Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693542

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693542

Asia-Pacific Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 354 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

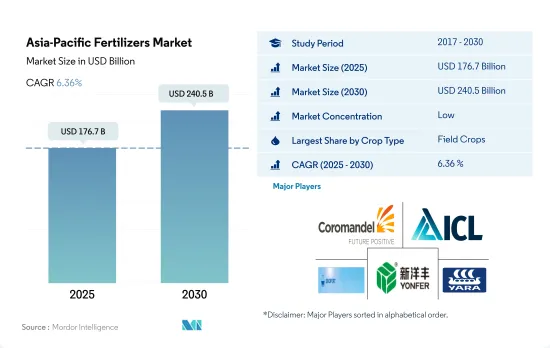

The Asia-Pacific Fertilizers Market size is estimated at 176.7 billion USD in 2025, and is expected to reach 240.5 billion USD by 2030, growing at a CAGR of 6.36% during the forecast period (2025-2030).

Intensive cultivation and soil nutrient depletion increase fertilizer consumption

- The Asia-Pacific fertilizer market is dominated by field crops, which make up around 81.5% of the overall fertilizer market. Field crop production accounts for more than 90.0% of the region's total agricultural land. The major field crops produced in the region are rice, wheat, soybean, rapeseed/canola, and cotton. Generally, field crops consume the most nitrogen fertilizers. Because grains and cereals are grown intensively, they deplete soil nutrients, necessitating the use of more fertilizers to compensate.

- In 2022, horticultural crops constituted 17.9% of the region's fertilizer market value. China and India command over 70.0% of the horticultural crop production area in the region. The rising demand for fresh fruits and vegetables, coupled with efforts to meet this demand, is poised to propel the horticultural crop market.

- China and India, with their abundant arable land and sizable populations, stand out as key agricultural players in the Asia-Pacific. The government's significant financial support for agricultural mechanization and productivity enhancement further bolsters this growth trajectory.

- The region has witnessed a notable uptick in cultivation area, with a 10.5 million ha expansion from 2017 to 2022. Agriculture employs a fifth of the region's population and occupies more than half of its land, making it a vital contributor to the Asia-Pacific economy. The imperative to enhance food security, coupled with evolving climatic conditions and soil nutrient challenges, is poised to fuel the fertilizer market in the region.

The growing population's need for higher food production and productivity may drive the market

- According to the USDA, China, the world's largest fertilizer producer and exporter, accounted for 25% of global fertilizer production. In 2022, the Chinese fertilizer market was valued at USD 70.3 billion, with a consumption of 94.2 million metric tons.

- India, the world's second-largest fertilizer consumer, consumed 81.4 million metric tons in 2022. Despite being the third-largest global producer, India relies on imports for 25% of its urea, 55% of its phosphorus, and 100% of its potash annually.

- The Indonesian agricultural sector has been experiencing a considerable expansion, which has led to an increase in arable land. This, in turn, has boosted the country's agricultural production, making it an essential player in the region's agricultural industry. As a result, Indonesia has become the third-largest consumer in terms of market value and volume consumption, accounting for 5.6% of the value and 6.7% of volume in the region.

- In 2022, Pakistan held a 4.2% share in the Asia-Pacific fertilizer market. Field crops dominated fertilizer consumption, accounting for 86.3% of the volume, followed by horticultural crops at 13.5% and turf & ornamental crops at a negligible 0.1%. This trend can be attributed to the larger land area dedicated to field crops.

- The market is expected to be driven by factors such as the growing population's need for higher food production and productivity, especially since the area available for cultivation is decreasing. Additionally, the adoption of advanced cultivation methods will increase the usage of both conventional and specialty fertilizers.

Asia-Pacific Fertilizers Market Trends

The increase in cultivation area is attributed to the growing domestic and export demand

- Field crop cultivation dominates the Asia-Pacific region, accounting for more than 95% of the total crop area. Rice, wheat, and corn are the major field crops produced in the region, together accounting for about 38% of the total crop area in 2022. The rising area under cultivation is expected to increase the need for fertilizer usage in the country.

- The Asia-Pacific region, which includes China, India, Pakistan, and Australia, is among the world's largest wheat producers. China and India are also the world's largest wheat producers and consumers. Wheat is one of the major staple foods of this region, driving the increase in demand and consumption. Notably, the area under wheat cultivation increased by 638.6 thousand ha from 2018 to 2022. In 2022, China accounted for the production of 138 million metric tons of wheat, making it the largest wheat producer in the world, and India recorded wheat production of 103 million metric tons.

- Rice is the largest cultivated field crop in the region. Its cultivation alone accounted for about 16.44% of the total agricultural land in 2022. Rice is the staple food of Asia and most parts of the Pacific region. China was projected to produce 147 million tons of rice, and India was expected to harvest 124 million tons of rice in 2022. India was also expected to consume 109 million tons while exporting a world-leading 19.5 million tons.

- The surge in both domestic and international demand for field crops has prompted an expansion in the cultivation area dedicated to these crops. This significant increase in cultivated land is expected to have a direct and positive impact on the Asia-Pacific fertilizer market throughout the 2023-2030 period.

About 28% of nitrous oxide emissions from cropland globally are from Chinese agricultural lands

- The average application rate of primary nutrients (nitrogen, potassium, and phosphorus) in field crops in China stood at 129.1 kg/ha in 2022. Nitrogen dominated the mix, accounting for 58.5%, followed by potassium at 25.3% and phosphorus at 16.1%. The primary nutrients are predominantly applied through soil-based methods. In 2022, conventional soil-based primary macronutrient fertilizers held a commanding 69.2% share of the primary macronutrient fertilizer market.

- Asia witnesses a significant demand for primary nutrients, especially nitrogen and potassium fertilizers, owing to the prevalent deficiencies in these nutrients in the region's soils. Notably, the Asia-Pacific region, with its vast land area and population, leads the global agrochemical production and consumption. China's agricultural lands alone contribute to about 28% of the world's nitrous oxide emissions from croplands.

- Among field crops, wheat recorded the highest average primary nutrient application rate at 214.9 kg/ha in 2022. Nitrogen took the lead among primary nutrients, with an average application rate of 448.5 kg/ha. This high nitrogen demand is attributed to its crucial role in plant metabolism, as well as its presence in chlorophyll and amino acids.

- The contamination of surface and groundwater with nitrogen and phosphorus has been linked to inadequate guidance on fertilizer application rates and the potential for excessive crop yields. However, there is a noticeable shift toward the adoption of highly efficient fertilizers.

Asia-Pacific Fertilizers Industry Overview

The Asia-Pacific Fertilizers Market is fragmented, with the top five companies occupying 5.83%. The major players in this market are Coromandel International Ltd., ICL Group Ltd, Sinofert Holdings Limited, Xinyangfeng Agricultural Technology Co., Ltd. and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92607

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Anhydrous Ammonia

- 5.1.2.2.3 Urea

- 5.1.2.2.4 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

- 5.5 Country

- 5.5.1 Australia

- 5.5.2 Bangladesh

- 5.5.3 China

- 5.5.4 India

- 5.5.5 Indonesia

- 5.5.6 Japan

- 5.5.7 Pakistan

- 5.5.8 Philippines

- 5.5.9 Thailand

- 5.5.10 Vietnam

- 5.5.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Coromandel International Ltd.

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 ICL Group Ltd

- 6.4.6 Sinofert Holdings Limited

- 6.4.7 Sociedad Quimica y Minera de Chile SA

- 6.4.8 Xinyangfeng Agricultural Technology Co., Ltd.

- 6.4.9 Yara International ASA

- 6.4.10 Zhongchuang xingyuan chemical technology co.ltd

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.