Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692046

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692046

Middle East Red Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 220 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

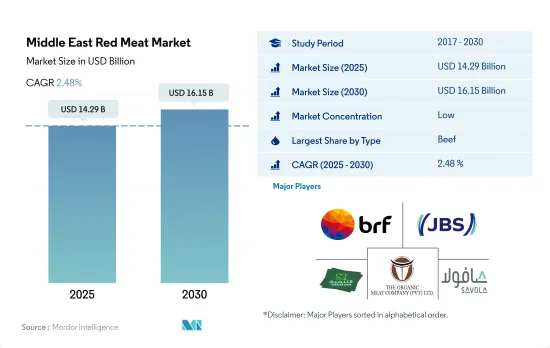

The Middle East Red Meat Market size is estimated at 14.29 billion USD in 2025, and is expected to reach 16.15 billion USD by 2030, growing at a CAGR of 2.48% during the forecast period (2025-2030).

A diverse range of gastronomic preferences drives the demand for various meat products

- Mutton is the major red meat type consumed largely due to the religious affiliations of Bahrain's population. The population of Bahrain in 2023 was 1,485,509, a 0.9% increase from 2022. Bahrain, Qatar, and Kuwait have the highest per capita consumption of mutton in the region. The rise in mutton consumption in Bahrain can be attributed to increased disposable incomes. Bahrain's gross national disposable income per capita was USD 22,707.50 in 2022. The country also saw an increase in the ex-pat population from Western and Asian nations in the past two decades, leading to a more diverse range of gastronomic preferences, including items like hamburgers.

- Apart from mutton and other meat, pork is expected to be the fastest-growing meat consumed in the region, with an anticipated CAGR of 10.50% during the forecast period. The demand for pork increased in the region due to the increased ex-pat population. In 2022, 12.9% of the UAE population was Christian. Similarly, other Middle Eastern countries like Cyprus (which has a 78% Christian population), Lebanon, and Egypt have a high Christian population. This population group consumes all types of red meat, including pork, resulting in higher consumption.

- Beef is the second most consumed meat in the region, and Bahrain has the highest per capita beef consumption, which amounted to 15.80 kg in 2023. The country relies on beef imports from New Zealand, Pakistan, and the United Arab Emirates. Most fresh meat cuts available through online channels are New Zealand's Beef Sirloin, Topside Steak, and Silverside Steak. Future growth is expected to be in high-end food service, particularly in countries such as Saudi Arabia that are looking to develop their tourism industries.

Initiatives for self-sufficiency are anticipated to boost the market's growth

- The red meat consumption in the Middle East observed a growth of 20.61% by value from 2017 to 2022. The expenditure on imported meat tends to be higher in the Middle East, particularly in the Gulf Cooperation Council (GCC) countries, owing to a growing and affluent population. Quality, halal assurance, and taste are the major factors considered by consumers in the Middle East when making red meat purchasing decisions. However, sustainability is not the main reason Middle Eastern consumers buy beef and lamb.

- Saudi Arabia held the major share and highest CAGR by value in 2022. The red meat market in Saudi Arabia grew by 17.36% from 2017 to 2022. The increased consumption was a result of increased demand attributed to the increased disposable income and local production. Saudi Arabia has very high halal standards set by the Saudi Food and Drug Authority (SFDA), and this helps increase the confidence of consumers, especially the Muslim population, in Saudi-made products. Processed red meat is the fastest growing segment in the country owing to the busy lifestyles, increasing number of working women, and other factors.

- Oman is anticipated to be the second fastest-growing red meat-consuming country during the forecast period. It is anticipated to register a growth of 2.23% by value. Increasing investments from the government to support self-sufficiency are expected to play an important part in the growth. State-backed enterprises, including the red meat companies, continue to enhance production and are offered investment opportunities. Consumption of red meat in Oman is largely dominated by mutton, mainly due to the religious affiliation of Omani consumers. Mutton is often used in traditional dishes such as shawarma, kebabs, and biryani.

Middle East Red Meat Market Trends

Underdeveloped local supply chain in the region is a restraint to the production of beef

- Beef production in the region declined by 7.92% in 2022 from 2021. Saudi Arabia accounted for the region's major share of beef production. However, beef production is declining in Saudi Arabia. In 2022, beef production in the country dropped by 21.63%, registering a decline from 40 thousand tons in 2021 to 31 thousand tons in 2022. Imports account for the major beef source in Saudi Arabia. The country's beef imports grew at a rate of 1.54% in 2022 compared to 2021. India, Brazil, and Australia were the major exporters of beef to Saudi Arabia in 2021, with India exporting around 27 thousand tons. With the change in the maximum shelf life of imported frozen products, manufacturers from the United States are hoping that will result in increased sales growth in the Kingdom.

- Qatar has an exponential decline in beef production, and it had a decline of 43.74% in 2022 compared to the previous year. Qatar's beef production reached 925 tons in 2022 from 1644 tons in 2021. However, the local value chain of the bovine category is underdeveloped, and live bovine animals are imported for local slaughtering. Large amounts of water and animal feed are required for fattening large animals such as cattle.

- Bahrain accounted for the lowest production in the region. However, the country saw growth in the production of beef by 3.40% in 2022. The beef market in Bahrain sees a huge demand during the Ramadan season. According to the Ministry of Municipalities Affairs and Agriculture Undersecretary for Animal Wealth Resources, the country imported 11,611 heads of livestock, including 10,500 heads of sheep, 1,077 heads of cattle, and 40 heads of camels, to ensure sufficient stock, bringing the total availability to 27,000 heads of livestock during the Ramadan season of 2023.

The region has observed a growing demand for premium meat products

- Kuwait and Bahrain recorded the highest prices for essential goods in the Gulf region. In 2022, 1 kg of beef was priced at USD 4.91 in Bahrain and USD 4.93 in Kuwait, whereas in the United Arab Emirates and Saudi Arabia, it was priced below USD 4. The reliance of Gulf countries on imports for necessities, including beef and beef products, is one of the leading causes of price increases.

- Spending on premium meat is high in Middle Eastern countries owing to their large affluent populations. For the past eight years, the United Arab Emirates (UAE) and Saudi Arabia have consistently ranked among Australia's top 20 most valuable beef export markets. In October 2022, the price of beef in Australia reached USD 2.82/1 kg, up by 5.3% week on week and 5.1% year on year (Y-o-Y), owing to rising exports. Western-style food services have grown rapidly in the last decade due to accelerated economic growth driven by rapid urbanization, rising disposable incomes, and increased tourism. This has increased demand for high-quality beef grades and cuts.

- The Saudi Food and Drug Authority (SFDA) has expanded the shelf life for chilled beef from the United States from 70 to 120 days. This measure is expected to help US exporters save at least USD 4 per kg due to lower transportation costs using sea transportation while providing Saudi Arabian importers with the flexibility to purchase larger quantities of US beef. Instead of just a few weeks as per the prior regulation, Saudi Arabian importers now have at least 70 days to sell American beef. The extra time is expected to increase profitability since a longer shelf life minimizes the need for last-minute panic sales at steep discounts.

Middle East Red Meat Industry Overview

The Middle East Red Meat Market is fragmented, with the top five companies occupying 2.64%. The major players in this market are BRF S.A., JBS SA, Tanmiah Food Company, The Organic Meat Company Ltd and The Savola Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90341

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Beef

- 3.1.2 Mutton

- 3.1.3 Pork

- 3.2 Production Trends

- 3.2.1 Beef

- 3.2.2 Mutton

- 3.2.3 Pork

- 3.3 Regulatory Framework

- 3.3.1 Saudi Arabia

- 3.3.2 United Arab Emirates

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Beef

- 4.1.2 Mutton

- 4.1.3 Pork

- 4.1.4 Other Meat

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 Bahrain

- 4.4.2 Kuwait

- 4.4.3 Oman

- 4.4.4 Qatar

- 4.4.5 Saudi Arabia

- 4.4.6 United Arab Emirates

- 4.4.7 Rest of Middle East

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Almunajem Foods

- 5.4.2 BRF S.A.

- 5.4.3 Golden Gate Meat Company

- 5.4.4 JBS SA

- 5.4.5 Kibsons International LLC

- 5.4.6 Tanmiah Food Company

- 5.4.7 The Organic Meat Company Ltd

- 5.4.8 The Savola Group

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.