Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690933

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690933

Asia-Pacific Industrial Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 155 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

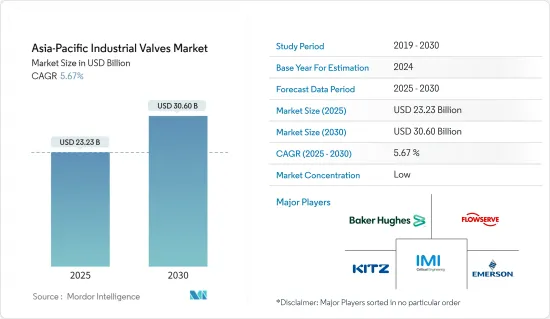

The Asia-Pacific Industrial Valves Market size is estimated at USD 23.23 billion in 2025, and is expected to reach USD 30.60 billion by 2030, at a CAGR of 5.67% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic was a major challenge for the industrial valves market. It directly affected the manufacturer's supply chain across the globe and shut down the production facilities to minimize the risk of spreading the virus.

- The factors driving the market are increasing demand for valves from water treatment plants and the oil and gas industry.

- Further, the need to enable valves for a wider range of applications in the downstream market is contributing to the growth of the Asia-Pacific valves market.

- China accounts for the largest share of the Asia-Pacific industrial valves market.

Asia-Pacific Industrial Valves Market Trends

Growing Demand in the Oil and Gas Industry

- The upstream oil and gas industry is the largest user of valves to outfit millions of wellhead 'Christmas trees' that usually include 3 to 5 valves per tree in sizes of 2' to 8', as well as to segment and control flow through millions of miles of gathering pipelines (2' to 20' valves) and cross-country trunk pipelines (up to 60' or larger) required to bring the crude oil and gas to refineries, and the refined product (gasoline, diesel, natural gas) to end-user markets.

- With the increase in pipelines across the countries, the need for storage terminals to store hydrocarbons also increases. Therefore, Asia-Pacific countries plan to invest in storage terminals to meet the demand.

- Asia-Pacific has dominated the oil and gas downstream market, with most of the demand coming from China, Southeast Asian countries, and India. The energy demand is anticipated to grow by 50-60% in two decades.

- China is expected to build 23 gas storage facilities by 2030, with an investment of around USD 8.5 billion. Completing the storage facilities and the upcoming gas pipelines in the country are expected to boost the midstream sector. As a result, the demand for petroleum products is expected to cross 650 MT by the mid-decade, with the transportation segment having the highest demand of nearly 370 MT.

- Several petrochemical projects are planned to be constructed in the region. For instance, China is expected to have 512 petrochemical projects commence operations in 2021-2025. According to a petrochemicals report published by the International Energy Agency (IEA), nearly all regions except Europe may increase the production of primary chemicals by 2050. However, the most significant capacity growth is seen in Asia-Pacific.

- Also, China targets to slash its growing dependence on gas imports by boosting domestic projects like shale fields to secure its energy supply. The government is expected to fund new efforts to boost domestic production, particularly from unconventional sources like shale gas. It is also estimated that China's shale gas production will reach around 280 billion cubic meters by 2035. Thus, the Chinese government's effort and plan to boost its shale gas production are expected to create an opportunity for industrial valves in the coming years

- Such factors are expected to augment the demand for industrial valves.

India is Expected to Register the Fastest Growth

- India is one of the fastest-growing countries in terms of manufacturing sectors and machinery, giving rise to the need for industrial valves. The government provides benefits to companies setting up manufacturing units. It also outlines various policies to boost the manufacturing sector. For instance, as per the India Brand Equity Foundation (IBEF), in 2023, India's manufacturing exports hit a record high, reaching USD 447.46 billion, marking a 6.03% growth from the previous year, when exports stood at USD 422 billion.

- India is the third-largest producer and consumer of electricity worldwide, with an installed power capacity of 429.96 GW as of January 31, 2024.

- India boasts a thriving mining industry. In FY22, the country had a total of 1,319 reporting mines, with 545 dedicated to metallic minerals and 775 to non-metallic minerals. Moreover, according to the data published by the Indian Brand Equity Foundation (IBEF), during 2022-2023, India's iron ore exports amounted to USD 1.75 billion compared to USD 3.18 billion during 2021-2022.

- India's pharmaceutical industry holds a significant position on the global stage, ranking third in production volume and 14th in production value. Projections from the India Brand Equity Foundation (IBEF) suggest that the industry's market size is set to hit USD 65 billion in 2024, double to USD 130 billion by 2030, and soar to a staggering USD 450 billion by 2047.

- The oil and gas industry is among the eight core industries in India, playing a major role in influencing decision-making for all the other important sections of the economy. India's oil demand is projected to rise rapidly in the world, reaching 10 million barrels per day by 2030.

- According to the International Energy Agency (IEA), natural gas consumption in India is expected to grow by 25 billion cubic meters (bcm), registering an average annual growth of 9% until 2024.

- These factors will likely increase the demand for industrial valves in India during the forecast period.

Asia-Pacific Industrial Valves Industry Overview

The Asia-Pacific industrial valves market is fragmented, with no player capturing a significant share of the market. Some of the major players in the market include (not in any particular order) Emerson Electric Co., KITZ Corporation, Flowserve Corporation, Baker Hughes, and IMI Critical Engineering.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 72535

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Valves from Water Treatment Plants

- 4.1.2 Increasing Demand for Valves in the Oil and Gas Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Capital Investment to Hamper the Market Growth

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 By Type

- 5.1.1 Butterfly Valve

- 5.1.2 Ball Valve

- 5.1.3 Globe Valve

- 5.1.4 Gate Valve

- 5.1.5 Plug Valve

- 5.1.6 Other Types

- 5.2 By Product

- 5.2.1 Quarter-turn Valve

- 5.2.2 Multi-turn Valve

- 5.2.3 Other Products (Control Valves)

- 5.3 By Application

- 5.3.1 Power

- 5.3.2 Water and Wastewater Management (Including Desalination)

- 5.3.2.1 Metal, Mineral, and Mining

- 5.3.2.2 Other Applications

- 5.3.3 By Chemicals

- 5.3.4 Oil and Gas

- 5.3.4.1 Upstream

- 5.3.4.2 Mid-stream

- 5.3.4.3 Downstream

- 5.3.5 Food Processing

- 5.3.6 Pulp and Paper

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Malaysia

- 5.4.6 Thailand

- 5.4.7 Indonesia

- 5.4.8 Vietnam

- 5.4.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Ranking Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Alfa Laval

- 6.3.2 AVK Holding AS

- 6.3.3 Baker Hughes

- 6.3.4 CIRCOR International Inc.

- 6.3.5 Crane Co.

- 6.3.6 Curtiss-Wright Corporation

- 6.3.7 Danfoss AS

- 6.3.8 EBRO ARMATUREN Gebr. Brer GmbH

- 6.3.9 Emerson Electric Co.

- 6.3.10 Flowserve Corporation

- 6.3.11 Georg Fischer Ltd

- 6.3.12 Hitachi Metals Ltd

- 6.3.13 Honeywell International Inc.

- 6.3.14 IMI Critical Engineering

- 6.3.15 ITT Inc.

- 6.3.16 KITZ Corporation

- 6.3.17 NIBCO

- 6.3.18 Okano Valve Mfg. Co. Ltd

- 6.3.19 PARKER HANNIFIN CORP.

- 6.3.20 SAMSON AKTIENGESELLSCHAFT

- 6.3.21 Schlumberger Limited

- 6.3.22 The Weir Group PLC

- 6.3.23 Valvitalia SpA

- 6.3.24 Velan Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.