PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644496

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644496

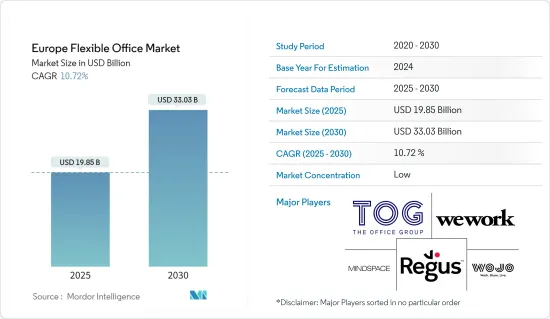

Europe Flexible Office - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe Flexible Office Market size is estimated at USD 19.85 billion in 2025, and is expected to reach USD 33.03 billion by 2030, at a CAGR of 10.72% during the forecast period (2025-2030).

Key Highlights

- In Q1 2023, flex office take-up in Europe constituted 4% of the total office take-up, marking a decline from its peak of 8% in 2019 and the 7% recorded in Q1 2022. Leading the pack, London City accounted for 13% of the take-up, with Prague at 8% and Amsterdam at 6%. A similar pattern emerged in major US cities, with flex office take-up dwindling from 7% in 2019 to 1.5% in 2023. This trend aligns with a global shift, where smaller operators enter the market and expand their footprint beyond major cities.

- The increase in small and medium-sized businesses is a trend observed across all major cities of Europe, while new working practices are neither location nor sector-specific. These trends have fueled the flexible office market in Europe. The number of startups in the region is expected to boost the market's growth.

- The growing significance of digital systems and the need for completing knowledge-intensive tasks has transformed into a surging desire among employees to work from the office or from any desired location in an independent way.

- This has offered firms in Europe a chance to utilize the office space more proficiently, reduce the traveling hours of employees, and increase employee satisfaction, thereby boosting their work efficiency and productivity. This will help the flexible office market grow during the forecast period.

- Although the demand for flexible office space continues to grow, some obstacles stand in the way of the adoption of this model. Commonly raised concerns include the issues of information security, confidentiality, and privacy in a more open environment. This leads to the companies worrying about the potential impact on their marketing, especially because it could weaken their brands. However, such concerns are outweighed by the risk that companies may need more flexible space in their portfolios. This is due to the developments in the labor market, with many employers worrying about either keeping or attracting the most highly skilled workers.

Europe Flexible Office Market Trends

Increasing Demand for Coworking Spaces

Occupiers are increasingly showing interest in both flexible office spaces and those fitted by landlords. This trend responds to the escalating costs of fit-outs and financing and delays in development completions. Opting for these spaces helps mitigate these risks and offers occupiers enhanced flexibility and convenience. Also, the scarcity of prime flexible office spaces in key locations further fuels the demand for landlord-fitted spaces, with some centers reporting full occupancy rates.

Traditionally, smaller tenants have preferred fitted office spaces, with most deals for spaces under 5,000 sq. ft. However, there has been a noticeable increase in the number of fitted office space deals, ranging from 5,000 to 10,000 sq. ft. This trend is particularly pronounced in the City of London market.

In 2022, the City of London doubled transaction volumes for landlord-fitted spaces below 10,000 sq. ft. Landlord-fitted spaces constituted 42% of all office leasing transactions below 10,000 sq. ft in the City of London in 2022, a significant jump from the 21% seen in 2021.

Additionally, there is a rising demand for fully managed spaces where landlords offer soft services. It is anticipated that smaller tenants will continue to prefer fitted spaces, particularly as 'package deals' that include soft services gain traction.

The United Kingdom Dominates the Market

Management agreements are gaining popularity in the United Kingdom, and they accounted for 43% of deals by H1 2023, a significant jump from just 9% in 2019. Currently, 14 serviced office operators in the United Kingdom are actively searching for spaces exceeding 20,000 sq. ft, and an overwhelming 93% prefer the management agreement model.

London's office space market is rapidly expanding, fueled by its thriving start-ups and IT sectors, surging office lease demands, and the emergence of flexible workspaces.

This surge in small and medium-sized businesses is a nationwide trend, while new work practices transcend location and sector boundaries.

These dynamics drive the flexible office market in London, as the region's burgeoning start-up scene is set to fuel its expansion further.

Several key factors are shaping London's office market. These include notable trends such as a surge in completions, shorter lease terms, robust growth in the flexible workspace segment, and an oversupply of prime office spaces due to a persistent preference for quality.

Recent studies from 2023 have highlighted an increasing demand for flexible office spaces in London. As businesses increasingly call for a return to the office, flexible work arrangements benefit both in-person and remote scheduling.

This heightened demand leads to a dwindling supply of flexible offices and a subsequent rise in costs. For instance, in 2022, the rental cost for a permanent desk in a flexible workspace saw a 3.4% quarterly increase, reaching GBP 690 per month (USD 867.19 per month).

Europe Flexible Office Industry Overview

The European flexible office market is fragmented, with many players existing in the flexible office spaces market. Also, many more companies are entering the market to meet the increasing demand for casual office environments. The European flexible office market companies are involved in several growth and expansion strategies to gain a competitive advantage. The major players include The Office Group, WeWork, WOJO, Regus Group, and Mindspace.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Insights into Office Rents

- 4.6 Insights into Office Space Planning

- 4.7 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Booming remote work driving the market

- 5.1.2 Increasing number of start-ups and small businesses

- 5.2 Restraints

- 5.2.1 Growing number of providers offering similar services affecting the market

- 5.2.2 Economic uncertainities and regulatory factors affecting the market

- 5.3 Opportunities

- 5.3.1 The potential to expand into untapped markets

- 5.3.2 The evolving needs of remote workers and freeelancers are also driving the market

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers/Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Private Offices

- 6.1.2 Coworking Spaces

- 6.1.3 Virtual Offices

- 6.2 By End User

- 6.2.1 IT and Telecommunications

- 6.2.2 Media and Entertainment

- 6.2.3 Retail and Consumer Goods

- 6.3 By Geography

- 6.3.1 Germany

- 6.3.2 United Kingdom

- 6.3.3 France

- 6.3.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 The Office Group

- 7.2.2 WeWork

- 7.2.3 WOJO

- 7.2.4 Regus Group

- 7.2.5 Mindspace

- 7.2.6 KNOTEL

- 7.2.7 Ordnung ApS

- 7.2.8 Matrikel1

- 7.2.9 Green desk

- 7.2.10 DBH Business Services*

- 7.3 Other companies

8 FUTURE OF THE MARKET

9 APPENDIX

10 DISCLAIMER