PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683812

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683812

Climate Change Consulting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

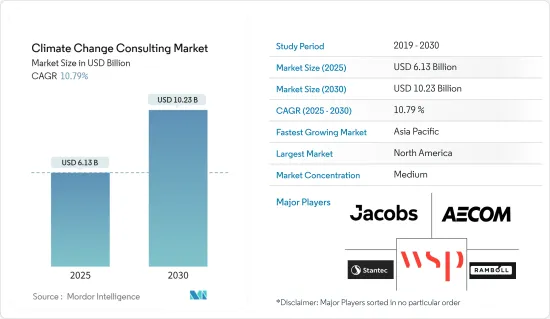

The Climate Change Consulting Market size is estimated at USD 6.13 billion in 2025, and is expected to reach USD 10.23 billion by 2030, at a CAGR of 10.79% during the forecast period (2025-2030).

The Climate Change Consulting market is undergoing rapid growth, spurred by rising environmental concerns and stricter regulatory frameworks. This surge is driven by organizations across industries seeking to align with sustainability goals, reduce greenhouse gas emissions, and manage climate risks.

Key Highlights

- Diverse end-user sectors: The market spans industries like energy and power, manufacturing, mining, and the public sector, all of which require climate resilience planning and environmental risk assessment.

- Consulting firms' role: These firms support companies, governments, and NGOs in adopting decarbonization strategies, mitigating climate risks, and meeting sustainability reporting requirements.

- Pandemic influence: The COVID-19 pandemic initially slowed consulting activities but later accelerated demand for low-carbon transitions, fostering stronger market growth in climate change consulting services.

Carbon Footprint Reduction: A Key Market Driver

One of the most significant drivers of the Climate Change Consulting market is the global focus on carbon footprint reduction and achieving net-zero emissions. This shift is reinforced by increasing regulatory pressures, such as the Net-Zero Government Initiative introduced by the United States at COP27.

Key Highlights

- Government initiatives: The U.S. Net-Zero Government Initiative sets the stage for national emissions reductions by 2050, incentivizing public and private sector collaboration.

- Corporate sustainability goals: Leading firms like GHD are taking steps to meet net-zero targets, guided by initiatives such as the Science Based Targets initiative (SBTi), which helps businesses set verified climate goals.

- Regulatory landscape: The rising importance of compliance with stringent environmental regulations globally drives businesses to seek out consulting services for carbon footprint reduction strategies.

National Goals Driving Market Growth

Governments around the world are setting ambitious climate goals, significantly expanding the market for climate change consulting services.

Key Highlights

- U.S. government funding: In March 2023, the Biden administration allocated USD 250 million to reduce climate pollution and promote clean energy business development.

- Global partnerships: International initiatives like the Global Shield Against Climate Risks, launched at COP27, involve countries providing EUR 210 million to protect vulnerable nations, creating new consulting opportunities.

- China's climate commitments: China's Country Climate and Development Report outlines key sectoral shifts required to meet its climate targets, fostering market growth for consulting services.

Emerging Trends in Climate Change Consulting

A growing focus on carbon footprint analysis, mitigation, and climate adaptation strategies is shaping the future of the Climate Change Consulting market.

Key Highlights

- Footprint assessment demand: Firms like KERAMIDA Inc. are providing comprehensive carbon footprint evaluations for various organizations, including government agencies.

- U.S. government investments: The EPA recently awarded USD 3 million to New Jersey for developing innovative climate strategies, while the DOE invested USD 47 million to support methane mitigation projects.

- Adaptation and resilience: Adaptation strategies are critical, as exemplified by the EPA's 2022 Climate Adaptation Implementation Strategies, reinforcing the need for specialized consulting services in building climate resilience.

- Future Outlook: Opportunities and Challenges : The Climate Change Consulting market offers vast opportunities, but challenges remain as companies and governments attempt to balance ambitious goals with practical implementations.

- Smart city growth: Urbanization and the development of eco-friendly infrastructure projects globally are driving demand for sustainable consulting services.

- Private sector investment: Increasing public and private investments in sustainable buildings and green technologies are pushing the market forward.

- Barriers to adoption: However, some sectors face slower uptake, and gaps between realistic implementation and aspirational climate targets continue to challenge the market.

Climate Change Consulting Market Trends

Energy and Power: Largest End-User Segment

The Energy and Power sector remains the largest consumer of climate change consulting services, holding 29.04% of the market share in 2023, valued at USD 1.32 billion. This sector is expected to grow to USD 2.77 billion by 2029 at a CAGR of 13.11%, driven by regulatory and technological changes.

- Regulatory drivers: Stringent emission policies across the globe are compelling energy companies to seek expert advice on sustainability strategy, decarbonization, and greenhouse gas emissions management.

- Carbon pricing influence: The implementation of carbon pricing and emissions trading schemes is creating a heightened demand for compliance consulting, particularly within energy sectors where emissions are highest.

- Tech advancements: Rapid developments in renewable energy technology and smart grid systems present new opportunities for consultants as firms integrate these innovations into their long-term sustainability plans.

- Corporate investments: Notable investments, such as Deloitte's USD 1 billion in its Sustainability & Climate practice, signal the growing emphasis on climate change mitigation within the energy sector.

Asia-Pacific: Fastest-Growing Regional Segment

The Asia-Pacific region is emerging as the fastest-growing segment for climate change consulting, with a projected CAGR of 15.43% from 2023 to 2028.

- Regional growth leaders: China dominates this segment, holding 35.42% of the Asia-Pacific market share in 2022 and expected to grow at a CAGR of 14.37% by 2028.

- Climate vulnerability: Asia-Pacific's susceptibility to climate change risks like rising sea levels and extreme weather is driving the demand for climate adaptation services across sectors.

- Government initiatives: Countries like Australia are making strong commitments to emissions reduction and renewable energy transitions, further expanding the market for climate change consulting.

- Corporate sustainability: Businesses across the region are increasingly prioritizing ESG reporting and sustainability consulting to address climate-related risks and align with international standards.

Climate Change Consulting Industry Overview

Global Players Dominate a Semi-consolidated Market

The Climate Change Consulting market is characterized by a mix of global conglomerates and specialized niche players. Major industry leaders, such as Jacobs Solutions Inc., WSP Global Inc., and Ramboll Group A/S, command significant market share by leveraging acquisitions and providing comprehensive consulting services.

Strategic acquisitions: ERM's acquisition of Coho and BCG's purchase of Quantis underscore a trend of top players expanding their sustainability expertise through strategic deals.

Fragmentation: The market remains semiconsolidated, with both large-scale players and smaller, specialized consulting firms offering diverse services, from carbon footprint reduction to energy efficiency consulting.

Technological edge: Firms with strong capabilities in data analytics, advanced climate risk modeling, and sector-specific climate policy advisory services are emerging as leaders in this competitive landscape.

Global market share: North America holds 44.23% of the market, with heightened demand for services driven by a robust economy and a well-developed regulatory framework supporting sustainability initiatives.

Factors for Future Success in the Evolving Market

To thrive in the climate change consulting market, players will need to focus on innovation, regulatory expertise, and sector-specific sustainability strategies.

Technology investment: Deloitte's USD 1 billion investment in sustainability services highlights the importance of technological advancements for future success in the industry.

Sector-specific knowledge: Consulting firms with deep expertise in industry-specific regulations, such as those in energy, transportation, and urban development, are well-positioned to gain market share.

Partnerships for innovation: Collaboration with technology providers and academic institutions will drive the development of cutting-edge climate solutions.

Emerging services: Expanding service portfolios to include climate resilience planning and decarbonization strategies will be critical to meeting evolving client needs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Size Estimates and Forecasts for the Study Period

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Focus on the Reduction of Carbon Footprint and Fulfilment of Net Zero Targets

- 5.1.2 National Goals Across the World to Combat Climate Change

- 5.1.3 Emerging Trends in Climate Change Consulting

- 5.2 Market Challenges

- 5.2.1 Lower Levels of Adoption with Large Gaps in the Realistic Scenario

- 5.2.2 Barriers to adoption lead to Challenge of the market

- 5.3 Key Trend Analysis within Various Services

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Energy and Power

- 6.1.2 Mining

- 6.1.3 Public Sector

- 6.1.4 Manufacturing

- 6.1.5 Other End-user Industries

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 Spain

- 6.2.2.4 Italy

- 6.2.2.5 France

- 6.2.2.6 Benelux

- 6.2.2.7 Poland

- 6.2.2.8 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 Australia

- 6.2.3.2 China

- 6.2.3.3 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Rest of Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Jacobs Solutions Inc.

- 7.1.2 AECOM

- 7.1.3 WSP Global Inc.

- 7.1.4 Stantec Inc.

- 7.1.5 Ramboll Group A/S

- 7.1.6 Tetra Tech Inc.

- 7.1.7 ERM International Group Limited

- 7.1.8 Ove Arup & Partners International Ltd

- 7.1.9 GHD Group Limited

- 7.1.10 Sweco AB

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET