PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692493

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692493

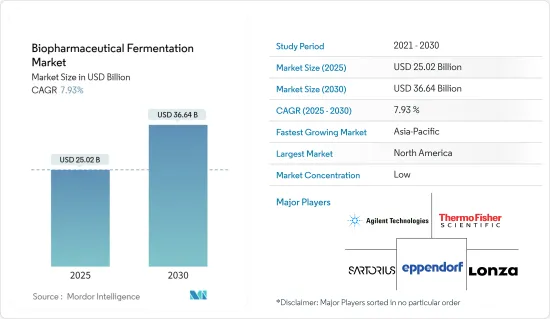

Biopharmaceutical Fermentation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Biopharmaceutical Fermentation Market size is estimated at USD 25.02 billion in 2025, and is expected to reach USD 36.64 billion by 2030, at a CAGR of 7.93% during the forecast period (2025-2030).

The market has seen a surge in demand due to the introduction of cost-effective biosimilars, enhancing the uptake of biotech-based drugs. Fermentation plays a pivotal role in producing the active substances of these drugs. For instance, a January 2024 report from MJH Life Sciences highlighted a notable increase in cancer-related products, with certain categories capturing an 80% share of biosimilars. Key players, through product launches and strategic initiatives, have further bolstered the adoption of these drugs. A case in point is Boehringer Ingelheim's October 2023 launch of an unbranded biosimilar version of AbbVie's Humira, priced at a striking 81% discount to the original.

The global rise in disease prevalence, such as cardiovascular issues, has driven the demand for biotech-based drugs. A January 2024 British Heart Foundation report noted that 7.6 million individuals in England and 620 million worldwide are grappling with cardiovascular diseases, a figure on the rise due to aging and lifestyle changes. This escalating demand for biotech drugs is poised to propel market growth.

Company initiatives, such as Eikonoklastes Therapeutics' November 2022 partnership with Forge Biologics for ALS-targeting gene therapy and Sanofi's August 2022 alliance with Janevent Biologics for oncology drugs, underscore the industry's momentum. These collaborations in biologics development leverage advanced biologics and innovative drug delivery systems to create more effective treatments. Such advancements are expected to boost demand for biopharmaceutical fermentation, driving market growth during the forecast period.

Consequently, factors like the escalating cancer burden and increased strategic activities by industry players are anticipated to fuel market growth. However, the high costs associated with biopharmaceutical fermentation and installations may temper this expansion.

Biopharmaceutical Fermentation Market Trends

Chromatography Segment Expects to Register a Significant CAGR Over the Forecast Period

Significant growth is projected for the chromatography segment in the biopharmaceutical fermentation market during the forecast period. This growth is driven by rising demand for innovative biopharmaceutical drugs and the introduction of new products.

Chromatography separates molecules based on size, charge, hydrophobicity, and specific ligand binding. The choice of chromatography type depends on the physical and chemical characteristics of the fermentation products. For example, reversed-phase high-performance liquid chromatography (HPLC) is employed to purify recombinant human insulin and separate biological variant insulin molecules from various species.

The introduction of new chromatography devices is expanding the segment's product portfolio. For instance, in November 2023, 3M expanded its chromatographic clarifier lineup with the Harvest RC Chromatographic Clarifier, BT500. This 500-mL, single-use clarifier is tailored for monoclonal antibodies, recombinant proteins, and biologics, delivering predictive yield samples in just 10 minutes from a 5-8% packed cell volume (PCV) culture.

In October 2022, Tosoh Bioscience GmbH unveiled the Octave BIO Multi-Column Chromatography (MCC) system, designed for downstream process intensification. Paired with SkillPak BIO pre-packed columns, it streamlines pre-clinical process development. Octave BIO is the one of the first in a series of MCC instruments targeting all biomolecule manufacturing phases, from pre-clinical to clinical and GMP production.

Strategic partnerships between pharmaceutical and biotechnology firms are set to enhance chromatography solutions for efficient downstream processing. For example, in February 2024, Purolite and Repligen Corporation launched Praesto CH1, a 70μm agarose-based affinity resin, tailored for purifying specialized mAbs like bispecifics and recombinant antibody fragments.

Given these developments, especially product launches and collaborations between pharmaceutical and biotechnology firms, the chromatography segment is poised for substantial growth in the coming years.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America is set for significant growth in the biopharmaceutical sector during the forecast period. This expansion is driven by a rising demand for biotech medications, heightened research and development activities, and increased investments in biopharmaceutical fermentation. Additionally, as chronic diseases become more prevalent, medication consumption rises, further propelling the biopharmaceutical sector. This trend not only boosts the demand for biologics and biotech drugs but also underscores the importance of biopharmaceutical fermentation.

Strategic moves by industry players, such as technological advancements, product launches, approvals, fundraising, and partnerships, are expected to drive market growth. For example, in January 2024, WuXi Biologics in the U.S. upgraded its new facility in Worcester, Massachusetts. This enhancement is set to raise the facility's commercial drug substance capacity from 24,000 liters to 36,000 liters, in response to growing service demand. Such an increase in capacity is poised to amplify the utilization of biopharmaceutical fermentation.

Furthermore, rising disease prevalence in North America, including rheumatoid arthritis, diabetes, and cancer, is bolstering the market. These diseases drive the demand for biotech and biological drugs, produced through biopharmaceutical fermentation. Highlighting this, a 2023 report from the Canadian Cancer Society (CCS) emphasized the escalating cancer burden in Canada, signaling a growing opportunity for new biopharmaceuticals and, consequently, market growth.

In January 2024, Eurofins CDMO unveiled its pilot-scale biologic drug development facility in Ontario, tailored for pharmaceutical companies. This facility offers range of services, such as upstream and downstream development, supplies for preclinical or Phase 1 trials. Additionally, in October 2023, Thermo Fisher Scientific boosted its manufacturing capacity in St. Louis, Missouri, for biologics production. The company further expanded its biopharmaceutical footprint by launching a cell therapy manufacturing facility in San Francisco, California, in March 2023.

Given the rising burdens of diseases like diabetes and cancer, the growing demand for biopharmaceutical fermentation, and heightened corporate activities, the market is poised for growth in the coming years.

Biopharmaceutical Fermentation Industry Overview

Numerous global and regional players contribute to the fragmented nature of the biopharmaceutical fermentation market. Key players in the competitive landscape encompass both international and local firms. Notable companies holding significant market shares include Thermo Fisher Scientific Inc., Danaher Corporation, Sartorius Stedim Biotech, Merck KGaA, Eppendorf AG, F. Hoffmann-La Roche Ltd., Nova Biomedical Corporation, Lonza Group AG, Agilent Technologies, and Becton, Dickinson, and Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Biotech based Drugs

- 4.2.2 Rising Research and Development Activities to Produce Novel Biological Drugs

- 4.3 Market Restraints

- 4.3.1 High Cost of Biopharmaceutical Fermentation and its Installation

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Upstreams Products

- 5.1.1.1 Bioreactors/Fermentors

- 5.1.1.2 Bioprocess Analyzers

- 5.1.1.3 Process Monitoring System

- 5.1.1.4 Other Upstream Products

- 5.1.2 Downstream Products

- 5.1.2.1 Filtration and Seperation

- 5.1.2.2 Chromatography

- 5.1.2.3 Consumables and Acessories

- 5.1.2.4 Other Downstream Products

- 5.1.1 Upstreams Products

- 5.2 By Application

- 5.2.1 Antibiotics

- 5.2.2 Recombinant Proteins

- 5.2.3 Other Applications

- 5.3 By End User

- 5.3.1 Biopharmaceutical Industries

- 5.3.2 Contract Research Organization

- 5.3.3 Acedemic Research Institutes

- 5.3.4 Other End users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Agilent Technologies

- 6.1.2 Thermo Fisher Scientific Inc.

- 6.1.3 Lonza Group AG

- 6.1.4 Sartorius Stedim Biotech

- 6.1.5 Eppendorf AG

- 6.1.6 Danaher Corporation

- 6.1.7 F. Hoffmann-La Roche Ltd.

- 6.1.8 Nova Biomedical Corporation

- 6.1.9 Merck KGaA

- 6.1.10 Becton, Dickinson and Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS