Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693643

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693643

India Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 234 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

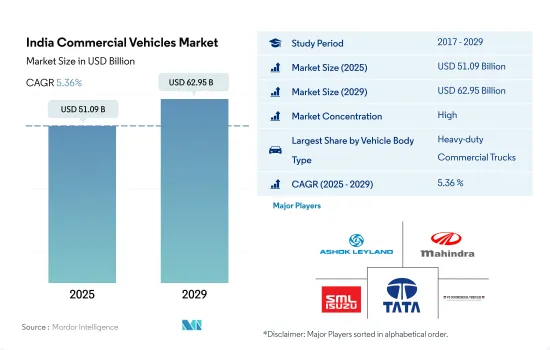

The India Commercial Vehicles Market size is estimated at 51.09 billion USD in 2025, and is expected to reach 62.95 billion USD by 2029, growing at a CAGR of 5.36% during the forecast period (2025-2029).

Indicates a versatile approach to meet the country's diverse commercial transport needs, emphasizing efficiency and adaptability in vehicle design

- The Indian commercial vehicles market encompasses various vehicle body types, including light commercial vehicles (LCVs), medium-duty trucks (MDTs), heavy-duty trucks (HDTs), and buses. This market plays a pivotal role in India's economic landscape, facilitating the movement of goods and passengers across the country's vast geography. The market trends in each vehicle segment mirror broader shifts in India's economy, infrastructure, and regulations, offering valuable insights into the transportation and logistics sectors.

- LCVs dominate the Indian commercial vehicles market thanks to their adaptability, cost-effectiveness, and ability to navigate the country's diverse and often challenging road conditions. These vehicles serve as the backbone of both urban and rural logistics, particularly in sectors like e-commerce, courier services, and FMCG distribution, where their accessibility to remote areas is paramount. The segment's growth is bolstered by favorable government policies, including reduced GST rates and initiatives supporting the MSME sector, which heavily relies on LCVs for transportation.

- MDTs and HDTs are vital for long-haul transportation, playing a key role in India's expanding infrastructure and industrial sectors. These vehicles find primary use in construction, mining, and heavy goods transportation, where their larger capacity and durability are essential. The demand for MDTs and HDTs closely aligns with economic growth, infrastructure projects, and industrial output. Recent regulatory changes, such as the adoption of BS-VI emission standards, have spurred technological advancements in this segment but have also led to increased vehicle costs, impacting demand dynamics.

India Commercial Vehicles Market Trends

Government initiatives and stringent norms drive rapid growth in the electric vehicle market in India

- India's electric vehicle (EV) market is in a growth phase, with the government actively formulating strategies to combat pollution. The Fame India scheme, launched in 2015, has played a pivotal role in driving vehicle electrification. Building on its success, Fame Phase 2, active till April 2022, further bolstered EV sales, especially in 2021, with the government offering subsidies like INR 10,000 grants for electric cars with battery capacities up to 15 kWh.

- State governments across India are increasingly incorporating electric buses into their fleets, aiming to transition from internal combustion engine (ICE) buses. This move not only cuts operational costs but also curbs carbon emissions and improves air quality. In a notable move, the Delhi government greenlit the procurement of 300 new low-floor electric (AC) buses in March 2021, with 100 of them hitting the roads in January 2022. These initiatives contributed to a significant 62.58% surge in demand for electric commercial vehicles in India in 2022 over 2021.

- The demand for electric cars has surged in recent times, driven by the government's introduction of stringent norms. In August 2021, the Indian government unveiled the Vehicle Scrappage Policy, targeting the phasing out of polluting and unfit vehicles, irrespective of their age. This policy, set to be implemented by 2024, is steering consumers toward electric cars. Additionally, the government has set an ambitious target of having 30% of all cars in India electrified by 2030. These initiatives are poised to propel electric car sales during the 2024-2030 period in India.

India Commercial Vehicles Industry Overview

The India Commercial Vehicles Market is fairly consolidated, with the top five companies occupying 91.28%. The major players in this market are Ashok Leyland Limited, Mahindra & Mahindra Limited, SML Isuzu Limited, Tata Motors Limited and VE Commercial Vehicles Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 93031

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Body Type

- 5.1.1 Buses

- 5.1.2 Heavy-duty Commercial Trucks

- 5.1.3 Light Commercial Pick-up Trucks

- 5.1.4 Light Commercial Vans

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ashok Leyland Limited

- 6.4.2 Asia Motor Works Limited

- 6.4.3 Daimler India Commercial Vehicles Pvt. Ltd.

- 6.4.4 Eicher Motors Ltd.

- 6.4.5 Force Motors Ltd.

- 6.4.6 Mahindra & Mahindra Limited

- 6.4.7 SML Isuzu Limited

- 6.4.8 Tata Motors Limited

- 6.4.9 VE Commercial Vehicles Limited

- 6.4.10 Volvo Buses India Private Limited

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.