PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687161

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687161

Europe Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

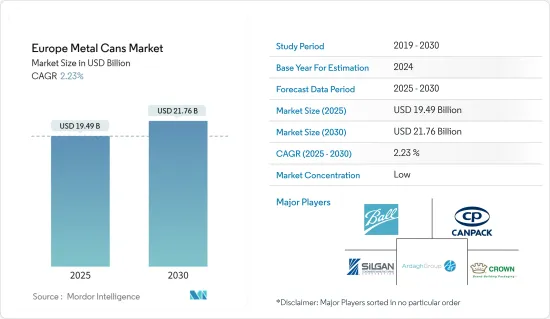

The Europe Metal Cans Market size is estimated at USD 19.49 billion in 2025, and is expected to reach USD 21.76 billion by 2030, at a CAGR of 2.23% during the forecast period (2025-2030).

Key Highlights

- The food and beverage sector's robust European demand propels the metal cans market. Widely utilized for packaging carbonated drinks, beer, energy drinks, and canned foods like soups and vegetables, metal cans boast advantages such as extended shelf life, protection from light and air, and transport ease. With the rising popularity of convenient ready-to-eat meals and beverages, this sector's steady growth is still strong.

- A surging demand for sustainable packaging is driving the market's expansion. Aluminum cans, being highly recyclable, resonate with the mounting consumer and regulatory push to curb plastic waste. Europe, boasting one of the world's highest recycling rates for aluminum cans, positions these cans as the top choice for companies aiming to uphold environmental standards. Furthermore, stringent European regulations on packaging waste and sustainability are nudging businesses towards eco-friendly solutions, bolstering the metal cans market.

- Beyond sustainability, there's a notable pivot towards premium packaging. Brands are leveraging metal cans for their practicality and as a marketing tool. Thanks to advancements in printing and design, brands can craft visually striking cans that capture attention on shelves. This is particularly evident in the beverage sector, where eye-catching cans enhance product visibility and convey brand identity. Additionally, the rising trend of health-conscious, ready-to-drink beverages amplifies the demand for metal cans.

- European manufacturers, including Ardagh Group, Ball Corporation, and Crown Holdings, dominate the production and distribution of metal cans. These companies source raw materials from global suppliers, primarily aluminum and steel, and trade their finished products in international markets. Europe is a significant hub for importing and exporting metal cans, mainly driven by demand from the beverage industry.

- However, the European metal cans market grapples with challenges, including volatile raw material prices and stiff competition from alternatives like plastic bottles and cartons. The energy-intensive nature of aluminum manufacturing raises environmental concerns. Nevertheless, Europe's strong recycling infrastructure and a persistent demand for sustainable, convenient, and premium packaging bodes well for the market's continued growth.

Europe Metal Cans Market Trends

Alcoholic Beverages to Register Significant Growth Rate

- In Europe, the demand for metal cans in the alcoholic beverage sector has increased steadily due to consumers' growing preference for convenience and portability. Cans are lighter and more durable than glass bottles, making them easier to transport and store. This advantage is significant for outdoor events, festivals, and on-the-go consumption in urban areas. As consumers, particularly younger demographics, prioritize convenience, the market for canned alcoholic beverages, including beer, cider, and ready-to-drink cocktails, continues to expand. Metal cans provide a practical packaging solution for these products, driving their adoption across the European alcoholic beverage market.

- Sustainability concerns significantly influence the demand for metal cans in Europe. Consumer awareness of environmental issues has increased the preference for eco-friendly packaging. Aluminum cans are recyclable, and the region maintains one of the highest aluminum recycling rates globally. As European governments implement stricter regulations on plastic packaging and waste management, alcoholic beverage brands are adopting metal cans as a sustainable solution. This shift aligns with consumer demand for environmentally responsible products and packaging, making metal cans advantageous for producers and consumers.

- The premiumization trend in Europe contributes to the increased demand for metal cans in the alcoholic beverage market. The growth of craft beers, hard seltzers, and premium ready-to-drink cocktails has prompted manufacturers to use high-quality aluminum cans with refined designs. Printing and decoration technology improvements enable vibrant and customized packaging that enhances brand visibility and product differentiation. As consumers seek premium experiences, brands use metal cans to demonstrate quality and innovation, supporting European market growth.

- The emergence of health-conscious drinking in Europe affects metal can demand. Low-alcohol, low-calorie, and alcohol-free beverages, including hard seltzers, functional drinks, and alcohol-free beers, have gained popularity. Due to their convenience and lightweight properties, these beverages frequently use metal can packaging. As health trends continue to influence the European alcoholic beverage market, metal cans serve as an effective packaging solution for these emerging products, increasing their market presence in the region.

- The beer sales volume in Germany increased from 5,336.34 thousand hectoliters in March 2024 to 6,768.34 thousand hectoliters in May 2024, driving the demand for metal cans in the packaging market. The beer market growth, particularly during the spring and summer, increases the requirement for packaging solutions that provide convenience, durability, and sustainability. Metal cans, specifically aluminum cans, are preferred for beer packaging due to their lightweight nature, recyclability, and ability to preserve beverage quality.

- The increasing beer sales volumes in Germany correspond with market trends supporting metal can demand. Consumer preferences for portable and convenient beverage packaging make cans an efficient and cost-effective option for manufacturers and consumers. The increase in beer sales during outdoor events and festivals requires packaging solutions that ensure product integrity during transport and handling. Metal cans effectively meet these requirements, making them a primary choice for beer producers and suppliers in Germany.

United Kingdom to Hold Significant Market Share

- The metal can packaging market in the UK continues to expand, particularly in the beverage sector, with growth across beer, soft drinks, energy drinks, and ready-to-drink cocktails. Aluminum cans have emerged as a primary packaging option for many brands due to their lightweight properties, recyclability, and product preservation capabilities. These characteristics align with UK consumer preferences for portable and environmentally responsible packaging.

- Consumer demand for sustainable packaging has significantly influenced the adoption of metal cans in the UK. Implementing environmental regulations targeting plastic waste reduction has positioned aluminum cans as a viable alternative. The infinite recyclability of cans supports the UK's circular economy objectives. Government policies, including the Plastic Packaging Tax and Extended Producer Responsibility (EPR) schemes, have encouraged companies to adopt metal can packaging. The UK's net zero emissions target by 2050 reinforces the market potential for sustainable packaging options like metal cans over glass and plastic alternatives.

- Health and wellness trends have also influenced the rise of metal can packaging in the UK. Consumers increasingly seek low-alcohol, low-calorie, and functional beverages like hard seltzers, kombucha, and fitness-focused drinks. These products are often packaged in cans, which consumers perceive as convenient and environmentally responsible. The lightweight nature of cans, combined with their recyclability, appeals to health-conscious individuals seeking products that complement their active lifestyles while supporting sustainability. The packaging maintains beverage freshness and carbonation, which is particularly important for products like hard seltzers and craft beers.

- The craft beer movement and premiumization of alcoholic beverages in the UK have increased demand for high-quality metal can packaging. Craft breweries and boutique producers select cans for their practicality and capacity to showcase innovative designs and branding. Metal cans enable vibrant, custom graphics and detailed artwork that appeal to design-conscious consumers. Aluminum cans preserve craft beer quality by protecting against light and oxygen exposure. This combination of product preservation and design capabilities has established cans as a preferred packaging choice for premium beverages, supporting metal can market growth in the UK.

- The high retail sales revenue of major energy drink brands in the UK, including Red Bull (USD 510.73 million), Monster (USD 444.53 million), and Lucozade (USD 285.07 million), drives the demand for metal can packaging. These companies choose metal cans for their convenience, portability, and ability to maintain product freshness and carbonation, which suits consumer preferences for on-the-go consumption. The recyclability of aluminum cans also attracts environmentally conscious consumers. Both premium and value brands, such as Prime and Euro Shopper, are adopting metal can packaging to improve product presentation and meet sustainability requirements, indicating continued growth in metal can demand within the energy drink market.

- The metal can packaging trend in the UK is driven by a convergence of factors, including sustainability, convenience, consumer demand for healthier drinks, and the premiumization of alcoholic beverages. With aluminum cans offering a recyclable, efficient, and consumer-friendly solution, their popularity is likely to continue rising across various beverage categories. As consumer preferences shift toward more eco-conscious and convenient packaging, the metal can market in the UK is poised for sustained growth, fueled by design, functionality, and sustainability innovations.

Europe Metal Cans Industry Overview

The European metal cans market is fragmented, with multiple companies operating in the region. Major players include Ball Corporation, Ardagh Group S.A., Crown Holdings, Inc., and Silgan Holdings Inc. These companies compete for market share through various strategic initiatives. Mergers and acquisitions help companies expand their geographical presence and production capabilities.

Companies strengthen their supply chain networks and enhance their market position through collaborations. Product innovations enable companies to meet evolving consumer demands and maintain competitive advantages in the market. Companies also focus on sustainability initiatives and technological advancements to differentiate themselves from competitors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of Macro-economic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Sustainability Gains Importance, Metal Cans Shine with Their High Recyclability

- 5.2 Market Challenge

- 5.2.1 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By Type

- 6.2.1 Food Cans

- 6.2.1.1 Vegetables

- 6.2.1.2 Fruits

- 6.2.1.3 Pet Food

- 6.2.1.4 Soups and Condiments

- 6.2.1.5 Other Food Cans (Baby Food, Dairy, Fruit/Vegetable Juices, Seafood, and Meat and Poultry Cans)

- 6.2.2 Beverage Cans

- 6.2.2.1 Alcoholic

- 6.2.2.2 Non-Alcoholic

- 6.2.3 Aerosol Cans

- 6.2.3.1 Personal care and Cosmetics

- 6.2.3.2 Household and Homecare

- 6.2.3.3 Other Aerosol Cans

- 6.2.4 Other Cans

- 6.2.1 Food Cans

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Spain

- 6.3.5 Italy

- 6.3.6 Poland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ball Corporation

- 7.1.2 Ardagh Group

- 7.1.3 Crown Holdings, Inc.

- 7.1.4 Silgan Holdings Inc.

- 7.1.5 CAN-PACK SA

- 7.1.6 Massilly Holding SAS

- 7.1.7 Tecnocap Group

- 7.1.8 Tata Europe Ltd

- 7.1.9 ASA Group

- 7.1.10 Eurobox Metal Packaging

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET