Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693521

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693521

Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 298 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

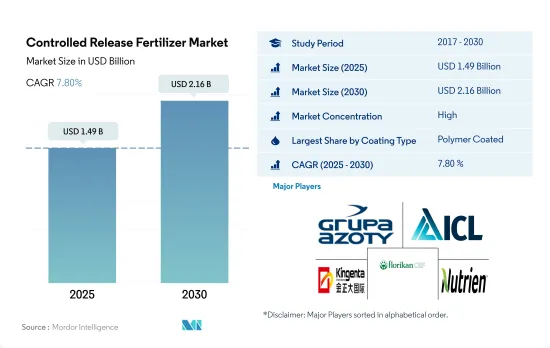

The Controlled Release Fertilizer Market size is estimated at 1.49 billion USD in 2025, and is expected to reach 2.16 billion USD by 2030, growing at a CAGR of 7.80% during the forecast period (2025-2030).

The rising pressure on the agriculture industry to reduce the environmental impact of farming practices and the high nutrient efficiency and precise application will drive the market

- In 2022, control-release fertilizers held a 3.0% value share of the specialty fertilizer market. With mounting pressure on the agriculture sector to minimize environmental impact, the market for control release fertilizers is poised for growth. Their high nutrient efficiency and precise application methods are projected to drive a 7.6% value CAGR from 2023 to 2030.

- Polymer-coated fertilizers play a crucial role in curbing nutrient leaching, a process where excessive rainfall or irrigation washes away nutrients from the root zone. During the study period, the market value of polymer-coated fertilizers surged by 120.6%, capturing a dominant 76.3% market share in 2022. However, the global market faced a setback in 2020 due to supply chain disruptions triggered by the COVID-19 lockdown.

- The polymer-sulfur-coated fertilizers hold the second-largest market share of 18.4% in 2022, worth USD 281.6 million of the overall CRF market. The increasing efforts to enhance production through advanced techniques such as precision farming and dosing of specialty fertilizers, including controlled-release fertilizers, are expected to boost the market for polymers with sulfur-coated fertilizers. The market for polymer-sulfur-coated fertilizers is likely to record a CAGR of 7.3% during 2023-2030.

- In 2022, "other CRFs" constituted 5.3% of the total controlled-release fertilizer market. This segment, encompassing various coatings, is anticipated to witness a 4.3% CAGR in volume from 2023 to 2030. The upswing is attributed to the growing preference for biodegradable coated fertilizers and heightened environmental concerns driving their adoption.

The United States accounted for the largest market share, with field crops accounting for a higher cultivation area

- North America dominates the global controlled-release fertilizer market. In the region, the United States is the largest market for controlled-release fertilizers, accounting for 69.0% of the market share in 2022.

- Europe occupied the second-largest share in the global controlled-release fertilizer market. The controlled-release fertilizer market in Europe is observed to have notably stable growth across all countries in the region, with France occupying the largest share of 22.4%, followed by the United Kingdom for the year 2022.

- The Asia-Pacific is the third-largest regional market for controlled-release fertilizers globally. China dominates the APAC controlled-release fertilizers market, accounting for about 42.1% of the market share in 2022. In China, polymer-coated fertilizers recorded the highest share in the controlled-release fertilizers market, followed by polymer sulfur-coated fertilizers. The polymer-coated fertilizers segment was valued at USD 30.3 million in 2017 and is anticipated to reach USD 97.2 million by the end of 2030.

- Controlled-release urea is the most commonly used form of CRF in the world. Nitrogen loss is one of the main problems faced by rice farmers, and the efficiency of nitrogen utilization in rice is often inadequate. This is due to the large loss of nitrogen due to volatilization, leaching, and denitrification. One way to improve nitrogen efficiency is to use controlled-release urea. Controlled-release urea generally outperforms granular urea fertilizers in reducing nitrogen loss, stimulating plant growth, and increasing nitrogen concentration, thus boosting its preference.

- The increased efficiency of controlled-release fertilizers is anticipated to drive the global market from 2023 to 2030.

Global Controlled Release Fertilizer Market Trends

Rising pressure on the agriculture industry to meet the growing demand for food is expected to increase the area under field crop cultivation globally

- The global agricultural sector is facing many challenges. According to the UN, the world population may exceed 9 billion by 2050. This population growth may overburden the agricultural industry, which is already experiencing an output loss due to a lack of laborers and the shrinkage of agricultural fields caused by rising urbanization. According to the Food and Agriculture Organization, 70% of the global population is expected to live in cities by 2050. Due to the global loss of arable land, farmers now need to utilize more fertilizers to increase crop yields.

- Asia-Pacific is the world's largest producer of agricultural products. Agriculture is critical to the region's economy, as it employs about 20% of the total available workforce. Field crop cultivation dominates the region, accounting for about more than 95% of the total crop area in the region. Rice, wheat, and corn are the major field crops produced in the region, together accounting for about 24.3% of the total crop area in 2022.

- North America ranks as the second-largest arable region globally. Its farms cultivate a diverse range of crops, with a focus on field crops. Notably, corn, cotton, rice, soybean, and wheat are the prominent field crops, as highlighted by the USDA. In 2022, the United States accounted for 46.2% of North America's crop cultivation area. However, the country witnessed a significant drop in crop acreage between 2017 and 2019, primarily due to adverse environmental conditions, leading to severe flooding in regions like Texas and Houston.

The global average application rate of primary nutrients like nitrogen, potassium, and phosphorus in field crops is 164.31 kg/ha

- Corn/maize, rapeseed/canola, cotton, sorghum, rice, wheat, and soybean are some of the major crops worldwide in terms of consumption of primary nutrients. The primary nutrient application rates for these field crops are 230.57 kg/ha, 255.75 kg/ha, 172.70 kg/ha, 158.46 kg/ha, 154.49 kg/ha, 135.35 kg/ha, and 120.97 kg/ha, respectively. Primary nutrient fertilizers are crucial for crops because they play an essential role in plant metabolic processes and assist in forming tissues such as cells, cell membranes, and chlorophyll. Phosphorus is essential for growing high-quality crops, while potassium activates the enzymes needed for plant growth and development.

- The global average application rate of nitrogen, potassium, and phosphorus in field crops is 164.31 kg/ha. Nitrogen is the most widely used primary nutrient fertilizer used in field crops. It accounted for an application rate of 224.6 kg/hectare, followed by potassic fertilizers with 150.3 kg/hectare, and phosphorus as the third-most consumed fertilizer with an application rate of 117.9 kg/hectare in 2022.

- In 2022, the nitrogen application rate was highest in rapeseed, amounting to 347.4 kg/hectare. Similarly, the phosphorus application rate was the highest in corn, at 156.3 kg/hectare, while the potassium application rate was highest in canola, at 248.6 kg/hectare.

- Global field crop cultivation area is increasing, particularly in South American and Asia-Pacific countries. These are the growing markets for fertilizers. Due to their efficiency, specialty fertilizers are widely used in developed regions such as Europe and North America, as well as other regions with widespread nutrient deficiencies. These factors are anticipated to drive the global primary nutrient fertilizers market between 2023 and 2030.

Controlled Release Fertilizer Industry Overview

The Controlled Release Fertilizer Market is fairly consolidated, with the top five companies occupying 77.38%. The major players in this market are Grupa Azoty S.A. (Compo Expert), ICL Group Ltd, Kingenta Ecological Engineering Group Co., Ltd., New Mountain Capital (Florikan) and Nutrien Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92585

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 Bangladesh

- 5.3.1.3 China

- 5.3.1.4 India

- 5.3.1.5 Indonesia

- 5.3.1.6 Japan

- 5.3.1.7 Pakistan

- 5.3.1.8 Philippines

- 5.3.1.9 Thailand

- 5.3.1.10 Vietnam

- 5.3.1.11 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Netherlands

- 5.3.2.5 Russia

- 5.3.2.6 Spain

- 5.3.2.7 Ukraine

- 5.3.2.8 United Kingdom

- 5.3.2.9 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Nigeria

- 5.3.3.2 Saudi Arabia

- 5.3.3.3 South Africa

- 5.3.3.4 Turkey

- 5.3.3.5 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ekompany International BV (DeltaChem)

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Mivena BV

- 6.4.7 New Mountain Capital (Florikan)

- 6.4.8 Nutrien Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.