PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690730

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690730

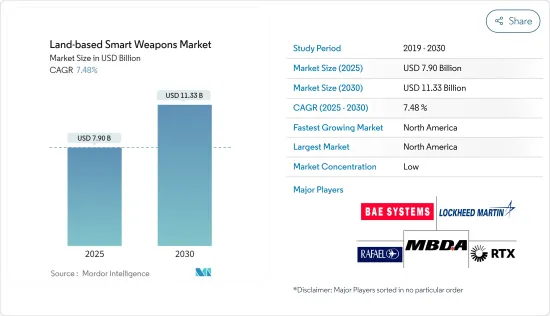

Land-based Smart Weapons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Land-based Smart Weapons Market size is estimated at USD 7.90 billion in 2025, and is expected to reach USD 11.33 billion by 2030, at a CAGR of 7.48% during the forecast period (2025-2030).

Geopolitical tensions and global political instability drive the demand for precision in targeting enemy assets, including vehicles, buildings, and individuals, thereby fueling the growth of the land-based smart weapons market.

Major economies ramp up military expenditures, enabling armed forces to invest significantly in advanced terrestrial combat systems and man-portable weaponry. This trend will boost the land-based smart weapons market during the forecast period.

Government initiatives to develop and manufacture guided ammunition and missiles domestically, thereby reducing reliance on foreign technologies, are poised to propel the market's growth. Additionally, heightened investments in integrating advanced technologies to enhance the accuracy and performance of existing missiles and ammunition are anticipated to further boost sales of smart ammunition for land applications during the forecast period.

Land-based Smart Weapons Market Trends

Ammunitions and Other Products Segment is Expected to Witness Highest Growth During the Forecast Period

As modern warfare evolves, smart weapons and ammunition development and procurement have surged. Rising cross-border conflicts and the imperative to minimize civilian casualties are driving the demand for precision-guided munitions. Escalating defense budgets from global powers further fuel this demand. During 2023, global military spending hit USD 2,443 billion, marking a 6.8% rise from USD 2,240 billion in 2022. This uptick was primarily due to Russia's invasion of Ukraine and mounting geopolitical tensions.

For decades, nations have deployed unguided mortars against personnel, light armor, and structures. Traditional mortar systems often require multiple rounds to stabilize and adjust for weather. This limitation has spurred a transition to guided mortars, which enhance accuracy and reduce ammo consumption. Their precision not only boosts their effectiveness against tanks but also improves the targeting of moving objects. Such benefits have led to the widespread adoption of guided mortar systems across numerous global militaries. Loitering munitions, a distinct weapon category, hover in target zones, scouting, and striking once a target is identified.

Demand for precision-guided artillery shells has surged over the last decade. For example, in June 2024, the French DGA contracted KNDS France for the KATANA 155mm high-precision guided ammunition, boasting cutting-edge guidance tech for meter-level accuracy. In another instance, Aerojet Rocketdyne and NIOA forged a partnership in November 2023, aiming to enhance Australia's Guided Weapons and Explosive Ordnance (GWEO) capabilities. Their collaboration, revealed at INDO PACIFIC 2023, aligns with the Australian Government's Defence Strategic Review, which allocated USD 2.5 billion for a sovereign GWEO manufacturing base. This initiative aims to create a multi-user facility, boosting Australia's defense self-reliance, export potential, local employment, and integration into the global guided weapons supply chain.

In a similar move, in May 2023, the US Army tapped BAE Systems with a USD 72.5 million contract for advancing precision-guided artillery munitions R&D. Programmable ammunition has seen a surge in popularity, leading to widespread international purchases. Highlighting this trend, a European NATO customer engaged Rheinmetall in December 2022 for 45,000 programmable cartridges in the 40 mm x 53 HV HE-T ABM (High-velocity High Explosive-Tracer Airburst Munition) caliber, with deliveries slated for the first half of 2024. Such advancements and procurement of cutting-edge munitions are poised to propel this segment's growth during the forecast period.

North America to Dominate the Market During the Forecast Period

North America currently leads the market and is poised to maintain its position throughout the forecast period. This dominance is primarily attributed to the substantial military spending by the US, which fuels its land forces' development and procurement initiatives. For example 2023, the US military's defense budget reached USD 916 billion, marking a 2.3% increase from 2022. These heightened investments in advanced weaponry directly respond to perceived threats from China's and Russia's bolstered battlefield capabilities.

Consequently, the US is actively testing advanced smart weapons and ammunition to address these challenges. For instance, in March 2024, the US Department of Defense (DoD) unveiled its fiscal year 2025 budget proposal, dedicating a notable USD 143.2 billion to research, development, testing, and evaluation (RDT&E). USD 29.8 billion is allocated explicitly for precision-guided artillery ammunition and related munitions. This allocation highlights a strategic shift towards advanced weaponry, underscoring its importance in modern combat despite the associated costs.

Similarly, in April 2023, the US Army revealed its development of the XM1223 Multi-Mode Proximity Airburst (MMPA) ammunition. This High Explosive Proximity (HEP) round, designed for the M-SHORAD chain gun, can be programmed to target small unmanned aircraft systems (UASs) and ground vehicles. Additionally, the DoD is enhancing the Ground-based Midcourse Defense (GMD) system's capabilities and reliability. In August 2023, the US Army further solidified its commitment to advanced munitions by awarding a contract modification for extended Excalibur 155mm guided projectiles. Such strategic investments are set to propel the region's growth at an accelerated pace during the forecast period.

Land-based Smart Weapons Industry Overview

The land-based smart weapons market is fragmented and features a diverse array of local and international players supplying guided weapons, programmable ammunition, and missiles to global land forces. Beyond the international entities, numerous state-owned firms are developing and producing smart weapons for domestic use and are also eyeing export prospects.

Key players in this market include RTX Corporation, Lockheed Martin Corporation, MBDA, BAE Systems plc, and Rafael Advanced Defense Systems Ltd. As several developing nations set their sights on acquiring next-generation land-based smart weapons, market players are seizing the opportunity, offering advanced solutions to secure a competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product

- 5.1.1 Missiles

- 5.1.2 Ammunitions and Other Products

- 5.2 Technology

- 5.2.1 Satellite Guidance

- 5.2.2 Radar Guidance

- 5.2.3 Infrared Guidance

- 5.2.4 Laser Guidance

- 5.2.5 Other Technologies

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 General Dynamics Corporation

- 6.2.3 Lockheed Martin Corporation

- 6.2.4 RTX Corporation

- 6.2.5 Rheinmetall AG

- 6.2.6 MBDA

- 6.2.7 Rafael Advanced Defense Systems Ltd.

- 6.2.8 Safran SA

- 6.2.9 Northrop Grumman Corporation

- 6.2.10 IAI

7 MARKET OPPORTUNITIES AND FUTURE TRENDS