Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690770

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690770

Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

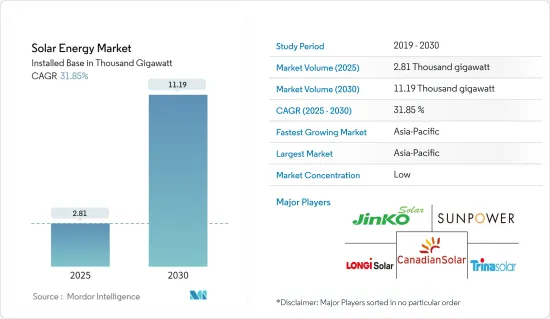

The Solar Energy Market size in terms of installed base is expected to grow from 2.81 thousand gigawatt in 2025 to 11.19 thousand gigawatt by 2030, at a CAGR of 31.85% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, favorable government policies and declining prices and installation costs of solar PV systems, along with the declining price of solar panels and installation costs, are likely to support the global solar energy market's growth during the forecast period.

- On the other hand, factors such as the rising adoption of alternate clean power sources, such as gas-fired power plants and onshore and offshore wind projects, are likely to hinder the market growth during the study period.

- Nevertheless, the integration of solar energy with energy storage systems is expected to create several opportunities for the market in the future.

- During the forecast period, Asia-Pacific is expected to be the largest and fastest-growing region in the solar energy market due to the increasing solar installations in China, India, and other countries.

Solar Energy Market Trends

Solar Photovoltaic (PV) Segment Expected to Dominate the Market

- Solar PV systems convert sunlight directly into electricity using solar panels made up of semiconductor materials, typically silicon. When sunlight strikes the solar cells, it excites electrons, generating a flow of direct current (DC) electricity. This DC electricity is converted into alternating current (AC) using an inverter in homes, businesses, and the electrical grid.

- The solar photovoltaic (PV) segment is expected to account for the most significant yearly capacity additions for renewables, well above hydro and wind, for the next five years. According to the International Renewable Energy Agency (IRENA 2024), Solar PV installed capacity accounted for 1412.093 GW, comparatively higher than the 721.989 GW installed in 2020.

- Additionally, the global electricity demand is continuously increasing due to population growth, urbanization, and the electrification of various sectors, including transportation. Solar PV systems offer a scalable and decentralized solution to meet this growing energy demand, particularly in regions with limited or unreliable grid infrastructure.

- Global solar PV annual installations grew by over 80% in 2023 compared to 2022, reaching 417 GWdc of grid-connected installed capacity. Due to ambitious government targets, policy support, and increasing competitiveness, investments in PVs are expected to grow further in the coming years.

- According to the International Energy Agency (IEA), global solar PV manufacturing capacity is expected to reach almost 1,000 GW in 2024, adequate to meet the annual demand for IEA Net Zero Emissions by 2050 scenario of almost 650 GW in 2030.

- Governments in the United States, Europe, and India have started to prioritize solar PV supply chain diversification, implementing policies such as India's Production Linked Incentive (PLI) scheme and the US Inflation Reduction Act (IRA) to provide direct financial incentives for domestic manufacturers to increase their competitiveness with Chinese ones. As a result, over 120% more new solar PV manufacturing projects were announced from 2022 to 2023 to potentially create national PV supply chains with over 20 GW of capacity in each region.

- On the other hand, India is witnessing significant developments in solar PV deployments. The country installed 9.71 GW of solar PV in 2023, 15.4% more than in 2022. A new target to increase PV capacity auctioned to 40 GW annually, and the dynamic development of the domestic supply chain is expected to result in a further acceleration in PV growth shortly.

- Moreover, governments worldwide have introduced supportive policies and financial incentives to promote solar PV installations. These measures include feed-in tariffs, tax credits, grants, and net metering programs. Such policies encourage the adoption of solar PV systems by reducing upfront costs, improving investment returns, and facilitating grid integration.

- For instance, Australia has set a goal of generating 82% of its electricity through renewable sources like solar PV and wind by 2030, and solar PV is expected to be a significant contributor to achieving this target.

- Therefore, based on the abovementioned factors, the utility sector is expected to dominate the solar energy market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Many countries in Asia-Pacific, such as China, India, and Japan, have implemented ambitious renewable energy targets and supportive policies to encourage solar energy adoption. These policies include feed-in tariffs, renewable portfolio standards, and subsidies for solar installations. Strong government support and stable policy frameworks have created a conducive environment for the region's solar energy market growth.

- According to the China National Energy Agency, China's cumulative installed power capacity reached approximately 2.92 TW, a 13.9% increase year over year, with solar power accounting for 609.49 GW, a 55.2% jump year over year. Also, according to the new guidelines from the National Development and Reform Commission (NDRC) and the National Energy Administration (NEA), China plans to expand its distributed renewable energy capacity to 500 GW by 2025.

- Furthermore, the countries in Asia-Pacific have a rapidly growing population and expanding economies, leading to an increasing demand for electricity. Solar energy offers a scalable and sustainable solution to this growing energy demand. As a result, there is a strong market potential for solar energy deployment in the region.

- Moreover, several countries in Asia-Pacific have undertaken ambitious large-scale solar energy projects. For instance, China has been a leader in utility-scale solar installations, with extensive solar farms and solar parks. These large-scale projects have boosted the region's cumulative solar capacity and positioned it as a dominant player in the global solar market.

- In April 2024, Serentica Renewables, part of Vedanta Group, announced that it plans to invest up to INR 30,000 crore (~USD 3.59 billion). The company aims to achieve 17 GW of renewable energy by 2030. Also, Adani Group, an Indian multinational conglomerate, announced that it is planning to invest around INR 2.3 lakh crore (~USD 27.55 billion) through 2030 in India's most ambitious renewable energy expansion and solar and wind manufacturing capacity addition.

- Moreover, Asia-Pacific countries, particularly China, have also emerged as major manufacturing hubs for solar PV components and systems. The region benefits from economies of scale, efficient supply chains, and competitive production costs, significantly reducing the overall cost of solar energy systems. This cost advantage has contributed to the dominance of Asia-Pacific in the global solar energy market.

- Therefore, Asia-Pacific is expected to dominate the solar energy market during the forecast period.

Solar Energy Industry Overview

The solar energy market is fragmented. Some of the key players in the market (in no particular order) include Canadian Solar Inc., JinkoSolar Holding Co. Ltd, Trina Solar Co. Ltd, SunPower Corporation, and LONGi Green Energy Technology Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 71528

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Solar Energy Installed Capacity and Forecast in GW, till 2029

- 4.3 Global Renewable Energy Mix, 2023

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Government Incentives and Policies

- 4.6.1.2 Declining Price and Installation Cost of Solar PV Systems

- 4.6.2 Restraints

- 4.6.2.1 Rising Adoption of Alternate Clean Power Sources

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGEMENTATION

- 5.1 Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.1.1 Overview

- 5.1.1.2 Solar Photovoltaic (PV) Installed Capacity and Forecast, till 2029

- 5.1.1.3 Annual Solar PV Shipments, in GW, till 2023

- 5.1.1.4 Share of Solar PV Shipments (%), by Technology, 2023

- 5.1.1.5 Average Selling Price of Solar PV Module, in USD/W, till 2023

- 5.1.1.6 Key Projects Information

- 5.1.2 Concentrated Solar Power (CSP)

- 5.1.2.1 Overview

- 5.1.2.2 Concentrated Solar Power (CSP) Installed Capacity and Forecast, till 2029

- 5.1.2.3 Solar Thermal Capacity in Operation, in GW, till 2023

- 5.1.2.4 Solar Thermal Installed Capacity Share (%), by Collector Type, 2023

- 5.1.2.5 Key Projects Information

- 5.1.1 Solar Photovoltaic (PV)

- 5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Mexico

- 5.2.1.3 Canada

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 Spain

- 5.2.2.3 Italy

- 5.2.2.4 United Kingdom

- 5.2.2.5 France

- 5.2.2.6 NORDIC

- 5.2.2.7 Turkey

- 5.2.2.8 Russia

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 Vietnam

- 5.2.3.6 South Korea

- 5.2.3.7 Malaysia

- 5.2.3.8 Thailand

- 5.2.3.9 Indonesia

- 5.2.3.10 Rest of Asia-pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Chile

- 5.2.4.4 Colombia

- 5.2.4.5 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Egypt

- 5.2.5.4 Nigeria

- 5.2.5.5 South Africa

- 5.2.5.6 Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Canadian Solar Inc.

- 6.3.2 JinkoSolar Holding Co. Ltd

- 6.3.3 Trina Solar Co. Ltd

- 6.3.4 SunPower Corporation

- 6.3.5 LONGi Green Energy Technology Co. Ltd

- 6.3.6 First Solar Inc.

- 6.3.7 JA Solar Holding

- 6.3.8 Abengoa SA

- 6.3.9 Acciona SA

- 6.3.10 Brightsource Energy Inc.

- 6.3.11 Engie SA

- 6.3.12 NextEra Energy Inc.

- 6.3.13 ACWA Power

- 6.3.14 Sharp Corporation

- 6.3.15 REC Solar Holdings AS

- 6.3.16 Hanwha Corporation

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Energy Storage Systems Integration

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.