Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685902

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685902

Europe Commercial Aircraft Cabin Interior - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 167 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

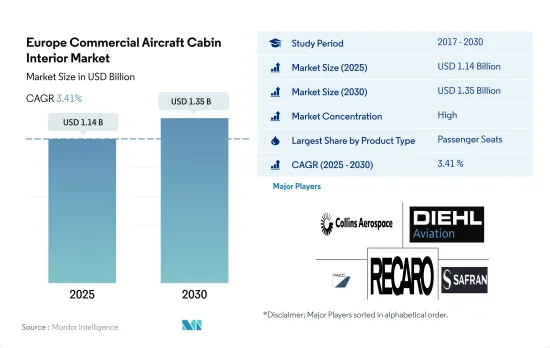

The Europe Commercial Aircraft Cabin Interior Market size is estimated at 1.14 billion USD in 2025, and is expected to reach 1.35 billion USD by 2030, growing at a CAGR of 3.41% during the forecast period (2025-2030).

European airlines are new technologies in the aircraft cabin interiors that are expected to aid in new product developments and innovations in the segment

- The European commercial aircraft cabin interior market has been segmented into seats, cabin lighting, in-flight entertainment systems, windows, galley, lavatories, and other product types. The airline companies in the region are emphasizing increasing the utility of these products while improving the overall passenger comfort and experience.

- An enhanced seating structure with more developed space than economy-class seats is becoming highly essential due to the rising preferences for business-class travelers. European airline operators and OEMs are increasing their efforts to reduce weight and develop a sustainable way to manage the airline industry, considering the zero-emission 2050 goal.

- Airlines are focusing on modernized cabins with advanced interior lighting to improve the passenger experience. The widespread adoption of LED ambient lighting technology on next-generation aircraft has enabled cabin modernization activities to maintain a consistent service quality on board. Airlines in the region are moving toward advanced LED lighting as it helps the airlines eliminate various drawbacks of existing interior cabin lights in terms of efficiency, reliability, durability, and weight. Various OEMs possess advanced LED lighting over conventional aircraft cabin lights.

- Major European carriers, such as Air Europa, Air France, British Airways, and Iberia Airlines, improved their in-flight entertainment systems in terms of screen quality and features. Around 2,500 passenger aircraft are expected to be delivered in the region during 2023-2030. The surge in aircraft procurement numbers is expected to boost the demand for commercial aircraft cabin interior products in the European passenger aviation sector during the forecast period.

The proliferation of low-cost carriers and the need for enhanced passenger cabin experiences are expected to aid the market's growth

- Cabin interiors in aircraft have evolved into a prominent component of the overall passenger experience. European airline companies are now focusing on modernized cabins to improve the passenger experience.

- The increase in air passenger traffic is driving the demand for new aircraft procurements, further boosting the cabin interior market. For instance, in 2022, air passenger traffic in the whole of Europe amounted to 1.3 billion, a growth of 8% compared to 2021. Airline companies in Europe are implementing fleet expansion plans to cater to the growing air passenger traffic in the major countries. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in the region. Hence, the growing air passenger traffic is expected to generate demand for new aircraft in these countries compared to other European countries.

- The increasing air passenger traffic may eventually boost aircraft orders and deliveries. The major commercial aircraft manufacturing OEMs, i.e., Boeing and Airbus, are expected to deliver a large number of aircraft in the region over the forecast period. Over 2,800 new jets are expected to be delivered to the region. Of these, 2,500+ are expected to be narrowbody aircraft, primarily due to the preference for economical smaller aircraft, the success of LCCs, and the introduction of long-range narrowbody aircraft. The major airline companies in the region, such as Air France, British Airways, and Lufthansa, are focusing on improving the overall passenger experience in the aircraft, thus aiding the demand for commercial aircraft cabin interior products in the region.

Europe Commercial Aircraft Cabin Interior Market Trends

The growth in air passenger traffic is expected to be supported by the increasing demand for domestic and international air travel

- The gradual relaxation of travel restrictions in various European countries in 2022 made travel within the continent much easier than during the COVID-19 pandemic. Due to this trend, international demand soared, with passengers unable to travel during the lockdowns eager to fly abroad once again instead of taking domestic vacations. In 2022, air passenger traffic in the whole of Europe reached 1.3 billion, a growth of 8% compared to 2021. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in Europe and, hence, may generate more demand for new aircraft compared to other European countries over the coming years. European airlines have also been responsible for carrying almost 40% of global international air passengers.

- European airport traffic grew by 247% in the first six months of 2022 compared to 2021, resulting in an additional 660 million passengers handled across the continent. The United Kingdom, the Netherlands, Turkey, and Germany, which have some of the countries with the busiest airports, recorded a significant rise in passenger traffic in H1 2022. In August 2022, passenger traffic in the top five European airports increased by 68.1% but remained -17.5% below pre-pandemic August 2019 levels, mainly due to continued travel restrictions in Asia. A similar increase in air passenger traffic was observed at airports in the Rest of Europe in August 2022. Commercial air traffic declined from Ukrainian airports, and airports in Belarus and Russia recorded declining passenger volumes as well since the beginning of the Russia-Ukraine War. The air passenger traffic is expected to surge by 31% during 2023-2030, with increased demand in domestic and international aviation.

The economic development initiatives implemented in the European Union are expected to aid the GDP per capita income growth

- The European region had the second-highest GDP, with USD 17 trillion, in 2022. Out of the total region's GDP, the Netherlands recorded the highest growth rate, i.e., 19%. In contrast, other major countries such as France and Germany accounted for growth rates of 10% and 14%, respectively. Out of the total GDP, the air transport industry in the United Kingdom contributed around USD 87 billion annually, while France and Germany contributed around USD 86 billion and USD 68 billion, respectively.

- The GDP per capita income of the overall European Union was around USD 39,000 in 2023. The per capita GDP of the region's major economies, including the UK, France, and Germany, has returned to pre-pandemic levels. The GDP per capita income of the UK, Germany, and France surged by around 15%, 9%, and 7%, respectively, in 2022 as compared to 2019. The peak of the cohesion policy programs for the 2014-2020 period, in parallel to the start of the programs for the 2021- 2027 period, ensures a constant flow of investment into people and businesses across the region. Since the COVID-19 pandemic, more than EUR 186 billion has been paid out through cohesion policy programs to enhance resilience and social and regional growth. The penetration of air travel is correlated with the GDP per capita. Countries with higher GDP per capita tend to have higher numbers of airline seats per capita. Germany has the highest GDP per capita in the region at USD 51,100, which increased by 14% from 2017 to 2022. France's GDP per capita increased by 12% from 2017 to 2022, while that of the United Kingdom increased by 22% within the same five-year time frame. Such growth instances across major economies and pan-Europe are anticipated to aid the European airline industry during the forecast period.

Europe Commercial Aircraft Cabin Interior Industry Overview

The Europe Commercial Aircraft Cabin Interior Market is fairly consolidated, with the top five companies occupying 68.91%. The major players in this market are Collins Aerospace, Diehl Aerospace GmbH, FACC AG, Recaro Group and Safran (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 49151

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Cabin Lights

- 5.1.2 Cabin Windows

- 5.1.3 In-Flight Entertainment System

- 5.1.4 Passenger Seats

- 5.1.5 Other Product Types

- 5.2 Aircraft Type

- 5.2.1 Narrowbody

- 5.2.2 Widebody

- 5.3 Cabin Class

- 5.3.1 Business and First Class

- 5.3.2 Economy and Premium Economy Class

- 5.4 Country

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Spain

- 5.4.4 Turkey

- 5.4.5 United Kingdom

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Astronics Corporation

- 6.4.2 Collins Aerospace

- 6.4.3 Diehl Aerospace GmbH

- 6.4.4 FACC AG

- 6.4.5 GKN Aerospace Service Limited

- 6.4.6 Jamco Corporation

- 6.4.7 Panasonic Avionics Corporation

- 6.4.8 Recaro Group

- 6.4.9 Safran

- 6.4.10 SCHOTT Technical Glass Solutions GmbH

- 6.4.11 Thales Group

- 6.4.12 Thompson Aero Seating

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.