PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644462

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644462

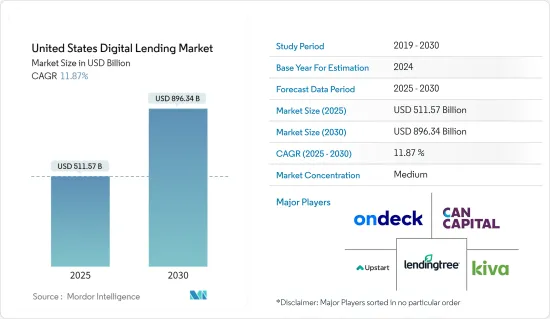

United States Digital Lending - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States Digital Lending Market size is estimated at USD 511.57 billion in 2025, and is expected to reach USD 896.34 billion by 2030, at a CAGR of 11.87% during the forecast period (2025-2030).

Market expansion is anticipated to be fueled by the advantages provided by digital lending platforms, such as improved loan optimization loan process, quicker decision-making, compliance with regulations and norms, and improved corporate efficiency. Traditional lending platforms required physical contact and human engagement at every stage, which prolonged processing times and raised the possibility of human error. However, digital lending platforms allow banks to automate the loan process, improving consumer satisfaction.

Key Highlights

- The United States is one of the largest and most advanced markets for digital lending globally due to its early adoption of digitization in various sectors. Also, factors such as the strong economy and robust presence of prominent solution providers, coupled with strong investment by government and private organizations for the development and growth of research & development activities, are poised to drive the demand for digital lending in the region.

- Funding is a crucial element of the digital lending business model. There are three major funding models used by digital lenders: Marketplace lenders, Balance sheet lenders, and bank channel lenders. Several digital lenders have been tapping multiple funding models as they grow.

- Further, banking institutions retain certain fundamental competitive advantages. Arguably the most important is their access to insured deposits, which affords them low-cost capital. Regulatory concerns have likely caused banks to hesitate when adopting new technologies, but banks are increasingly looking for points of entry to the fintech space. It is expected that many banks will partner with existing fintech companies to have their cost advantages with the fintech's technological capabilities.

- By combining their technological expertise with banks' lower cost of capital, these partnerships could enable banks to provide more efficient customer experiences at lower rates and open them up to previously untapped customer segments. Also, in the United States, platforms engaging in credit origination can be subjected to licensing requirements in each state. For this reason, many platforms partner with the banks to originate loans agreed online.

- Owing to the COVID-19 pandemic, SMEs in the region faced challenges in raising funds during the crisis to keep their businesses operating. Digital Lending is expected to find several opportunities, especially among SMEs, for growth and adoption. Further, during the COVID-19 pandemic, the government aimed to support the people. Moreover, given widespread job losses, wage reductions, and a severe liquidity shortage, banks and financial institutions (FIs) anticipates to experience an increase in credit costs and non-performing assets ratio as the effects of COVID-19 on the lending industry develop. Lenders can benefit significantly from the use of technology to assist them in adjusting to the new normal.

United States Digital Lending Market Trends

Increasing Number of Potential Loan Purchasers with Digital Behavior

- According to the U.S. Small Business Administration, there are USD 410 billion in sub-USD 1 million loans to small firms and USD 4 trillion in outstanding consumer loans for small enterprises in the US. In addition, the US Federal Reserve Bank of NY calculates an approximate USD 100 billion unmet credit demand due to banks' resistance to making small-dollar loans. To address the unmet demand, technology-driven digital lenders are attracting attention in their capacity to collaborate with banks.

- Moreover, credit platforms majorly encourage investors to spread the risks. Investors can choose to spread the investments across various multiple loans and often can automatically gain exposure to a portfolio of loans based on the risk category and terms they select. Among P2P (peer-to-peer) consumer platforms, more than 95% of the United States use an auto-selection process. In facilitating credit, fintech platforms can provide monitoring and servicing functions that are similar to those of traditional credit providers such as banks.

- Most consumers use fintech providers to refinish or consolidate existing debts, but some use them to finance their major purchases (such as vehicles or real estate). Borrowing by students to fund higher education is prominent in the United States.

- On the business side, various small and micro enterprises typically seek funds for working capital or investment projects. Financing can also be in the form of invoice trading, whereby investors purchase discounted claims on a firm's invoices (receivables). SMEs are contributing to the economy significantly for most regions. The following statistics validate the above statement: According to the US Small Business Administration (SBA), more than 50% of Americans either own or work for a small business.

Consumer Digital Lending is Expected to Grow Significantly

- Bank channel-based lending drew particular attention, especially with the IPO of consumer loan-focused GreenSky Inc. The company has secured more than USD 11 billion in bank commitments. Small business-focused lender OnDeck announced an expansion of its OnDeck-as-a-Service platform through which it licenses its technology to banks. The company added PNC Bank as a customer and launched a new subsidiary, ODX, to handle future bank channel-based business. Avant launched a bank partnership platform for personal lending called Amount.

- In order to keep growing, digital lenders are taking advantage of opportunities to expand the scope of their activities, both in terms of funding and product offerings. For example, SoFi, which began as a student loan refinancing company, now offers personal loans and mortgages. Personal loan-focused LendingClub also offers a business loan product. While some the companies, such as Square and PayPal, entered digital lending from adjacent fintech segments, some lenders are moving in the other direction by offering nonlending services. SoFi has been the most aggressive on this front, offering wealth management services and accepting applicants for its high-yield deposit account product, SoFi Money.

- Student-focused lenders remain the most diversified platforms in the digital lending sector as Student loan startups are witnessing new investments and new customers as the region faces a continued student loan debt crisis. The Federal Reserve estimates USD 1.7 trillion in U.S. student loan debt. Students, on average, graduate with USD 29,000 of private and federal loan debt and default on their loans at a rate of 15%.

- Product offerings in this segment include student loan refinance, direct student loans, personal loans, and even wealth management and mortgage products.

- Due to its capacity to assist financial institutions with service delivery, document management, information storage, and data processing online, the cloud can be regarded as one of the most important trends in digital lending. It's understandable why, according to Accenture, more than 90% of banks currently have at least a significant level of workloads operating in the cloud.

United States Digital Lending Industry Overview

The United States digital lending market is expected to be semi-consolidated, observing an increase in the number of investments and M&A activities by various global enterprises to gain access to the market. Vendors are increasingly spending on gaining a consumer base by offering numerous benefits. In addition, such investments are a strong part of their competitive strategy. Access to the distribution channel, already present business relations, better supply chain knowledge, and the self-owned platform give the established tech giants entering the market an advantage over the new competitors.

In October 2023, Blend Labs, a United States-based software company, and MeridianLink Inc., a software provider for financial institutions and consumer reporting agencies, announced a partnership. Blend stated that lenders utilizing MeridianLink Consumer loan origination software (LOS) can use Blend's unified platform and consumer banking origination software for a quick onboarding and application procedure for banking, credit card, and loan products.

In September 2023, the digital lending platform Revvin, formerly MortgageHippo, was announced to be acquired by Maxwell, a mortgage fintech sponsored by Wells Fargo, to improve its point-of-sale technology. The company focuses on Revvin's faster loan origination process, which Maxwell thinks would benefit lenders as the mortgage market continues to be challenged by rising interest rates, limited loan volume, and increasing lending expenses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Regulatory Landscape

- 4.3 Key Indicators for Personal Loan Borrowers in the United States

- 4.3.1 Percentage of Loan Debt in United States Held By Borrowers

- 4.3.1.1 Super Prime

- 4.3.1.2 Prime Plus

- 4.3.1.3 Prime

- 4.3.1.4 Near Prime

- 4.3.1.5 Sub Prime

- 4.3.2 Average Outstanding Balances in United States Held By Borrowers

- 4.3.2.1 Super Prime

- 4.3.2.2 Prime Plus

- 4.3.2.3 Prime

- 4.3.2.4 Near Prime

- 4.3.2.5 Sub Prime

- 4.3.3 Delinquency Rates of Borrowers in United States

- 4.3.3.1 Super Prime

- 4.3.3.2 Prime Plus

- 4.3.3.3 Prime

- 4.3.3.4 Near Prime

- 4.3.3.5 Sub Prime

- 4.3.1 Percentage of Loan Debt in United States Held By Borrowers

- 4.4 Analysis of Origination Volumes of Digital Lenders

- 4.4.1 Personal Loans

- 4.4.2 SME Loans

- 4.5 Analysis of Subprime Borrowers in the United States

- 4.5.1 Distribution by States

- 4.5.2 Demographic Breakdown by Age

- 4.5.3 Overall Shrinking of Subprime Population in the Country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Uptick of Potential Loan Purchasers with 'Digital Behavior'

- 5.1.2 Increasing Disposable Income

- 5.2 Market Restraints

- 5.2.1 Security Concerns involved in Digital Lending

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Business

- 6.1.1.1 Business Digital Lending Market Dynamics

- 6.1.1.2 Business Digital Lending Ecosystem (including both Startups and Incumbents)

- 6.1.1.3 Market Size Estimates and Forecasts

- 6.1.2 Consumer

- 6.1.2.1 Consumer Digital Lending Market Dynamics

- 6.1.2.2 Consumer Digital Lending Models (Payday Lenders, Peer-to-peer Loans, Personal Loans, Auto Loans, and Student Loans)

- 6.1.2.3 Consumer Digital Lending Ecosystem (including both Startups and Incumbents)

- 6.1.2.4 Market Size Estimates and Forecasts

- 6.1.1 Business

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bizfi, LLC.

- 7.1.2 OnDeck Capital Inc.

- 7.1.3 Prosper Marketplace Inc.

- 7.1.4 LendingClub Corp.

- 7.1.5 Social Finance Inc. (SoFi)

- 7.1.6 Upstart Network Inc.

- 7.1.7 Kiva Microfunds

- 7.1.8 Kabbage Inc.

- 7.1.9 Lendingtree Inc.

- 7.1.10 CAN Capital Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE OUTLOOK