PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852043

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852043

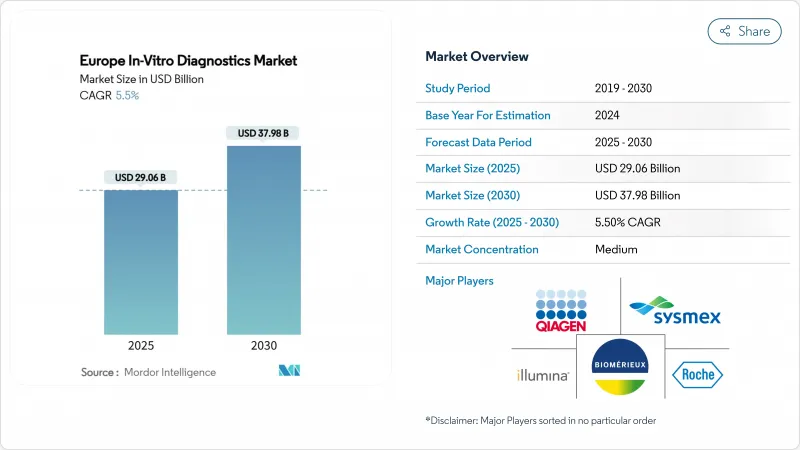

Europe In-Vitro Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe in vitro diagnostics market stands at USD 29.06 billion in 2025 and is forecast to reach USD 37.98 billion by 2030, reflecting a 5.5% CAGR over the period.

This trajectory highlights the region's rapid uptake of advanced testing platforms, the push for early chronic-disease detection and the regulatory lift provided by the EU IVDR. Germany's leading healthcare infrastructure, the United Kingdom's digital transformation agenda and the strong shift toward point-of-care models are giving suppliers clear expansion avenues. Molecular techniques are moving from specialised centres into mainstream care pathways, while immunodiagnostics remain a workhorse for routine analysis and screening. Consumables continue to anchor recurring revenue, and non-invasive specimen types are broadening patient access.

Europe In-Vitro Diagnostics Market Trends and Insights

Burden of Chronic & Infectious Diseases Elevates Demand for Early Diagnostics

Rising multimorbidity means almost 70% of inpatient treatment decisions already depend on accurate laboratory evidence. Oncology and cardiovascular pathways now integrate biomarker panels to stratify risk and guide therapies. Roughly 50 million Europeans are managing more than one chronic condition, intensifying calls for multiplex tests that handle several analytes from a single sample. Post-pandemic surveillance budgets remain higher than pre-2020 benchmarks, ensuring labs maintain expanded infectious-disease capacity. Health ministries view wider testing access as prerequisite for universal-coverage goals, pushing procurement of high-throughput platforms and near-patient devices at primary-care level.

Adoption of Point-of-Care Testing Across Primary Care Networks

Decentralised devices are cutting diagnostic turnaround in family-medicine settings. A United Kingdom cost-minimisation study showed GBP 29 savings per 100 patients screened when point-of-care analysers were used during NHS Health Checks. European paediatricians report large inter-country differences, yet urine dipstick availability in primary care now exceeds 80% in two-thirds of surveyed nations. Machine-learning firmware embedded in new devices is lifting sensitivity for low-abundance targets and enabling multi-marker cards that rival core-laboratory precision. These benefits are catalysing payer acceptance, especially for chronic-disease follow-up.

Lengthy Regulatory Timelines & Compliance Costs under EU IVDR

The Association for Molecular Pathology reports that 73% of European laboratories still lack full clarity on IVDR obligations, while notified-body queues extend up to two years for some categories. Start-ups face disproportionate legal and biostatistical-study expenses, delaying novel assays for emerging pathogens and rare diseases. Although the Commission granted phased deadlines, any lapse in certification can disrupt hospital supply chains.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Personalised Medicine Boosts Molecular & Companion Diagnostics

- Aging Population & Preventive Screening Programs Expand Test Volumes

- Reimbursement Uncertainty for Advanced Molecular Tests

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Europe in vitro diagnostics market size for immunodiagnostics was bolstered by a 27% revenue share in 2024, reflecting its role in hormone, infectious-disease and autoimmune panels. High-sensitivity chemiluminescent assays keep volumes robust, while COVID-19 investments have permanently upgraded instrument fleets. Molecular diagnostics is expected to generate the highest 7.2% CAGR through 2030, propelled by declining sequencing costs and companion-test uptake. Oncology now accounts for most European genomic testing, but rapid-cycling PCR platforms for respiratory pathogens, sexually transmitted infections and antimicrobial stewardship broaden the addressable base. AI-driven variant-calling software lifts analytical confidence and compresses reporting times.

Routine clinical chemistry remains foundational for electrolyte and metabolic screens, supported by continuous analyser automation. Hematology benefits from digital morphology and integrated coagulation modules that turn full blood counts into rich diagnostic outputs. Meanwhile, microbiology workflows integrate MALDI-TOF and syndromic panels, speeding pathogen ID and therapy guidance. As these test categories intertwine via middleware, clinicians obtain comprehensive views from fewer samples, meeting the drive for efficient patient-centred care across the Europe in vitro diagnostics market.

Reagents and consumables delivered 65% of 2024 revenue, underlining the razor-and-blade economics that stabilise cash flow and raise switching barriers. Bulk purchasing agreements in national tenders favour incumbents, yet quality-management clauses now weigh digital-traceability functions. Instruments are trending toward open-channel architectures that flex between chemistry and immunoassay modalities, helping labs maximise analyser uptime. Middleware dashboards curate quality-control flags and utilisation analytics, nudging procurement towards holistic platform deals rather than isolated analyser sales.

The software and services segment, while smaller, is forecast to post the fastest 8.5% expansion. Labs increasingly pay subscription fees for LIS integration, AI-assisted result interpretation and regulatory documentation modules. Vendors monetise cloud-based analytics that benchmark peer performance and automate external-quality assessments. This pivot elevates digital differentiation at a time when core analytic sensitivity gains are approaching technical ceilings, sustaining competitive edge in the Europe in vitro diagnostics industry.

Disposable devices held 58% revenue share in 2024 and are projected to clock a 6.9% CAGR. Single-use cartridges safeguard infection control in polyclinic settings and support home-testing convenience. Lateral-flow strips now cover C-reactive protein, cardiac troponin and vitamin-D assays, while microfluidic chips mount multiplex panels with minimal user steps. Environmental concerns spur suppliers to introduce biodegradable casings and take-back programs that reduce plastic waste.

Reusable devices dominate high-throughput central-lab workflows, where annual sample volumes justify capital investment. Upgrades focus on walk-away automation, self-cleaning modules and lower reagent dead-volume to curb consumable spend. Hybrid architectures pair reusable optical readers with disposable fluidics, balancing sustainability and performance across Europe in vitro diagnostics market applications.

The Europe In-Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, and More), Product & Service (Instrument, and More), Usability (Disposable IVD Devices, and More), Specimen Type (Blood, and More), Site of Testing (Central Laboratories and More), Application (Infectious Diseases and More), End User (Diagnostic Laboratories and More) and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Roche

- Abbott Laboratories

- Siemens Healthineers

- Danaher Corp. (Beckman Coulter & Cepheid)

- Thermo Fisher Scientific

- bioMerieux

- Beckton Dickinson

- Bio-Rad Laboratories

- QIAGEN

- Sysmex Corp.

- Hologic

- DiaSorin

- Illumina

- QuidelOrtho Corp.

- Mindray Bio-Medical

- Agilent Technologies

- Randox Laboratories

- Grifols

- Werfen

- Gentian Diagnostics ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Burden of Chronic & Infectious Diseases Elevates Demand for Early Diagnostics

- 4.2.2 Adoption of Point-of-Care Testing Across Primary Care Networks

- 4.2.3 Shift to Personalized Medicine Boosts Molecular & Companion Diagnostics

- 4.2.4 Aging Population & Preventive Screening Programs Expand Test Volumes

- 4.2.5 EU IVDR Raising Quality Standards and Stimulating High-Value Innovation

- 4.3 Market Restraints

- 4.3.1 Lengthy Regulatory Timelines & Compliance Costs under EUIVDR

- 4.3.2 Reimbursement Uncertainty for Advanced Molecular Tests

- 4.3.3 Laboratory Workforce Shortage and Capacity Constraints

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Molecular Diagnostics

- 5.1.3 Immunodiagnostics

- 5.1.4 Hematology

- 5.1.5 Microbiology & Lateral Flow

- 5.1.6 Other Tests

- 5.2 By Product & Service

- 5.2.1 Reagents & Consumables

- 5.2.2 Instruments/Analyzers

- 5.2.3 Software & Services

- 5.3 By Usability

- 5.3.1 Disposable IVD Devices

- 5.3.2 Reusable IVD Devices

- 5.4 By Specimen Type

- 5.4.1 Blood/Serum

- 5.4.2 Urine

- 5.4.3 Saliva

- 5.4.4 Tissue/Biopsy

- 5.5 By Site of Testing

- 5.5.1 Central Laboratories

- 5.5.2 Point-of-Care Testing

- 5.5.3 Home/Self-Testing

- 5.5.4 Reference Labs

- 5.6 By Application

- 5.6.1 Infectious Diseases

- 5.6.2 Diabetes

- 5.6.3 Cancer/Oncology

- 5.6.4 Cardiology

- 5.6.5 Autoimmune Disorders

- 5.6.6 Nephrology & Renal Panels

- 5.6.7 Prenatal/Genetic Screening

- 5.7 By End User

- 5.7.1 Diagnostic Laboratories

- 5.7.2 Hospitals & Clinics

- 5.7.3 Academic & Research Institutes

- 5.7.4 Home-Care/POC Centers

- 5.8 By Country

- 5.8.1 Germany

- 5.8.2 United Kingdom

- 5.8.3 France

- 5.8.4 Italy

- 5.8.5 Spain

- 5.8.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 F. Hoffmann-La Roche AG

- 6.3.2 Abbott Laboratories

- 6.3.3 Siemens Healthineers AG

- 6.3.4 Danaher Corp. (Beckman Coulter & Cepheid)

- 6.3.5 Thermo Fisher Scientific Inc.

- 6.3.6 bioMerieux SA

- 6.3.7 Becton, Dickinson & Co.

- 6.3.8 Bio-Rad Laboratories Inc.

- 6.3.9 QIAGEN N.V.

- 6.3.10 Sysmex Corp.

- 6.3.11 Hologic Inc.

- 6.3.12 DiaSorin SpA

- 6.3.13 Illumina Inc.

- 6.3.14 QuidelOrtho Corp.

- 6.3.15 Mindray Bio-Medical

- 6.3.16 Agilent Technologies Inc.

- 6.3.17 Randox Laboratories Ltd.

- 6.3.18 Grifols S.A.

- 6.3.19 Werfen

- 6.3.20 Gentian Diagnostics ASA

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment