PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687343

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687343

Pine Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

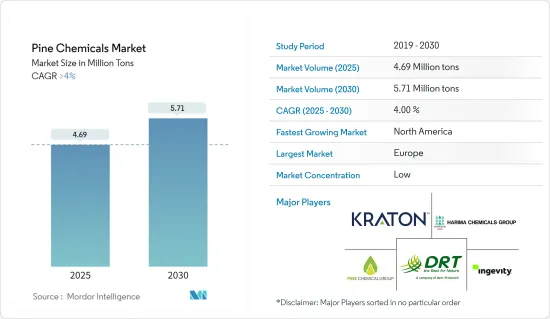

The Pine Chemicals Market size is estimated at 4.69 million tons in 2025, and is expected to reach 5.71 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

COVID-19 has had mixed effects on the pine chemicals market. Initially, demand decreased due to disruptions in supply chains, reduced industrial activity, and lower consumer spending. This led to temporary slowdowns in the production and sales of pine chemicals. However, as the pandemic progressed, there was an increased demand for certain pine-derived products, particularly those used in disinfectants, sanitizers, and pharmaceuticals.

Increasing demand for pine chemicals from the mining sector and the flavors and fragrances industry are the major factors driving the pine chemicals market.

However, an increase in the availability of cheaper substitutes and fluctuations in the price of raw materials are expected to hamper the growth of the pine chemicals market.

The expanding applications of pine chemicals in various end-user industries are expected to unveil new opportunities for the pine chemicals market.

Europe is expected to dominate the pine chemicals market globally, with the most significant consumption coming from countries such as Germany and Italy.

Pine Chemicals Market Trends

The Adhesives and Sealants Segment is expected to Dominate the Market

Pine chemicals, particularly rosin and its derivatives, exhibit excellent tackifying properties, making them ideal ingredients for adhesives and sealants. They enhance the adhesion strength and cohesion of these products, improving their performance and durability.

Pine-derived chemicals are used in a diverse range of adhesives and sealant formulations across industries such as construction, automotive, packaging, woodworking, and electronics. They are utilized in products like pressure-sensitive adhesives, hot-melt adhesives, rubber-based adhesives, and more.

Furthermore, the growth in the construction industry has propelled the consumption of adhesives and sealants, thus propelling the growth of the pine chemicals market. China is one of the world's largest construction markets. According to the National Bureau of Statistics (NBS), the construction industry's business activity index in China rose to 56.9 as of December 2023 from 55.9 in November 2023.

Pine chemicals are the key ingredient in the formulation of sealants used for caulking, joint sealing, and weatherproofing in construction. Tall oil-based sealants offer excellent adhesion to a wide range of substrates such as concrete, masonry, glass, and metal, making them practical for sealing gaps, cracks, and joints in building envelopes, windows, doors, and roofing systems.

India's construction Industry is projected to grow to USD 1.4 trillion by 2025. By 2030, an estimated 600 million people will live in urban centers, resulting in a need for 25 million additional mid- and ultra-luxury units. Under the National Investment Plan (NIP), India has an infrastructure investment budget of USD 1.4 trillion, with 24% of the budget earmarked for renewable energy, roads & highways, urban infrastructure, and 12% for railways.

Thus, the rising application of adhesives and sealants in the automotive and construction industries is expected to boost the market studied in the coming years.

Europe Region to Dominate the Market

Europe has extensive pine forests, particularly in countries like Sweden, Finland, Russia, and the Baltic States. These forests provide a rich source of pine resin, which serves as the raw material for pine chemical production. The availability of abundant and sustainable pine resources gives European producers a competitive advantage in the global market.

European companies cater to a wide range of industries and applications that utilize pine chemicals, including adhesives, sealants, paints, coatings, printing inks, personal care products, pharmaceuticals, and more. The diversity of end-use industries ensures a stable demand for pine chemicals within the region.

Further, pine-derived resins are commonly used as tackifiers in construction adhesives. These adhesives are then used to bond various construction materials, including wood, metal, concrete, and plastics. They provide strong and durable bonds, making them ideal for structural and non-structural applications in construction.

According to the latest estimate published by Eurostat, in December 2023, compared with December 2022, production in construction increased by 1.9% in the euro area and by 2.4% in Europe.

Germany is one of Europe's largest producers of general rubber goods (GRG) and tires. Continental AG, Dunlop GmbH, Michelin Tire Werke AG & Co. KGaA, Pirelli Deutschland GmbH, and Freudenberg Group are some of the significant manufacturers of tire and non-tire products in the country.

According to the estimate released by the Statistisches Bundesamt in June 2023, as of 2022, the turnover of the construction industry in Germany was higher than that of any civil engineering or specific construction sector. The highest turnover in civil engineering activities was for road and railway construction, at more than EUR 21 billion (USD 22.83 billion), and utility projects, which amounted to EUR 12 billion (USD 13.04 billion).

Thus, the factors mentioned above are expected to drive the market demand for pine chemicals, mainly from the European region.

Pine Chemicals Industry Overview

The pine chemicals market is fragmented, with the top five players accounting for a significant market share. The major players in the market (not in any particular order include) KRATON CORPORATION, Ingevity Corporation, DRT, Harima Chemicals Group Inc., and Pine Chemical Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Pine Chemicals in Mining and Flotation Chemicals and Lubricants

- 4.1.2 Increasing Demand from the Flavors and Fragrances Industry

- 4.2 Restraints

- 4.2.1 Diversion of CTO to Biofuels due to Government Incentives

- 4.2.2 Increase in the Availability of Cheaper Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Threat of New Entrants

- 4.4.3 Threat of Substitute Products and Services

- 4.4.4 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Tall Oil

- 5.1.1.1 Crude Tall Oil (CTO)

- 5.1.1.2 Tall Oil Fatty Acid (TOFA)

- 5.1.1.3 Distilled Tall Oil (DTO)

- 5.1.1.4 Tall Oil Pitch (TOP)

- 5.1.2 Rosin

- 5.1.2.1 Tall Oil Rosin

- 5.1.2.2 Gum Rosin

- 5.1.2.3 Wood Rosin

- 5.1.3 Turpentine

- 5.1.3.1 Gum/Wood Turpentine

- 5.1.3.2 Crude Sulphate Turpentine

- 5.1.3.3 Other Turpentines

- 5.1.4 Application

- 5.1.4.1 Adhesives and Sealants

- 5.1.4.2 Coatings

- 5.1.4.3 Printing Inks

- 5.1.4.4 Lubricants and Lubricity Additives

- 5.1.4.5 Biofuels

- 5.1.4.6 Paper Sizing

- 5.1.4.7 Rubber

- 5.1.4.8 Soaps and Detergents

- 5.1.4.9 Other Applications (Oil Field Chemicals, Chemical additives, Chewing Gums, and Food Additives)

- 5.1.1 Tall Oil

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles(Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Arakawa Chemical Industries Ltd

- 6.4.2 DRT (Derives Resiniques et Terpeniques)

- 6.4.3 Forchem Oyj

- 6.4.4 Harima Chemicals Group Inc.

- 6.4.5 Ingevity Corporation

- 6.4.6 Kraton Corporation

- 6.4.7 Mercer International

- 6.4.8 OOO Torgoviy Dom Lesokhimik

- 6.4.9 Pine Chemical Group

- 6.4.10 Respol Resinas SA

- 6.4.11 Sunpine AB

- 6.4.12 Synthomer Plc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Pine Chemicals (DTO, TOFA, CTO, TOP, and Wood Rosin)

- 7.2 Food and Packaging Safety Regulations of Adhesives and Sealants