PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907231

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907231

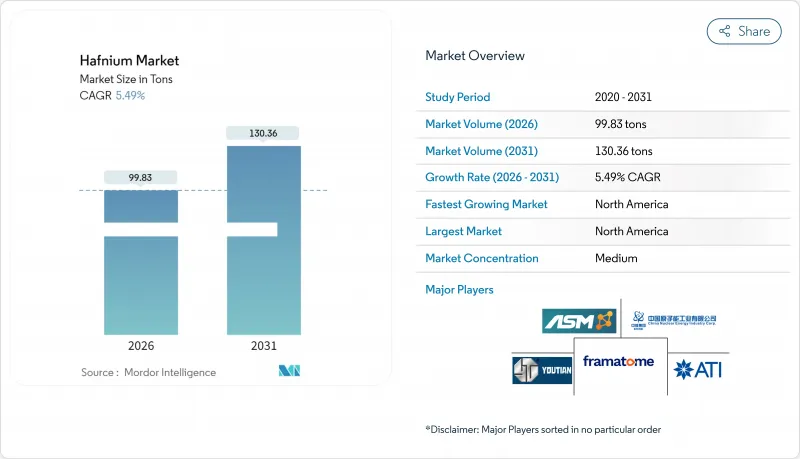

Hafnium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Hafnium market size in 2026 is estimated at 99.83 tons, growing from 2025 value of 94.63 tons with 2031 projections showing 130.36 tons, growing at 5.49% CAGR over 2026-2031.

This growth momentum flows from three converging forces: shrinking transistor gate dimensions in leading-edge chips, aerospace demand for ultra-high-temperature materials, and nuclear fleet upgrades that require neutron-absorbing control rods. Superalloys that replace rhenium with hafnium, the march toward 3-nm logic nodes, and strategic stockpiling by reactor operators collectively widen demand. On the supply side, refined output is confined to a handful of facilities, reinforcing an oligopolistic structure that compounds geopolitical risk and pricing power. France's Framatome, the United States' ATI, Chinese refiners, and Russian suppliers together deliver only 70-75 tons of primary product annually, leaving downstream users exposed to tariff shifts and export controls.

Global Hafnium Market Trends and Insights

Surging Demand for High-κ Dielectric Hafnium Oxides in 3-nm and Below Logic Nodes

Chipmakers are shifting from silicon dioxide to hafnium oxide gate dielectrics because the older material cannot suppress leakage when oxide thickness drops below 1 nm. Patents filed by Taiwan Semiconductor Manufacturing Company illustrate how hafnium oxide layers paired with lanthanum oxide extend planar scaling and enable continued progress toward 2-nm nodes slated for 2026. Beyond conventional transistors, ferroelectric hafnium-zirconium oxide films deliver dielectric permittivity above 900, opening doors for low-power embedded memory and capacitor architectures. These breakthroughs anchor an essential pathway for sustaining Moore's Law, driving steady growth for the hafnium market worldwide.

Rapid Scale-up of Reusable Launch Vehicles Using Ultra-High-Temperature Ceramics

Reusable launch systems subject leading-edge tiles and rocket throat inserts to repeated re-entry cycles exceeding 2,000 °C. Hafnium carbide, with a melting point near 3,890 °C, offers unmatched oxidation resistance, as validated through laser-heating studies at Imperial College London. Carbon-carbon composites doped with more than 5.7% hafnium carbide cut ablation losses nearly in half, extending component life in launch vehicles. As commercial and defense programs accelerate sortie rates, procurement managers are embedding hafnium ceramics into nose cones, control surfaces, and engine liners, pulling incremental tons into the hafnium market.

Supply Bottlenecks from Zirconium Co-production Dependency

Hafnium emerges only when zirconium intermediates are processed, typically at a 50:1 mass ratio, making capacity additions hostage to zirconium economics. Since zirconium ore reserves reside mainly in South Africa, Australia, and Mozambique, supply shocks in mineral sands cascade into hafnium availability. With separation plants limited to France, the United States, China, and Russia, any outage or policy shift quickly tightens global balances. Capital intensity further restricts new entrants, perpetuating concentration in the hafnium market.

Other drivers and restraints analyzed in the detailed report include:

- Strategic Stockpiling by Nuclear-Fleet Operators Amid Fuel Diversification

- Aerospace Superalloy Substitution for Rhenium Under Cost Inflation Pressure

- Volatile Price Spikes Driven by China-Centric Refining Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The carbide category captured 48.20% of 2025 volumes, thanks to its unmatched melting point and proven use in rocket throat inserts and hypersonic leading edges. This dominance accounts for nearly half of the hafnium market size allocated to material types. Although nitrided derivatives promise even lower ablation losses, foundational demand remains anchored in pure hafnium carbide. The global hafnium market, therefore, leans on carbide stability for baseline tonnage.

Hafnium oxide is charting the fastest 6.05% CAGR to 2031 as fab lines transition to 3-nm and move toward 2-nm production. Gate-stack adoption, ferroelectric memory prototypes, and capacitor innovations lift oxide volumes well above historical baselines. The segment's trajectory hints at a growing slice of hafnium market share across the forecast horizon, especially as chip revenue aims toward USD 1 trillion by decade-end. Fabricators now specify parts-per-trillion impurity thresholds, putting a premium on suppliers able to deliver electronics-grade oxide.

The Hafnium Report is Segmented by Type (Hafnium Oxide, Hafnium Carbide, and Other Types), Application (Super Alloy, Optical Coating, Nuclear, Plasma Cutting, and Other Applications), and Geography (Asia-Pacific, North America, Europe, and Rest of the World). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

North America controlled 38.55% of global demand in 2025, the largest share by region, and is on course for a 5.66% CAGR through 2031 despite limited indigenous production. ATI's Oregon and Utah operations produce specialty alloys, yet U.S. buyers still sourced 42% of imports from Germany, 29% from France, and 24% from China during 2017-20. Boeing's civil airframe programs, defense turbine overhaul schedules, and Intel's advanced fabs anchor consumption growth in the hafnium market.

Europe wields strategic leverage through France's Jarrie refinery, which holds roughly 43% of refined capacity and turns out nearly 30 tons per year. Airbus, Safran, and Rolls-Royce rely on this domestic supply, while Germany's historical role as the leading exporter to the United States highlights the region's processing specialization. Recent French export fees have tightened trans-Atlantic trade, but intra-EU demand remains steady amid aircraft backlog and rising reactor maintenance cycles.

Asia-Pacific's uptake accelerates as Japan and South Korea boost nuclear output and semiconductor lines. China's dual status as both producer and rising consumer introduces supply friction, since domestic fabs and launch-vehicle builders increasingly capture oxide and carbide volumes. Taiwan's leadership in 3-nm logic adoption and Vietnam's rare-earth development underscore the region's growing self-sufficiency aspirations. Overall, regional diversity in end uses, from control rods in fast reactors to thermal tiles on reusable rockets, keeps the hafnium market outlook constructive across Asia-Pacific.

- ACI Alloys

- American Elements

- ATI

- Australian Strategic Materials Ltd

- Baoji ChuangXin Metal Materials Co. Ltd (CXMET)

- China Nuclear JingHuan Zirconium Industry Co., Ltd

- CMP JSC

- Framatome (EDF)

- Nanjing Youtian Metal Technology Co.,Ltd

- Phelly Materials Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for high-κ dielectric hafnium oxides in 3-nm and below logic nodes

- 4.2.2 Rapid scale-up of reusable launch vehicles using hafnium-based ultra-high-temperature ceramics

- 4.2.3 Strategic stock-piling by nuclear-fleet operators amid fuel diversification

- 4.2.4 Aerospace super-alloy substitution for rhenium under cost-inflation pressure

- 4.3 Market Restraints

- 4.3.1 Supply bottlenecks from zirconium co-production dependency

- 4.3.2 Volatile price spikes driven by China-centric refining capacity

- 4.3.3 Difficulties in Seperation and Extraction

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Price Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Hafnium Oxide

- 5.1.2 Hafnium Carbide

- 5.1.3 Other Types (including Hafnium Metal)

- 5.2 By Application

- 5.2.1 Super Alloy

- 5.2.2 Optical Coating

- 5.2.3 Nuclear

- 5.2.4 Plasma Cutting

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Production Analysis

- 5.3.1.1 France

- 5.3.1.2 United States

- 5.3.1.3 China

- 5.3.1.4 Rest of the World

- 5.3.2 Consumption Analysis

- 5.3.2.1 Asia-Pacific

- 5.3.2.1.1 China

- 5.3.2.1.2 India

- 5.3.2.1.3 Japan

- 5.3.2.1.4 Rest of Asia-Pacific

- 5.3.2.2 North America

- 5.3.2.2.1 United States

- 5.3.2.2.2 Rest of North America

- 5.3.2.3 Europe

- 5.3.2.3.1 France

- 5.3.2.3.2 Germany

- 5.3.2.3.3 Russia

- 5.3.2.3.4 Rest of Europe

- 5.3.2.4 Rest of the World

- 5.3.2.1 Asia-Pacific

- 5.3.1 Production Analysis

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ACI Alloys

- 6.4.2 American Elements

- 6.4.3 ATI

- 6.4.4 Australian Strategic Materials Ltd

- 6.4.5 Baoji ChuangXin Metal Materials Co. Ltd (CXMET)

- 6.4.6 China Nuclear JingHuan Zirconium Industry Co., Ltd

- 6.4.7 CMP JSC

- 6.4.8 Framatome (EDF)

- 6.4.9 Nanjing Youtian Metal Technology Co.,Ltd

- 6.4.10 Phelly Materials Inc.

7 Market Opportunities and Future Outlook

- 7.1 Reusable spacecraft heat-shield tiles

- 7.2 Hafnium oxide nanoparticles as radiosensitizers

- 7.3 White-space and Unmet-need Assessment