Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687469

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687469

Analog Integrated Circuit (IC) Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

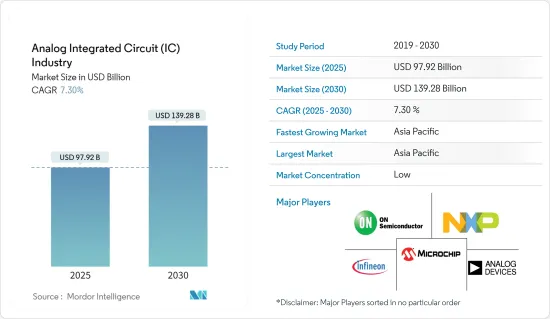

The Analog Integrated Circuit Industry is expected to grow from USD 97.92 billion in 2025 to USD 139.28 billion by 2030, at a CAGR of 7.3% during the forecast period (2025-2030).

Key Highlights

- Analog integrated circuits (ICs) include interconnected components crafted on a single semiconducting wafer. Unlike digital circuits, which operate on just two voltage levels, analog components react to a continuous spectrum of input signals. These circuits are integral to electronic devices, processing and forging various energy output levels. Appliances such as oscillators, DC amplifiers, multi-vibrators, and audio amplifiers rely on analog circuits to ensure consistent input and output levels.

- The rise of technologies like the Internet of Things (IoT) is set to drive market growth, highlighting the advantages of analog ICs in a wide array of real-time connected devices. Notably, IoT's footprint is expanding with the surge in high-speed connectivity, cloud adoption, and data analytics. For example, Forbes projects over 207 billion devices will be globally networked by the closing of 2024, which presents a positive growth opportunity for the market.

- The demand for analog ICs has surged in recent years, fueled by the boom in smartphones, computers, consumer electronics, and electric vehicles. Smartphones utilize various ICs, including charge ICs, display PMICs, SoC PMICs, and Camera PMICs. Industry giants like Apple, Qualcomm, Intel, and Samsung S.LSI dominate this landscape. Given the rising production of technologically advanced smartphones and the integration of 5G and 6G, the global analog IC market is poised for significant growth.

- However, a dip was witnessed in global smartphone need in 2023 compared to 2022, attributed to inflation, waning consumer spending, and a subdued outlook. This downturn is likely to influence market growth negatively. However, a modest recovery is expected in FY 2024 owing to the rising demand for 5G smartphones and the global expansion of 5G networks, especially with the surge in 5G and foldable smartphones. According to GSMA forecasts, by 2025, 5G networks are expected to encompass a third of the global population.

- The reliance on skilled analog chip design engineers is pronounced. However, there is a substantial scarcity in the semiconductor industry. Cindi Harper from Intel highlighted that industry demand for talent outstrips supply. According to Ruchir Dixit of Siemens EDA, a shortfall of 250,000 semiconductor engineers is expected to be seen in the United States over the next five years. In China and Taiwan, deficits of 300,000 and 50,000 engineers are expected, respectively. Such imbalances pose challenges to market growth.

- The Russia-Ukraine War reverberated across multiple industries, including electronics. This geopolitical tension intensified existing semiconductor supply chain disruptions and chip shortages. Such disturbances have led to price volatility in essential raw materials like nickel, palladium, copper, silicon, and titanium, resulting in material shortages.

- According to SEMI, Russia supplied 45-50% of the world's palladium, a crucial material for semiconductor packaging. With global trading doors closing on Russia, semiconductor manufacturers are increasingly pursuing alternative raw material sources, further prolonging semiconductor production delays. This is expected to hamper the growth of the market.

Analog Integrated Circuit (IC) Industry Trends

The Cell Phone Sub-segment is Expected to Hold a Major Share

- In the dynamic world of technology, application-specific analog ICs have become essential for cellular phones and multifunctional handheld devices, where voice communication remains a primary function. These devices, developed for extensive cellular networks like 2G, 3G, and Wimax, utilize transmission formats such as CDMA, GSM, and their enhanced versions.

- Rising smartphone adoption, particularly in developing countries, is driven by population growth and urbanization. For instance, by the end of 2023, GSMA reported that 5.6 billion people, or 69% of the global population, had subscribed to mobile benefits, marking a proliferation of 1.6 billion since 2015.

- The emergence of 5G technology has led to the adoption of 5G smartphones. According to Ericsson Mobility Report, 5 billion 5G mobile subscriptions are expected to be recorded by the end of 2028. These 5G networks are anticipated to cover 85% of the population and operate about 70% of mobile traffic.

- All these factors can be attributed to the continuously increasing share of the cell phone sub-segment of the market as there is an increasing need for advanced features in smartphones, such as great camera quality, AR, and VR, all of which are made possible by analog ICs. The importance of analog ICs lies in their ability to process analog signals with high precision and accuracy. This makes them critical for signal processing, power management, and data conversion applications. Additionally, combining multiple analog circuits on a single chip permits for smaller, more efficient, and cost-effective devices.

- GSMA projects that North America will see smartphone subscribers rise to 328 million by 2025, with mobile penetration at 86% and internet users at 80%. According to Ericsson Mobility Report, Middle East and Africa (MEA) is expected to have 60 million 5G subscribers by 2024, accounting for roughly 3% of total mobile subscriptions. GSMA estimates that there will be about 50 million 5G connections in MENA by 2025, with 20 million in the Arab states alone. These figures highlight the rapid adoption of cell phones, propelling the sub-segment forward.

China is Expected to be the Fastest-growing Market in Asia-Pacific

- China is set to solidify its position as a critical player in the analog IC market, driven by major semiconductor manufacturers, swift industrialization, and a sprawling consumer electronics landscape. The region is celebrated for its high-volume semiconductor production and the widespread adoption of analog ICs across various industries, including automotive, consumer electronics, and telecommunications. These dynamics are poised to propel the growth of the analog IC market in China, offering enticing prospects for market players.

- China's burgeoning IT and data center industry directly responds to the ever-increasing annual data generation. This growth is further underscored by China's rising stature in the global tech arena, primarily fueled by its vibrant data center ecosystem. China's internet data center industry is among the world's most technologically advanced, with many organizations leveraging digital platforms.

- With the increase in investments in data centers and internet penetration, the demand for sensor-enabled devices is also rising. These sensors, which interact with the physical space, necessitate analog processing to convert analog signals to digital ones. Merging these functionalities with digital technology yields a solution that is not only cost-effective and low-power but also reliable. Consequently, these elements are anticipated to bolster the market's growth in the coming years.

- The expanding 5G networking capabilities are set to drive significant demand for analog IC modules. Having made substantial strides in the 5G domain, China boasts a vast network of 5G base stations. Data from MIIT indicates that by the close of February 2024, China had established over 3.5 million 5G base stations. Owing to its hefty infrastructure investments and ambitious rollout strategies, the nation achieved widespread 5G coverage. Projections suggest that by the end of 2024, the number of 5G base stations in China might exceed six million.

- According to a report from South China Morning Post, China's smartphone industry showed signs of rejuvenation in 2023, witnessing a 6.5% uptick in shipments from the prior year. This rebound came as the world's largest handset market grappled with a tentative economic recovery and heightened domestic competition, especially with Huawei Technologies making notable strides in the 5G domain.

- According to ITA, China continues to dominate the global automotive landscape, leading in annual sales and manufacturing output. Projections indicate domestic vehicle production could reach 35 million by 2025. Furthermore, bolstered by a robust manufacturing base, China's automotive industry amplified its global presence, with exports soaring 81% year-on-year, totaling 1.76 million vehicles in the initial five months of 2023, as reported by the China Association of Automobile Manufacturers (CAAM). Given this development prowess, the demand for analog ICs in modern Chinese industries is anticipated to be substantial.

Analog Integrated Circuit (IC) Industry Overview

- The analog Integrated Circuit (IC) market forecast indicates a semi-consolidated landscape. Manufacturers are committed to fierce competition, leveraging product innovation and technological differentiation. Many companies strategically invest in developing analog ICs to secure a first-mover advantage and maintain competitiveness. Notable players in this arena include Analog Devices Inc., Infineon Technologies AG, Microchip Technology Inc., NXP Semiconductors NV, and ON Semiconductor.

- Recent advancements in analog ICs have centred on enhancing performance while curbing power consumption. A notable stride has been in mixed-signal ICs, which merge analog and digital circuits onto a single chip.

- This integration paves the way for intricate and efficient systems, especially for applications like data converters and sensor interfaces. Additionally, advanced fabrication technologies, including silicon-germanium (SiGe) and silicon-on-insulator (SOI), have been harnessed to elevate analog circuit performance.

- Looking ahead, there's a pronounced shift towards integrating analog and digital circuits at the system level, moving beyond the confines of the IC level. This change, termed system-on-a-chip (SoC) technology, promises more efficient and cost-effective devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 63830

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro Economic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Penetration of Smartphones, Feature Phones, and Tablets

- 5.2 Market Challenges

- 5.2.1 Increasing Design Complexity of Analog IC

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 General-Purpose IC

- 6.1.1.1 Interface

- 6.1.1.2 Power Management

- 6.1.1.3 Signal Conversion

- 6.1.1.4 Amplifiers/Comparators (Signal Conditioning)

- 6.1.2 Application-Specific IC

- 6.1.2.1 Consumer

- 6.1.2.1.1 Audio/Video

- 6.1.2.1.2 Digital Still Camera and Camcorder

- 6.1.2.1.3 Other Consumers

- 6.1.2.2 Automotive

- 6.1.2.2.1 Infotainment

- 6.1.2.2.2 Other Infotainment

- 6.1.2.3 Communication

- 6.1.2.3.1 Cell Phone

- 6.1.2.3.2 Infrastructure

- 6.1.2.3.3 Wired Communication

- 6.1.2.3.4 Short Range

- 6.1.2.3.5 Other Wireless

- 6.1.2.4 Computer

- 6.1.2.4.1 Computer System and Display

- 6.1.2.4.2 Computer Periphery

- 6.1.2.4.3 Storage

- 6.1.2.4.4 Other Computers

- 6.1.2.5 Industrial and Others

- 6.1.1 General-Purpose IC

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 VENDOR MARKET SHARE ANALYSIS

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Analog Devices Inc.

- 8.1.2 Infineon Technologies AG

- 8.1.3 Microchip Technology Inc.

- 8.1.4 NXP Semiconductors NV

- 8.1.5 ON Semiconductor

- 8.1.6 Richtek Technology Corporation (MediaTek Inc.)

- 8.1.7 Skyworks Solutions Inc.

- 8.1.8 STMicroelectronics NV

- 8.1.9 Renesas Electronics Corporation

- 8.1.10 Texas Instruments Inc.

- 8.1.11 Qorvo Inc.

9 PRICING ANALYSIS OF ANALOG IC MARKET

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.