Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687128

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687128

Optical Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 180 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

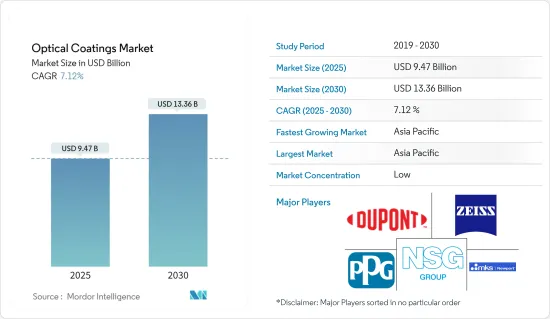

The Optical Coatings Market size is estimated at USD 9.47 billion in 2025, and is expected to reach USD 13.36 billion by 2030, at a CAGR of 7.12% during the forecast period (2025-2030).

Key Highlights

- Over the short term, increasing demand for optical coatings from the solar industry and technological advancements in the optical coatings process are expected to drive the market.

- High costs and some limiting properties of optical coatings are expected to hinder the market's growth.

- The upcoming demand for electric vehicles is likely to create opportunities for the market in the coming years.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR during the forecast period.

Optical Coatings Market Trends

The Electronics and Semiconductors Segment is Expected to Dominate the Market

- Optical coatings play a pivotal role in electronic applications, ensuring light seamlessly passes through optical surfaces. With the surging demand for cutting-edge electronic devices such as smartphones, tablets, and wearables, the appetite for premium optical coatings has surged. These coatings not only bolster the performance of electronic displays but also enhance their durability.

- Transparent conductive coatings find their place in electronic displays as well. The market in focus is buoyed by the relentless growth in demand for consumer electronics. As devices shrink in size and become more compact, the need for adept optical coatings grows. These coatings adeptly manage heat, mitigate glare, and elevate the optical clarity of smaller components.

- The semiconductor industry prioritizes precise, high-performance optical coatings. Integral to photolithography-a cornerstone of semiconductor fabrication-these coatings amplify the efficiency and quality of semiconductor devices. With the rising influence of IoT across diverse sectors, semiconductor demand has surged, subsequently propelling the optical coatings market.

- For instance, data from the Japan Electronics and Information Technology Industries Association (JEITA) highlighted that in 2023, Japan's electronics sector achieved a production value nearing JPY 10.7 trillion Japanese (~USD 76 billion). Encompassing consumer electronics, industrial equipment, and myriad electronic components, the industry is projected to touch USD 3.68 trillion by 2024, marking a commendable 9% Y-o-Y growth.

- World Semiconductor Trade Statistics reported on December 31, 2023, that the global semiconductor market was valued at USD 526.89 billion in 2023, with a promising 16.0% growth anticipated in 2024.

- Data from ZVEI in July 2024 indicates that Germany's electronic and digital sector achieved a turnover of EUR 238 billion (USD 259.28 billion) in 2023, reflecting a robust 10% growth from the previous year.

- Given these dynamics, the market is poised for significant movements in the foreseeable future.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is likely to lead the optical coatings market during the forecast period. Leading countries such as China, Japan, India, and South Korea are showcasing a surge in demand for optical coatings across various sectors, including electronics, semiconductors, aerospace, and defense.

- Data from the Civil Aviation Administration of China (CAAC) on July 12, 2024, revealed that passenger traffic in the first half of 2024 exceeded USD 350 million, marking a 23.5% Y-o-Y increase and a 9% rise from the same period in 2019.

- Furthermore, a report by Aviation A2Z in December 2023 highlighted that China would acquire 17 domestically manufactured aircraft (COMAC), with deliveries scheduled over the next two years, further bolstering the demand for optical coatings.

- As per the India Brand Equity Foundation (IBEF), India ranks fourth globally in renewable energy, wind power, and solar power capacity in 2024. The Annual 2023 India Solar Market Update noted that by the end of December 2023, India's cumulative solar capacity reached approximately 135 GW, with projections of hitting around 170 GW by March 2025.

- IBEF also highlighted that bolstered by government support and favorable economics, the renewable sector has become a magnet for investors. With an eye on self-sufficiency, India aims to meet its energy demand, which is projected to hit 15,820 TWh by 2040.

- The Japan Electronics and Information Technology Industries Association (JEITA) reported that in 2023, electronic components and devices contributed approximately JPY 6.97 trillion (USD 47 billion) to the nation's electronics industry, which boasted a total production value of around JPY 10.7 trillion (USD 76 billion).

- Given these dynamics, the optical coatings market in Asia-Pacific is set for steady growth during the forecast period.

Optical Coatings Industry Overview

The optical coatings market is highly fragmented in nature. Some of the key players in the market (not in any particular order) include DuPont, Zeiss International, Newport Corporation, PPG Industries Inc., and Nippon Sheet Glass Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 55454

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Solar Industry

- 4.1.2 Technological Advancements in the Optical Coatings Process

- 4.2 Restraints

- 4.2.1 High Costs and Some Limiting Properties of Optical Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Product Type

- 5.1.1 Optical Filter Coatings

- 5.1.2 Anti-reflective Coatings

- 5.1.3 Transparent Conductive Coatings

- 5.1.4 Mirror Coatings (High Reflective)

- 5.1.5 Beam Splitter Coatings

- 5.1.6 Other Product Types (Temperature Management Coatings)

- 5.2 By Technology

- 5.2.1 Chemical Vapor Deposition

- 5.2.2 Ion-beam Sputtering

- 5.2.3 Plasma Sputtering

- 5.2.4 Atomic Layer Deposition

- 5.2.5 Sub-wavelength Structured Surfaces

- 5.3 By End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Electronics and Semiconductors

- 5.3.3 Telecommunications

- 5.3.4 Healthcare

- 5.3.5 Solar

- 5.3.6 Automotive

- 5.3.7 Other End-user Industries (Military and Defense and Medical)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Qatar

- 5.4.5.4 United Arab Emirates

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Abrisa Technologies

- 6.4.3 AccuCoat inc.

- 6.4.4 Artemis Optical Ltd

- 6.4.5 Edmund Optics Inc.

- 6.4.6 DuPont

- 6.4.7 Inrad Optics

- 6.4.8 Materion Corporation

- 6.4.9 Newport Corporation

- 6.4.10 Nippon Sheet Glass Co. Ltd

- 6.4.11 Optical Coatings Technologies

- 6.4.12 PPG Industries Inc.

- 6.4.13 Quantum Coating Inc.

- 6.4.14 Reynard Corporation

- 6.4.15 SIGMAKOKI CO. LTD

- 6.4.16 Schott AG

- 6.4.17 Zeiss International

- 6.4.18 Zygo

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Upcoming Demand from Electric Vehicles

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.