Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689901

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689901

Low Friction Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

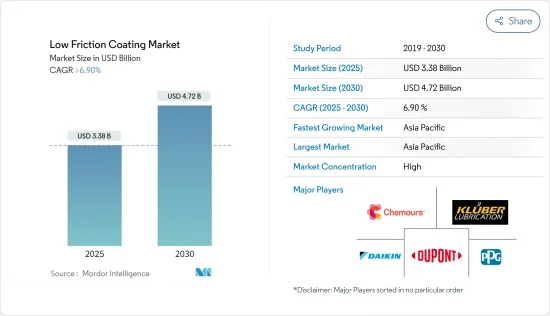

The Low Friction Coating Market size is estimated at USD 3.38 billion in 2025, and is expected to reach USD 4.72 billion by 2030, at a CAGR of greater than 6.9% during the forecast period (2025-2030).

Key Highlights

- Factors driving the market include the increasing demand for low-friction coatings in the aerospace industry and increasing applications in the automotive industry across major economies.

- However, government regulations on the toxicity of PTFE (polytetrafluoroethylene) are expected to hinder the market's growth.

- The growing demand for flow-friction coating in the healthcare industry is expected to act as an opportunity for the market studied in the coming years.

- During the forecast period, the low friction coating market is estimated to register the fastest growth and be the most dominant in Asia-Pacific.

Low Friction Coating Market Trends

Increasing Demand for Low Friction Coating in the Automotive and Transportation Industry

- Low-friction coatings possess extremely low coefficients of friction (COF), excellent release properties for resistance to galling, fretting, and sticking, high corrosion resistance, and many other benefits.

- Therefore, there is an increasing demand for low-friction coatings in the Automotive and Transportation Industry driven by the need for improved fuel efficiency, reduced emissions, and enhanced performance, as well as the adoption of new technologies like electrification and autonomous vehicles.

- Moreover, the rising volume of vehicle production globally is propelling the demand even further. For instance, according to the Organisation Internationale des Constructeurs d'Automobiles (OICA), automotive production globally increased from 84.83 million units in 2022 to 93.54 million units in 2023, representing a growth of 17% year-on-year.

- Furthermore, according to the European Automobile Manufacturers Association, in the first three quarters of 2023 (January 2023 to September 2023), the total production of cars in Europe increased by almost 14% compared to the same period in 2022. This substantially boosted the demand in the low-friction coating market.

- The automotive industry is expected to grow significantly over the coming years. Evolving digital technology, changes in customer sentiment, and economic health have played a vital role in non-commercial business practices of manufacturing vehicles.

- For instance, various automotive manufacturing companies such as Hyundai Motor Group, BMW Group, Toyota, Honda, Ford Motor Company, and General Motors have announced investments in electric vehicle manufacturing in North Carolina, Michigan, Ohio, Missouri, Kansas, and other states. This is likely to boost automotive manufacturing, thereby increasing the demand for low-friction coating.

- Hence, the automotive and transportation industry is projected to exhibit the highest demand for low-friction coating during the forecast period, solidifying its dominance in the market.

Asia-Pacific to Witness the Fastest Growth

- Asia-Pacific is expected to dominate the market during the forecast period. The rising demand for low-friction coatings, combined with the growing automotive and healthcare industry in countries like China and India, is expected to drive the demand for low-friction coatings in this region.

- The largest producers of low-friction coating are based in Asia-Pacific. Some of the leading companies in the production of low-friction coating are VITRACOAT, Daikin Industries, The Chemours Company, Dow, and ASV Multichemie Private Limited.

- China is the world's largest automobile market in terms of production and sales. According to the China Association of Automobile Manufacturers (CAAM), vehicle production in China reached 30.16 million units in 2023, growing 11.6% compared to the previous year.

- Furthermore, according to the Society of Indian Automotive Manufacturing (SIAM) data, in the financial year 2023, India manufactured 4.58 million vehicles, marking a notable increase from the 3.65 million produced in 2022-a growth rate of about 25%.

- According to the Boeing Commercial Outlook 2021-2040, in China, around 8,700 new deliveries will be made by 2040, with a market service value of USD 1,800 billion.

- Furthermore, the construction sector of Malaysia grew in 2023, with a total of 9,144 projects successfully implemented until September 2023, according to Public Works Minister Datuk Seri Alexander Nanta Linggi. In addition, there has been an increase in the country's investments in various commercial construction projects. For instance, Google invested around USD 2 billion in developing the country's first data center and a Google Cloud hub in May 2024. The new hubs will be developed at a business park in central Malaysia's Selangor state to meet the growing demand for IT services and artificial intelligence literacy programs for Malaysian students and educators.

- Given the above-mentioned facts and factors, the demand for low-friction coatings is expected to increase at the fastest rate in the Asia-Pacific market during the forecast period.

Low Friction Coating Industry Overview

The global low-friction coating market is consolidated. Some of the major companies in the market include (not in any particular order) PPG Industries Inc., The Chemours Company, DuPont, Kluber Lubrication, and Daikin Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 69226

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Application in the Automotive Industry

- 4.1.2 Growing Demand for Low-friction Coating in Aerospace Industry

- 4.2 Restraints

- 4.2.1 Government Regulation on Toxicity of Overheated PTFE

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Molybdenum Disulphide

- 5.1.2 Tungsten Disulphide

- 5.1.3 Polytetrafluoroethylene (PTFE)

- 5.1.4 Other Types

- 5.2 By End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Aerospace and Defense

- 5.2.3 Healthcare

- 5.2.4 Construction

- 5.2.5 Oil and Gas

- 5.2.6 Others End-user Industries

- 5.3 By Application

- 5.3.1 Bearings

- 5.3.2 Automotive Parts

- 5.3.3 Power Transmission Items

- 5.3.4 Valve Components and Actuators

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AFT Fluorotec Ltd

- 6.4.2 ASV Multichemie Private Limited

- 6.4.3 Carl Bechem GmBH

- 6.4.4 DAIKIN INDUSTRIES Ltd

- 6.4.5 DuPont

- 6.4.6 Endura Coatings

- 6.4.7 Curtiss-Wright Corporation

- 6.4.8 FUCHS

- 6.4.9 GGB

- 6.4.10 IHI HAUZER TECHNO COATING BV

- 6.4.11 IKV Tribology Ltd

- 6.4.12 Impreglon UK Limited

- 6.4.13 Indestructible Paint Limited

- 6.4.14 Kluber Lubrication (Freudenberg SE)

- 6.4.15 Micro Surface Corp.

- 6.4.16 Poeton

- 6.4.17 PPG Industries Inc.

- 6.4.18 The Chemours Company

- 6.4.19 VITRACOAT

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand for Low Friction Coating in Healthcare Industry

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.