PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683127

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683127

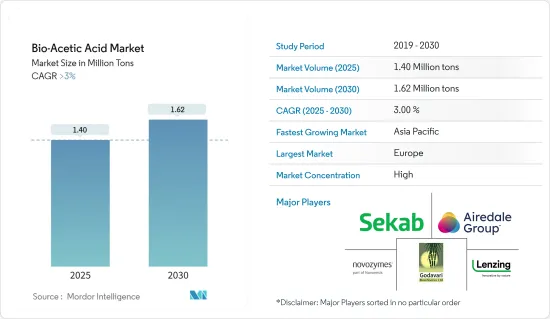

Bio-Acetic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Bio-Acetic Acid Market size is estimated at 1.40 million tons in 2025, and is expected to reach 1.62 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The bio-acetic acid market was negatively impacted by COVID-19 in 2020. Construction activities and automotive manufacturing activities were on a temporary halt owing to the pandemic scenario, which had minimized the demand for vinyl acetate monomer used in the formulation of these end-user industry products such as adhesives, paints, coatings, plastics, and composites, in turn, negatively impacted the market demand for bio-acetic acid. However, the market retained its growth trajectory due to all the industries' resumed production processes.

Increasing demand for bio-based and renewable chemicals and vinyl acetate monomers (VAM) is expected to drive market demand during the forecast period.

On the flip side, the availability of alternatives and volatility in the feedstock availability and prices are expected to hinder the growth of the market.

Developing new separation technologies to increase production efficiency is likely to act as an opportunity for the market studied over the forecast period.

Asia-Pacific accounts for the highest market share and is expected to dominate the market during the forecast period.

Bio-Acetic Acid Market Trends

The Vinyl Acetate Monomer (VAM) Segment to Dominate the Market

- Acetic acid is mainly used to manufacture vinyl acetate monomer (VAM). The major esters of acetic acid, such as ethyl acetate and butyl acetate, are commonly used as solvents for paints and coatings.

- Vinyl acetate monomer (VAM) is used to produce water-based paints, adhesives, waterproofing coatings, and paper and paperboard coatings that can be used in various end-use industries such as construction, paints and coatings, plastic, solvents, adhesives, and textiles.

- On the Global front, growth in vinyl acetate monomer consumption is driven by demand in China and the United States.

- In India, in 2023, Asian Paints (Polymers) Private Limited (APPPL), a wholly-owned subsidiary of Asian Paints Ltd, announced the setting up of a manufacturing facility of vinyl acetate-ethylene emulsion (VAE) and vinyl acetate monomer (VAM) at Dahej, Gujarat. The approximate cost of setting up the manufacturing facility would be INR 2,100 crore (USD 251.24 million).

- According to the Motilal Oswal Financial Services (MOFSL), vinyl acetate monomer (VAM) is the largest acetic acid derivative, accounting for 40% of its global demand.

- In October 2023, US-based multinational contractor KBR and its Japanese acetyls technology partner, Showa Denko, were selected by Asian Paints to provide services for a grassroots vinyl acetate monomer (VAM) plant in India. Under the contract terms, KBR will provide a technology license, basic engineering, and proprietary equipment for a 100,000 t/y plant. In contrast, Showa Denko will provide the catalysts, along with its technical operating know-how.

- Thus, all such trends in the VAM market are expected to drive the demand for the bio-acetic acid market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is the largest consumer of bio-acetic acid globally and is the fastest-growing market.

- Acetic acid is an important chemical reagent and industrial chemical used in producing plastic soft drink bottles, photographic films, paints, and coatings. The increasing construction activities boost the demand for paints and coatings to be used, boosting the demand for acetic acid.

- Asia-Pacific accounts for the growing demand for vinyl acetate monomer (VAM), a crucial role that China is playing. Due to the huge population in China and India, they pose a huge consumption potential for the global market.

- In India, 100% of domestic VAM demand is met through imports. The largest derivative, vinyl acetate monomer (VAM), accounts for 34% of acetic acid consumption. Singapore is a major importer, with more than half the share of the total quantity of VAM imported by India.

- In December 2023, Jiangsu Sopo Chemical in China announced investing in a vinyl acetate and EVA-integrated project in the Zhenjiang New District. This ambitious project will unfold in two stages, beginning with the construction of a VAM production plant with a substantial capacity of 330 thousand tons per year.

- In early 2023, INEOS and LOTTE Corporation announced plans to expand VAM production capacity from 450 kilotons to 700 kilotons by adding a third VAM plant in Ulsan, South Korea, with expectations for completion by the end of 2025.

- The factors above contribute to the increasing demand for bio-acetic acid consumption in Asia-Pacific.

Bio-Acetic Acid Industry Overview

The bio-acetic acid market is consolidated. Some major players (not in any particular order) include LENZING AG, Godavari Biorefineries Ltd, Airedale Group, Novozymes A/S (Novonesis Group), and Sekab.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Bio-based and Renewable Chemicals

- 4.1.2 Increasing Demand for Vinyl Acetate Monomers (VAM)

- 4.2 Restraints

- 4.2.1 Availability of Alternatives

- 4.2.2 Volatility in the Feedstock Availability and Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Raw Material

- 5.1.1 Biomass

- 5.1.2 Corn

- 5.1.3 Maize

- 5.1.4 Sugar

- 5.1.5 Other Raw Materials

- 5.2 Application

- 5.2.1 Vinyl Acetate Monomer (VAM)

- 5.2.2 Acetate Esters

- 5.2.3 Purified Terephthalic Acid (PTA)

- 5.2.4 Acetic Anhydride

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Qatar

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.6 Middle East and Africa

- 5.3.6.1 Saudi Arabia

- 5.3.6.2 South Africa

- 5.3.6.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AFYREN SA

- 6.4.2 Airedale Group

- 6.4.3 btgbioliquids

- 6.4.4 GODAVARI BIOREFINERIES LTD

- 6.4.5 Jubilant Ingrevia Limited

- 6.4.6 LanzaTech

- 6.4.7 LENZING AG

- 6.4.8 Novozymes A/S (Novonesis Group)

- 6.4.9 Sekab

- 6.4.10 SUCROAL SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of New Separation Technologies to Increase Production Efficiency