Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693586

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693586

Middle-East and Africa Business Jet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 178 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

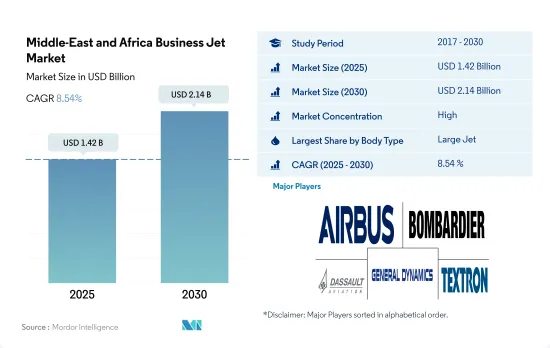

The Middle-East and Africa Business Jet Market size is estimated at 1.42 billion USD in 2025, and is expected to reach 2.14 billion USD by 2030, growing at a CAGR of 8.54% during the forecast period (2025-2030).

Large jets are driving the demand in the market

- Middle East & Africa accounted for around 3% of the global business jet deliveries from 2017 to 2022. After the pandemic, the demand for business jets in the region declined by 26% in 2021, specifically in the large business jet segment.

- The large jet segment in the Middle East & African general aviation market dominates the current operational fleet, accounting for 293 aircraft out of the total 588 aircraft. Adopting large jets is more prevalent in the Middle East & Africa. In terms of the current operational fleet, the large jets accounted for around 50% of the overall Middle East business jet fleet and 36% in the African region of July 2022.

- In 2022, air charter service providers witnessed high demand in the entire region, with a surge in new memberships for business aviation. For instance, in 2021, the UAE-based air charter service provider VistaJet registered a growth of around 100% in new memberships during January and June 2021.

- Bombardier was the leading OEM, with 23% of the current operational fleet size, followed by Gulfstream and Boeing, with 21% and 14%, respectively, in the Middle Eastern business jet fleet as of July 2022. In Africa, Bombardier was the leading player in terms of the current operational fleet, with 22% of the jets, followed by Cessna, BAE, and Gulfstream with 21%, 15%, and 13% of the current fleet, respectively. The surge in UHNWIs in the region is expected to aid the business jet segment in the country. Around 200+ aircraft are expected to be delivered during 2022-2028.

The number of first-time flyers of private jets has increased, further aiding market growth

- The Middle East & Africa accounted for around 3% of the global business jet deliveries from 2017 to 2022. After the COVID-19 pandemic, business jet demand in this region surged by 42% in 2022 compared to 2020, specifically in the large business jet segment. The number of first-time flyers in private jets has increased after the COVID-19 pandemic. Regional companies have also witnessed increased long-distance travel from European countries.

- Adopting large jets is more prevalent in the Middle East & Africa. In terms of the current operational fleet, large jets accounted for around 65%, followed by mid-size jets and light jets with shares of 19% and 13%, respectively, of the overall Middle Eastern business jet fleet as of December 2022. Gulfstream has focused on growth opportunities in this region with its large jet offerings, such as Gulfstream G450 and G650ER.

- In 2021, air charter service providers witnessed high demand in the whole Middle East & Africa with the surge in new memberships for business aviation. For instance, in 2021, UAE-based air charter service provider Vista Jet registered a growth of around 100% in new memberships from January to June 2021 compared to the first half of 2020.

- Gulfstream is the leading original equipment manufacturer, with 15% of the operational fleet size, followed by Cessna and Learjet, with shares of 13% and 10%, respectively, in the Middle Eastern business jet fleet as of December 2022. Furthermore, the number of HNWIs in the region increased from 0.7 million in 2017 to 1.2 million in 2022, with a growth of 72% between 2017 and 2022. Around 241 business jets are expected to be delivered between 2023 and 2030.

Middle-East and Africa Business Jet Market Trends

Oil and gas and real estate were the major industries that boosted the growth of HNWIs in the Middle East

- From 2017 to 2022, there was a surge of around 118% in the UHNWI population in the Middle East compared to Africa, where the number of UHNWIs surged only by around 4.4% in the same period. In 2022, the number of UHNWIs in the Middle East increased by 8%, while Africa experienced a 0.8% decrease compared to 2021.

- The HNWI-friendly policies of the Middle East led to the migration of a large number of HNWIs into these countries. For instance, in 2022, the United Arab Emirates was expected to attract the largest number of high-net-worth individuals. An inflow of around 4,000 millionaires is expected in the country. Most of the HNWIs belong to India, Russia, Africa, and other Middle Eastern countries. Saudi Arabia, the United Arab Emirates, and Turkey were the major countries in terms of the UHNWI population, witnessing growth rates of 98%, 57%, and 59%, respectively, during 2017-2022.

- In the Middle East, the growth in the HNWI population was majorly led by the United Arab Emirates and Israel due to an increase in tech industrial focus. The recovery in oil prices also helped the GDP growth of the Middle East and North Africa, reaching 4.3% in 2022 compared to a contraction of 3.9% in 2021. Financial services, basic materials, real estate, transportation, and logistics were the major industries that accounted for a large number of HNWIs in the region. In Africa, South Africa, Egypt, Kenya, Nigeria, and Morocco account for over 55% of the overall region's high-net-worth individuals (HNWIs).

Middle-East and Africa Business Jet Industry Overview

The Middle-East and Africa Business Jet Market is fairly consolidated, with the top five companies occupying 116.69%. The major players in this market are Airbus SE, Bombardier Inc., Dassault Aviation, General Dynamics Corporation and Textron Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92736

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 High-net-worth Individual (hnwi)

- 4.2 Regulatory Framework

- 4.3 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Large Jet

- 5.1.2 Light Jet

- 5.1.3 Mid-Size Jet

- 5.2 Country

- 5.2.1 Algeria

- 5.2.2 Egypt

- 5.2.3 Qatar

- 5.2.4 Saudi Arabia

- 5.2.5 South Africa

- 5.2.6 United Arab Emirates

- 5.2.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Bombardier Inc.

- 6.4.3 Cirrus Design Corporation

- 6.4.4 Dassault Aviation

- 6.4.5 Embraer

- 6.4.6 General Dynamics Corporation

- 6.4.7 Honda Motor Co., Ltd.

- 6.4.8 Pilatus Aircraft Ltd

- 6.4.9 Textron Inc.

- 6.4.10 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.