Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692546

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692546

China Less than-Truck-Load (LTL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 214 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

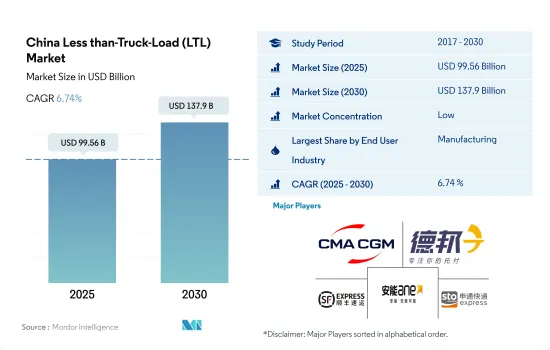

The China Less than-Truck-Load (LTL) Market size is estimated at 99.56 billion USD in 2025, and is expected to reach 137.9 billion USD by 2030, growing at a CAGR of 6.74% during the forecast period (2025-2030).

China's auto exports increased by 57.9% YoY in 2023, driving the growth of the market

- In 2022, the manufacturing end-user segment experienced growth boosted by the manufacturing industry's output, which rose by 3% and reached USD 4.83 trillion. China's manufacturing production sustained its development in 2022, with high-tech manufacturing and equipment manufacturing posting robust performance. Moreover, in 2023, China remained the world's top manufacturing hub, achieving this feat for the 14th consecutive year. The rise in production and exports is driving the demand for road services as the trucking industry plays a significant role in ensuring the timely delivery and distribution of manufactured goods domestically. In 2023, China's auto exports surged 57.9% YoY to a record high of 4.91 million vehicles.

- China is planning to increase its annual natural gas production from 205 bcm to more than 230 bcm by 2025 and maintain its crude oil production at 200 million tons annually. Moreover, the Chinese pharmaceutical industry is anticipated to register a CAGR of 12.2% by 2025. China intends to reinvent its pharmaceutical industry as part of the "Made in China 2025" industrial plan. Furthermore, major manufacturing firms will be fully digitized, and backbone enterprises in key industries will be smart by 2035.

China Less than-Truck-Load (LTL) Market Trends

Rising focus on developing clean energy infrastructure and transport sector investment under 14th Five-Year Plan driving growth

- In 2023, China's clean energy sector significantly contributed to the country's economic expansion. According to Energy and Clean Air (CREA), China's investment in renewable energy infrastructure amounted to USD 890 billion, almost matching global investments in fossil fuel supply for the same year. Clean energy, including renewable energy sources, nuclear power, electricity grids, energy storage, electric vehicles (EVs), and railways, constituted 9.0% of China's GDP in 2023, up from 7.2% YoY. EV production grew by 36% YoY in 2023.

- In the 14th Five-Year Plan (2021-2025), China revealed goals for expanding its transportation network. By 2025, high-speed railways will extend to 50,000 kms, up from 38,000 kms in 2020, with 95% of cities with populations above 500,000 covered by 250-km lines. The country aims to increase its railway length to 165,000 kms, civil airports to over 270, subway lines in cities to 10,000 kms, expressways to 190,000 kms, and high-level inland waterways to 18,500 kms by 2025. The primary objective is to achieve integrated development by 2025, emphasizing advancements in the transformation of the transportation system and its contribution to GDP.

China's retail diesel and gasoline prices were soared to historically high levels amid the Russia-Ukraine War

- In 2023, China imported 11% more crude oil than in 2022, totaling 563.99 mn metric tons (MMT), or 11.28 mn barrels per day. This surge was due to increased global crude oil prices amid the Russia-Ukraine War, causing fuel prices in China to reach historic highs. In Jan-Feb 2024, crude oil imports rose by 5.1% YoY, reaching 88.31 MMT. This increase was driven by purchasing crude oil at lower prices earlier. Brent futures peaked at USD 97.69 in September 2023, fell to USD 72.29 in December, and rose to USD 84.05 by March 2024. The decision made by the OPEC+ group in March 2024 to extend output cuts until the end of June has further boosted crude prices. This move has raised concerns about global oil demand, as the group is reducing production by nearly 6% of world demand. The recent increase in crude prices may also dampen China's imports starting from H2 2024.

- China plans to adjust retail prices for gasoline and diesel to align with recent shifts in global crude oil prices. The price hike reflects a tightening of global supply and a positive forecast for demand. According to NDRC, gasoline and diesel prices in China will increase by USD 28 per ton in 2024. Although there's expectation of declining demand for fuels, oil-based fuels will remain the primary choice until 2035.

China Less than-Truck-Load (LTL) Industry Overview

The China Less than-Truck-Load (LTL) Market is fragmented, with the major five players in this market being CMA CGM Group (including CEVA Logistics), Deppon Logistics Co., Ltd., SF Express (KEX-SF), Shanghai Aneng Juchuang Supply Chain Management Co., Ltd. and STO Express Co., Ltd. (Shentong Express) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92363

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 GDP Distribution By Economic Activity

- 4.2 GDP Growth By Economic Activity

- 4.3 Economic Performance And Profile

- 4.3.1 Trends in E-Commerce Industry

- 4.3.2 Trends in Manufacturing Industry

- 4.4 Transport And Storage Sector GDP

- 4.5 Logistics Performance

- 4.6 Length Of Roads

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Pricing Trends

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Major Truck Suppliers

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Changjiu Logistics

- 6.4.2 CMA CGM Group (including CEVA Logistics)

- 6.4.3 Deppon Logistics Co., Ltd.

- 6.4.4 DHL Group

- 6.4.5 SF Express (KEX-SF)

- 6.4.6 Shanghai Aneng Juchuang Supply Chain Management Co., Ltd.

- 6.4.7 Shanghai YTO Express (Logistics) Co., Ltd.

- 6.4.8 STO Express Co., Ltd. (Shentong Express)

- 6.4.9 Yimi Dida Supply Chain Group Co., Ltd.

- 6.4.10 Yunda Holding Co. Ltd.

- 6.4.11 ZTO Express

7 KEY STRATEGIC QUESTIONS FOR ROAD FREIGHT CEOS

8 APPENDIX

- 8.1 Global Logistics Market Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.