Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690765

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690765

South America Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 110 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

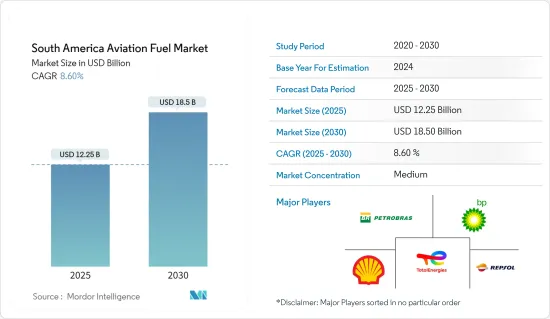

The South America Aviation Fuel Market size is estimated at USD 12.25 billion in 2025, and is expected to reach USD 18.50 billion by 2030, at a CAGR of 8.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the recovering number of air passengers, on account of cheaper airfare in recent times, more robust economic conditions, and increasing disposable income are among the major driving factors for the market.

- On the other hand, the market can face hurdles in the coming years due to the high share of fossil-fuel-based aviation fuels in South American countries, which are responsible for the degradation of the environment.

- Nevertheless, South America is one of the leading regions in biofuels. With an increasing shift towards aviation biofuels, significant opportunities are likely to be created in the near future.

- Brazil is the largest consumer of aviation fuels in South America, resulting in its dominance in the region. With the growing market, the nation is expected to continue its dominance during the forecast period.

South America Aviation Fuel Market Trends

The Commercial Sector to Witness a Significant Growth

- Commercial aviation involves the operation of both scheduled and non-scheduled aircraft, facilitating the commercial air transportation of passengers or cargo. Within this sector, the commercial segment stands out as one of the leading consumers of aviation fuel, constituting approximately a quarter of the total operating expenditure for airline operators.

- The total number of passengers transported in Latin America and the Caribbean (LAC) was 32.3 million in December 2022, which is the highest number of passengers. Meanwhile, the LATAM region had a total number of 53,861 passengers boarded by the airline group.

- The ongoing privatization of airports in countries like Brazil, Paraguay, and Peru is anticipated to contribute to the development of airport infrastructure and an increase in capacity, thereby providing support to the studied market in the region.

- Conversely, there has been a notable rise in the share of short-haul flights within the region, leading to an increased proportion of air traffic. In Latin America, the low-cost (LCC) and ultra-low-cost (ULCC) movements are experiencing significant momentum. Currently, more than ever, low-cost carriers in the region are witnessing accelerated growth, outpacing legacy airlines in their ascent.

- Moreover, in August 2023, Air bp has revealed plans to establish an aircraft fuel supply hub in Paulinia, located in Brazil's Sao Paulo state, as announced during LABACE 2023. The facility, anticipated to commence operations in 2023, is part of the company's strategic investment exceeding USD 10 million. This initiative aims to enhance logistical flexibility and provide improved fuel supply options for aircraft operators.

- Additionally, Air bp is in the process of developing a new fuel tank farm at Sao Paulo Congonhas Airport, set to become operational in 2024. These two upcoming facilities signify a significant investment, demonstrating Air bp's commitment to bolstering infrastructure and services in the aviation sector.

- Thus, the factors mentioned above are expected to drive growth in the commercial segment during the forecast period.

Brazil to Dominate the Market

- In South America, Brazil holds the distinction of being the largest consumer of aviation fuels. The designated products for aircraft use in the country encompass aviation kerosene (QAV), aviation gasoline, and alternative aviation kerosene (alternative QAV).

- The commercial aviation market in Brazil is substantial, with 831,000 flights recorded in 2022, marking a notable 39% increase compared to the previous year, as reported by ANAC. Within this total, 731,000 flights were domestic, reflecting a significant uptick of 33.7%, while international flights accounted for 100,000, showcasing a remarkable 89% increase, according to the Anuario do Transporte Aereo 2022.

- The sales of aviation fuel in Brazil faced an impact from Petrobras' suspension of the supply of imported aviation fuel due to chemical test results from a specific batch, which raised potential concerns. This development also prompted major fuel distributors, including BR Distribuidora and Raizen, to temporarily halt the sale of the product. However, the situation has improved and sales of aviation fuel has recovered from that impact.

- Moreover, In October 2023, Boeing officially inaugurated its Engineering and Technology Center in Brazil, joining the roster of 15 Boeing engineering sites worldwide dedicated to advancing aerospace innovation through cutting-edge technology development. In collaboration with the State University of Campinas (Unicamp), Boeing has also disclosed financial support to expand their sustainability collaboration. This extension involves the development of the third phase of the SAFMaps database, aimed at comprehending the viability of the most promising inputs for Sustainable Aviation Fuel (SAF) production in specific regions of Brazil.

- Overall, the aviation fuel market for Brazil is expected to register decent growth during the forecast period, owing to the supporting government initiatives, which are likely to aid the market's growth further.

South America Aviation Fuel Industry Overview

The South American aviation fuel market is semi-fragmented. Some of the major companies (in no particular order) are Petroleo Brasileiro SA, BP PLC, Shell PLC, TotalEnergies SE, and Repsol SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 71500

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Recovering Number of Air Passengers, on Account of the Cheaper Airfare in Recent Times

- 4.5.1.2 Increasing Disposable Income of Population

- 4.5.2 Restraints

- 4.5.2.1 High Share of Fossil-Fuel-Based Aviation Fuels in South American Countries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel (ATF)

- 5.1.2 Aviation Biofuel

- 5.1.3 AVGAS

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Defense

- 5.2.3 General Aviation

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Petroleo Brasileiro SA

- 6.3.2 Repsol SA

- 6.3.3 BP PLC

- 6.3.4 Shell PLC

- 6.3.5 TotalEnergies SE

- 6.3.6 Pan American Energy SL

- 6.3.7 Exxon Mobil Corporation

- 6.3.8 Allied Aviation Services Inc.

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Shift Towards Aviation Biofuels

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.