PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683804

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683804

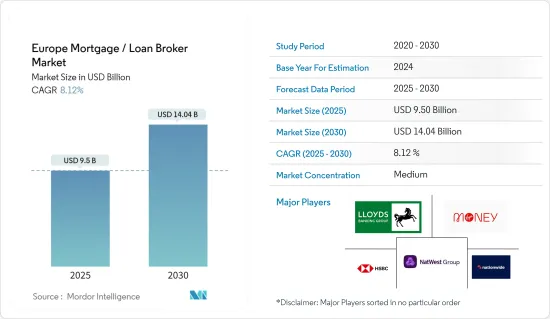

Europe Mortgage / Loan Broker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe Mortgage / Loan Broker Market size is estimated at USD 9.50 billion in 2025, and is expected to reach USD 14.04 billion by 2030, at a CAGR of 8.12% during the forecast period (2025-2030).

The European loan broker market has grown rapidly in recent years. This is due to several factors, including increased financial awareness, a variety of borrowing requirements, and a greater variety of loan products available. The growth of the European loan broker market can be attributed to several reasons, such as the need for specialist financial advice, outsourcing of loan search procedures, and the demand for attractive loan terms. Regulatory compliance, competition in the market, and the ever-changing digital environment are also factors that have contributed to the growth of the Europe loan broker market.

Loan brokers are diversifying their services to meet consumer needs, from personal loans to mortgages and auto loans to small business loans. The European loan brokers market is being affected by regulatory changes that seek to improve consumer safety, transparency, and fairness in lending. To maintain trust and trustworthiness, brokers must remain compliant with ever-changing regulations.

In fact, mortgage brokers in many of the world's largest markets are responsible for a surprising amount of home loan origination. For example, brokers in the Netherlands account for about 60% of all home loan originations, while brokers in Australia account for about 70%. In the UK, it's even higher at 75%. (Another type of intermediary, online aggregators, are also becoming increasingly important in the loan origination process by providing customers with transparency and competitive support.)

Europe Loan Broker Market Trends

The Housing Market's Expansion Drives Up Demand for Mortgage Brokers

The home loan segment is indeed a major market in the mortgage/loan broker market in Europe. The market for home loans in Europe is diverse, with various types of loans and lenders available across different countries. Factors such as interest rates, loan terms, and eligibility criteria can vary widely. Economic conditions, such as interest rates, employment levels, and housing market trends, significantly influence the residential mortgage market. Changes in these factors can impact borrower demand and lender profitability.

United Kingdom is Dominating the Market

In 2021, the mortgage lending market was booming in the United Kingdom. Gross lending increased 26% over 2020, when pandemic restrictions had a significant negative impact on lending, to GBP 308.5 billion. Yet it was also 15% more than the GBP 269.0 billion in 2019.

While slightly rising to 2.11% from 2.00% in 2020, the average mortgage interest rate stayed below the average of 2.25% in 2019. In response to the pandemic, the base rate was decreased in March 2020 from 0.75% to 0.10%. When more lenders priced in the extra risk or pulled these products off the market, mortgage interest rates first rose, especially at larger LTVs (over 75%).

Europe Loan Broker Industry Overview

The market is semi-consolidated, with some dominant players like Lloyds Banking Group. The main competitors in the European mortgage/loan broker business are covered in the research. Loan brokers face intense competition since they depend on their relationships with the best real estate agents and lenders in the communities they cover. Some major players in the market are Lloyds Banking Group, NatWest Group, Nationwide BS, HSBC Bank, and Virgin Money.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights of Technology Innovations in the Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Enterprise

- 5.1.1 Large

- 5.1.2 Small

- 5.1.3 Mid-sized

- 5.2 By Applications

- 5.2.1 Home Loans

- 5.2.2 Commercial and Industrial Loans

- 5.2.3 Vehicle Loans

- 5.2.4 Loans to Governments

- 5.2.5 Other Applications

- 5.3 By End- User

- 5.3.1 Businesses

- 5.3.2 Individuals

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Lloyds Banking Group

- 6.1.2 NatWest Group

- 6.1.3 Nationwide BS

- 6.1.4 HSBC Bank

- 6.1.5 Virgin Money

- 6.1.6 Santander UK

- 6.1.7 Barclays

- 6.1.8 Coventry BS

- 6.1.9 Yorkshire BS

- 6.1.10 TSB Bank*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 DISCLAIMER AND ABOUT US