PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644310

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644310

Digital Lending - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

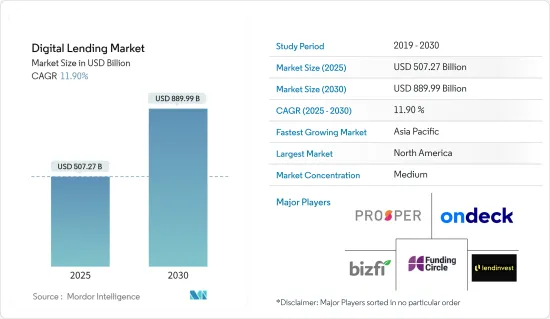

The Digital Lending Market size is estimated at USD 507.27 billion in 2025, and is expected to reach USD 889.99 billion by 2030, at a CAGR of 11.9% during the forecast period (2025-2030).

Key Highlights

- Digital lending, also known as fintech lending, involves securing loans through online platforms, making the borrowing process more efficient. Rather than physically visiting a bank, borrowers can apply for loans online. This digital approach removes the need for traditional intermediaries, such as banks, and significantly reduces the burden of paperwork.

- The lending landscape has changed drastically over the years due to the rapid adoption of digitization in the BFSI industry. While the traditional form of lending still prevails in many parts of the world, the benefits provided by digital solution providers are increasingly paving the way for the adoption of digital lending solutions and services across enterprises.

- Another major factor driving the market's growth is the changing consumer expectations and behavior due to the several benefits of digitizing banking and financial services. Customers may hail from diversified backgrounds and require loans for various purposes, ranging from personal loans to SME finance and home loans.

- Furthermore, technological advancements, such as the proliferation of smartphones, have led to an increase in the adoption of digital banking across several end-user verticals. Also, technologies like artificial intelligence, machine learning, and cloud computing benefit banks and fintech as they can process vast amounts of customer information. This data and information are then compared to obtain results about timely services/solutions that customers want, which has aided in developing customer relations.

- Aire, Kabbage, and Kasisto are some of the most prominent financial industry startups that are fully investing in AI. For instance, Kabbage uses AI algorithms that assess all risks of lending money to a particular customer, allowing company managers to give loans in minimal time. The demand for personalization of their needs among consumers in fintech and banking companies has further strengthened the demand for AI.

Digital Lending Market Trends

The Consumer Segment to Witness Significant Growth

- According to the latest Expectations & Experiences consumer trends survey from Fiserv Inc., a leading global provider of financial services technology solutions, almost two-thirds of people who have applied for loans in the past two years do so either partially or fully online, representing a significant increase from the previous year. A central portion of this growth is due to the increasing usage of smartphones and tablets.

- Digital lending startups have also started giving out loans for education and professional courses, expanding from mainly focusing on personal loans to consumer lending space. For instance, Bengaluru-based Zest Money is betting big on lending for professional education purposes. The company partnered with players like Upgrade, NMIMS, Great Learning, Acadgild, and Edureka to provide funds to entry-level- or mid-level executives wanting to acquire new skill sets.

- Millennials with a few years of work experience and no credit history (or the new-to-credit segment) find their loans either unapproved or at high interest rates. Moreover, in traditional banks, the time to decide for small businesses and corporate lending averages between three and five weeks, and the average time to cash is nearly three months. Such challenges are driving customers' digital behavior to mobile devices to access digital lending applications.

- Government regulations also augment digital behavior among consumers. For instance, in December 2023, the Reserve Bank of India (RBI) announced plans to subject digital loan aggregators to a regulatory framework to enhance transparency in operations. This move underscores the RBI's commitment to overseeing its regulated entities and the lending service providers it collaborates with, ensuring the smooth provision of permissible credit facilitation services.

Asia-Pacific to Register Major Growth

- Digital lending has been available to credit unions for quite some time. However, with emerging technologies and the fast-paced nature of consumer lending, it is more important than ever that digital lending offers members more than a paperless process.

- In April 2024, the National Bank for Agriculture and Rural Development (NABARD) announced a strategic partnership with the Reserve Bank's subsidiary, RBIH, to streamline the processing of agricultural loans. NABARD is projected to merge its e-KCC loan origination system portal with the Public Tech Platform for Frictionless Credit (PTPFC) developed by the Reserve Bank Innovation Hub (RBIH).

- The rapid adoption of smartphones, internet access, and a shift toward consumerism in India helped fuel the growth of digital lending enterprises. Currently, there are 338 online lending start-ups in India that are trying to reduce the gap between lenders and creditors through a seamless process.

- Moreover, the Government of Japan is launching programs to inculcate cashless behaviors in citizens. The government launched an initiative to increase cashless payments to 40% by 2025. With the consumption tax increase from 8% to 10% on October 1, 2019, several discount schemes were implemented. These schemes subsidized the installation of cashless payment terminals for merchants and provided 2% or 5% discounts for consumers when purchasing from registered SMEs or franchise stores.

Digital Lending Industry Overview

The digital lending market is fragmented owing to the presence of several solution providers, none of which holds a majority share. Market players, such as Funding Circle Limited, On Deck Capital Inc., Prosper Marketplace Inc., LendInvest Limited, and Bizfi LLCare, are making several innovations to improve their offerings and gain maximum market traction. The emerging players in the market are strategically raising funds to provide innovative and technologically integrated solutions. The market players also view strategic collaborations as a lucrative path toward growth.

- July 2024: Salesforce, a leading CRM provider, unveiled its plans to launch 'Digital Lending for India.' This platform is designed to enable banks and lenders in India to adopt digital approaches to consumer lending. By doing so, they can streamline operations, reduce costs, and eliminate the challenges of managing outdated, disparate systems. 'Digital Lending for India' is tailored exclusively for the Indian market. Furthermore, it offers integration capabilities, allowing banks to merge their financial data with Salesforce's customer insights.

- May 2024: PhonePe launched its secure digital lending platform within its app. This platform allows over 535 million registered users to access loans across six categories, including mutual fund, gold, and car loans. The loans are provided in partnership with a network of banks, non-banking financial companies (NBFCs), and other fintech companies, including Tata Capital, L&T Finance, Hero FinCorp, and Muthoot Fincorp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKETDYNAMICS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Important Touchpoints of Potential Loan Purchasers

- 4.5 Impact of COVID-19 on the Digital Lending and Allied Markets

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Potential Loan Purchasers with Digital Behavior

- 5.2 Market Challenges

- 5.2.1 Security concerns

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Business

- 6.1.1.1 Business Digital Lending Market Dynamics

- 6.1.1.2 Business Digital Lending Ecosystem (Including both Startups and Incumbents)

- 6.1.2 By Consumer

- 6.1.2.1 Consumer Digital Lending Market Dynamics

- 6.1.2.2 Consumer Digital Lending Models (Payday Lenders, Peer-to-Peer Loans, Personal Loans, Auto Loans, and Student Loans)

- 6.1.2.3 Consumer Digital Lending Ecosystem (Including both Startups and Incumbents)

- 6.1.1 Business

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Funding Circle Limited (Funding Circle Holdings PLC)

- 7.1.2 Bizfi LLC

- 7.1.3 On Deck Capital Inc.

- 7.1.4 Prosper Marketplace Inc.

- 7.1.5 LendInvest Limited

- 7.1.6 LendingClub Corp.

- 7.1.7 Zopa Limited

- 7.1.8 Social Finance Inc.

- 7.1.9 Upstart Network Inc.

- 7.1.10 Kiva Microfunds

- 7.1.11 Kabbage Inc.

- 7.1.12 CAN Capital Inc.

- 7.1.13 Lendingtree Inc.

- 7.1.14 Kaspi Bank JSC

- 7.1.15 Klarna Bank AB

- 7.1.16 Ferratum Oyj

- 7.1.17 Provident Bank (Provident Financial Services Inc.)

- 7.1.18 International Personal Finance PLC (IPF)

- 7.1.19 Oriente

- 7.1.20 Faircent

- 7.1.21 LenDenClub

- 7.1.22 CapFloat Financial Services Private Limited

- 7.1.23 Transactree Technologies Private Limited (LendBox)

- 7.1.24 Monexo

- 7.1.25 i-LEND

- 7.1.26 Decimal Technologies Pvt. Ltd

8 INVESTMENT ANALYSIS AND MARKET OPPORTUNITIES