Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683767

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683767

Europe Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 60 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

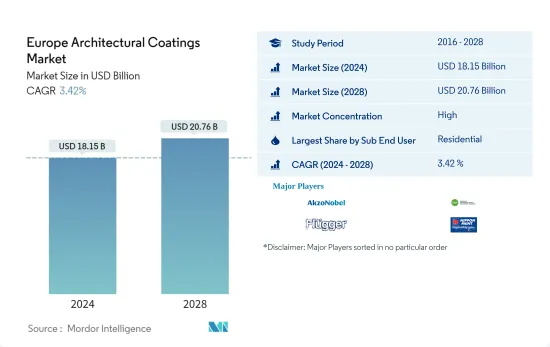

The Europe Architectural Coatings Market size is estimated at USD 18.15 billion in 2024, and is expected to reach USD 20.76 billion by 2028, growing at a CAGR of 3.42% during the forecast period (2024-2028).

Key Highlights

- Largest Segment by End-user - Residential : The share of residential coatings has been declining in Europe due to the relatively slow growth of residential constructions compared to commercial constructions.

- Fastest Segment by Technology - Solventborne : Waterborne coatings are the largest and fastest technology type due to consumer awareness and regulations, such as EU REACH, combined with various country-level regulations.

- Largest Segment by Resin - Acrylic : Acrylics are the most dominant resin type in Europe. They are expected to continue their dominance as acrylic latex emulsions are expected to replace solvent-borne coatings.

Europe Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

- Among the end-user segments, the residential segment dominated the construction sector in 2020, generating the highest demand for architectural coatings in the European market, with a share of 71.61%.

- The share of residential coatings has been declining over the past five years due to the relatively slow growth of residential construction compared to commercial. However, in 2020, the high growth of the residential DIY segment in many countries and the contraction of commercial paint consumption contributed to the sudden increase in the share of residential coatings in the European architectural coatings market.

- The growth of the commercial segment is expected to be slightly higher than its residential counterpart, which may result in a slight recovery of the commercial share during the forecast period.

Germany is the largest segment by Country.

- In Europe, Germany has the largest architectural coatings consumption, with more than 17% share, followed by Russia, France, Italy, and the United Kingdom. Spain, Poland, and Nordic regions were estimated to have had a share of around 5% each during 2020. The share of eastern block countries such as Poland and Russia is expected to increase due to the increasing median floor area and paint per capita.

- Poland is estimated to be the fastest-growing architectural market in Europe, with around 4% growth during the forecast period, followed by Russia, Spain, and France, with around 3% growth rates. Mature markets such as Germany and Italy are expected to have lower growth rates of less than and around 2% in volume.

- Many countries such as Poland, Italy, and Germany saw huge increases in residential consumption in 2020 due to huge growth in consumption in the residential DIY segment.

Europe Architectural Coatings Industry Overview

The Europe Architectural Coatings Market is moderately consolidated, with the top five companies occupying 41.46%. The major players in this market are AkzoNobel N.V., DAW SE, Flugger group A/S, Nippon Paint Holdings Co., Ltd. and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 93084

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Floor Area Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

- 4.1 Sub End User

- 4.1.1 Commercial

- 4.1.2 Residential

- 4.2 Technology

- 4.2.1 Solventborne

- 4.2.2 Waterborne

- 4.3 Resin

- 4.3.1 Acrylic

- 4.3.2 Alkyd

- 4.3.3 Epoxy

- 4.3.4 Polyester

- 4.3.5 Polyurethane

- 4.3.6 Other Resin Types

- 4.4 Country

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Italy

- 4.4.4 Nordic Countries

- 4.4.5 Poland

- 4.4.6 Russia

- 4.4.7 Spain

- 4.4.8 United Kingdom

- 4.4.9 Rest Of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles

- 5.4.1 AkzoNobel N.V.

- 5.4.2 Brillux GmbH & Co. KG

- 5.4.3 CIN, S.A.

- 5.4.4 DAW SE

- 5.4.5 Flugger group A/S

- 5.4.6 Hempel A/S

- 5.4.7 KOBER SRL

- 5.4.8 Nippon Paint Holdings Co., Ltd.

- 5.4.9 POLICOLOR SA

- 5.4.10 PPG Industries, Inc.

- 5.4.11 Sniezka SA

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.