PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644450

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644450

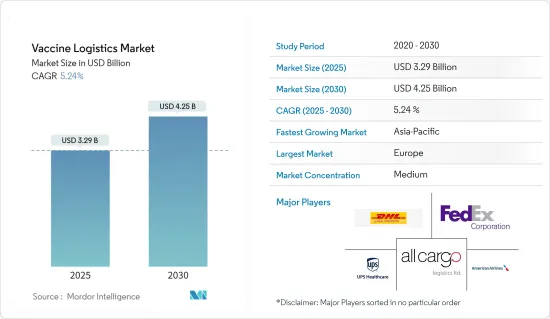

Vaccine Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Vaccine Logistics Market size is estimated at USD 3.29 billion in 2025, and is expected to reach USD 4.25 billion by 2030, at a CAGR of 5.24% during the forecast period (2025-2030).

New vaccines, evolving immunization schedules, innovative service delivery strategies, a broader target population, heightened cold-chain infrastructure demands, and limited funding are reshaping the dynamics of the vaccine transportation market.

Climate change has significantly altered the landscape of infectious diseases. Rising temperatures are broadening the habitats of disease vectors like mosquitoes and ticks, facilitating the spread of diseases such as malaria, dengue fever, and Lyme disease. This pattern, alongside extreme weather events and ecosystem disruptions, heightens the risk of zoonotic diseases, waterborne illnesses, and respiratory infections, underscoring the growing demand for vaccines.

For example, the Pfizer-BioNTech Vaccine mandates storage in specialized temperature-controlled thermal shippers, requiring ultra-low temperatures between -112°F and -76°F (-80°C to -60°C). Similarly, while the Moderna Vaccine doesn't demand the extreme temperatures of its Pfizer counterpart, it still requires storage at -4°F (-20°C). This vaccine must be transported directly from the manufacturing facility to its point of use, avoiding any prolonged exposure to elevated temperatures.

Transporting temperature-sensitive vaccines stands out as a particularly challenging endeavor among pharmaceuticals. These vital products necessitate meticulous handling throughout the supply chain, relying on precisely coordinated temperature-controlled logistics. Maintaining a consistent temperature is crucial, vaccines must remain within a specified range from production to administration. Deviating from this range jeopardizes the vaccine's potency and its protective efficacy against targeted diseases.

Moreover, the vaccine transportation market faces numerous challenges due to evolving vaccine requirements, climate change impacts, and stringent temperature control needs. Addressing these challenges is crucial to ensuring the efficacy and safety of vaccines worldwide.

Vaccine Logistics Market Trends

Growth and Transformation in the North American Vaccine Logistics Market

The North American vaccine logistics market is witnessing growth, primarily fueled by the surging demand for temperature-controlled transportation and storage solutions. Logistic providers are bolstering their cold chain capabilities to ensure vaccines retain their efficacy during transit. For example, FedEx has broadened its network of temperature-controlled facilities throughout the U.S., facilitating the efficient handling of vaccines that adhere to stringent temperature regulations. This strategic move not only addresses logistical challenges but also significantly enhances its cold chain capabilities, with key facilities in cities like Philadelphia and Dallas.

Furthermore, the rollout of new vaccines and the shifting immunization schedule are transforming North America's logistics landscape. In 2024, XPO has rolled out its thermally mapped transportation fleet to oversee the distribution of heat-sensitive vaccines nationwide. The company has successfully orchestrated deliveries in major cities like Chicago and Houston, guaranteeing that vaccines stay within the mandated temperature ranges from their origin to healthcare providers.

In conclusion, the North American vaccine logistics market is evolving rapidly, driven by advancements in cold chain technology and the introduction of new vaccines. Companies are also ensuring efficient and reliable vaccine distribution across the region.

Cold Chain Innovations in Vaccine Logistics Services

First, the demand for cold chain solutions is on the rise. Over the past decade from 2024, investments in the cold chain logistics sector have surged. As reported by the Biopharma Cold Chain Sourcebook, in 2020, temperature-controlled logistics made up nearly 18% of biopharma logistics expenditures. This upward trend shows no signs of slowing down.

For instance, many vaccines, such as those for diphtheria, tetanus, pertussis (DTP), and measles, mumps, and rubella (MMR), lack thermal stability. These heat-sensitive vaccines, if not kept between 2°C and 8°C, degrade quickly due to their biological components. Consequently, they depend heavily on a multi-stage refrigerated or cold-chain distribution system.

Moreover, with the advent of advanced technologies like artificial intelligence (AI) and blockchain, the pharmaceutical sector is witnessing a crucial trend: enhanced supply chain visibility. The tracking, monitoring, and management of temperature-sensitive products now generate more data than ever. Technologies that bolster this visibility not only mitigate spoilage risks but also ensure adherence to regulatory standards.

In addition, companies are innovating high-tech containers equipped with closed temperature-controlled systems. These containers facilitate the seamless transport of temperature-sensitive goods between cargo warehouses and aircraft, specifically catering to the pharmaceutical sector.

For instance, at the Port of Tyne in the UK, 5G-enabled autonomous drones have been deployed. These drones boost operational efficiency and oversee cargo handling, bolstering the cold chain by expediting processes and reducing delays for temperature-sensitive supplies.

In conclusion, the increasing demand for cold chain solutions, coupled with technological advancements, is transforming the vaccine logistics landscape. Enhanced supply chain visibility and innovative temperature-controlled systems are critical in ensuring the safe and efficient distribution of vaccines.

Vaccine Logistics Industry Overview

The vaccine logistics market is fragmented and is dominated by international companies, such as DHL Global Forwarding, AllCargo Logistics, American Airlines, FedEx Corporation and UPS Healthcare . These giants are pursuing expansion strategies, primarily through acquisitions. Their established presence allows for smoother market expansion compared to smaller players.

The demand for refrigerated warehouses, expedited delivery services, and bulk vaccine transportation is on the rise. This surge is further bolstered by heightened government investments, offering market players a chance to broaden their reach and enhance efficiency over time.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Technology innovation in temperature controlled packaging

- 4.2.1.2 Cross Border collaborations and initiative to enhance healthcare infrastructure

- 4.2.2 Restraints

- 4.2.2.1 Supply chain distruption and transportation bottlenecks can hinder timely vaccine distribution

- 4.2.2.2 Regulatory and Compiliance Challenges

- 4.2.3 Opportunities

- 4.2.3.1 Adoption of blockchain and IoT technology can improve transparency and tracebility

- 4.2.3.2 Next-Generation Vaccines

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers/Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technological Trends and Automation

- 4.5 Government Regulations and Initiatives

- 4.6 Industry Value Chain/Supply Chain Analysis

- 4.7 Spotlight on Ambient/Temperature-controlled Storage

- 4.8 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Land (Road and Rail)

- 5.1.1.2 Air

- 5.1.1.3 Sea

- 5.1.2 Warehousing

- 5.1.3 Value-added Services (Packaging, Labeling, etc.)

- 5.1.1 Transportation

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Drug Manufacturers and Distributors

- 5.2.3 Other End Users (Blood Banks, Clinics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 Australia

- 5.3.1.4 India

- 5.3.1.5 Singapore

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Thailand

- 5.3.1.9 South Korea

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 North America

- 5.3.3.1 United States

- 5.3.3.2 Canada

- 5.3.3.3 Mexico

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Colombia

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Egypt

- 5.3.5.2 Qatar

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Rest of the Middle East

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 DHL Global Forwarding

- 6.2.2 AllCargo Logistics

- 6.2.3 American Airlines

- 6.2.4 DB Schenker

- 6.2.5 FedEx Corporation

- 6.2.6 Kuehne Nagel

- 6.2.7 Nippon Express

- 6.2.8 Yamato Logistics

- 6.2.9 Americold Logistics

- 6.2.10 lynden international logistics

- 6.2.11 DP World

- 6.2.12 Coldman Logistics

- 6.2.13 Cavalier Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin