Austria

- 5.3.3.2 Belgium

- 5.3.3.3 Czech Republic

- 5.3.3.4 Denmark

- 5.3.3.5 Estonia

- 5.3.3.6 France

- 5.3.3.7 Germany

- 5.3.3.8 Ireland

- 5.3.3.9 Italy

- 5.3.3.10 Latvia

- 5.3.3.11 Lithuania

- 5.3.3.12 Norway

- 5.3.3.13 Poland

- 5.3.3.14 Russia

- 5.3.3.15 Spain

- 5.3.3.16 Sweden

- 5.3.3.17 UK

- 5.3.3.18 Rest-of-Europe

- 5.3.4 Middle East

- 5.3.5 North America

- 5.3.6 South America

- 5.3.6.1 Brazil

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BYD Auto Co. Ltd.

- 6.4.2 Daimler AG (Mercedes-Benz AG)

- 6.4.3 Ford Motor Company

- 6.4.4 Gac Aion New Energy Automobile Co.Ltd

- 6.4.5 General Motors Company

- 6.4.6 Groupe Renault

- 6.4.7 Nissan Motor Co. Ltd.

- 6.4.8 Stellantis N.V.

- 6.4.9 Tesla Inc.

- 6.4.10 Toyota Motor Corporation

- 6.4.11 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.