PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642066

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642066

France Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

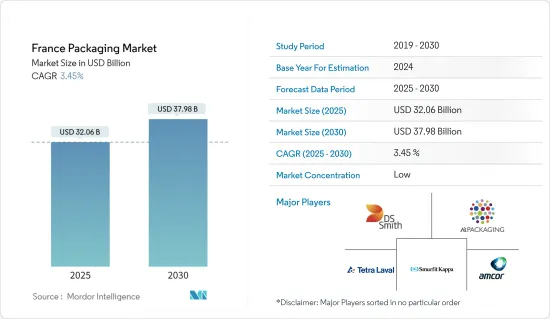

The France Packaging Market size is estimated at USD 32.06 billion in 2025, and is expected to reach USD 37.98 billion by 2030, at a CAGR of 3.45% during the forecast period (2025-2030).

The growing demand for packaging in France for the food and beverage industry is attributable to increasing tourism with increased emphasis on convenience, ready-to-eat, and value-priced foods.

Key Highlights

- According to the United States Department of Agriculture (USDA), the gross domestic product (GDP) in 2023 is estimated at USD 2.809 trillion. France is the world's seventh-largest economy and the second-largest in the EU. France has a flourishing food ingredient industry, producing a wide range of ingredients used domestically and exported worldwide, which signifies the demand for packaging in the country.

- Additionally, the growth in the number of tourists in France has stirred the demand for French food, an amalgamation of rich flavors and unique processes. The constant development and expansion of French food options in the country significantly drive the food industry in the country.

- French packaging manufacturers focus on reducing packaging waste by innovating new sustainable products. Consumer demand for eco-friendly products propels a notable shift towards sustainable packaging solutions. Materials that are biodegradable, compostable, and recyclable are becoming increasingly favored. In tandem, companies are prioritizing reducing plastic usage and embracing practices aligned with the circular economy.

- However, increasing regulations in the country against the use of plastic are anticipated to affect the market for plastic packaging in the country. For instance, the French Parliament's lower chamber passed a law in December 2020 that banned all single-use plastic products and packaging after 2040, in addition to several initiatives to increase reuse and recycling.

France Packaging Market Trends

Flexible Packaging to Have a Significant Share

- Flexible packaging is a means of packaging products using non-rigid materials, which allows for more economical and customizable options in France. As cheap and lightweight packaging is gaining popularity in the country, manufacturers are encouraged to use flexible packaging such as pouches, bags, and wraps for food, cosmetics, personal care, and E-commerce applications. Hence, these factors are responsible for boosting the market's growth.

- Pouch packaging is rapidly gaining popularity in France, as it is a highly convenient and portable solution. The growing popularity of pouch packaging, as it significantly uses less material than other containers and reduces food waste, drives the market growth. Consumers drove the demand for stand-up pouches (for snacks, beverages, baby food, or industrial oils and lubricants) exponentially over the past decade.

- French flexible packaging manufacturers, such as Amcor Group, provide flexible paper packaging solutions that help extend the shelf life of perishable food products. In December 2023, Amcor Group, a Swiss-based brand, supplied France-based cheese producer Fromagerie Milleret with recycle-ready paper flexible packaging for the company's Le Baron Brie and l'Ortolan Bio premium cheeses. Amcor's AmFiber Matrix packaging allows soft cheese producers to control the level of moisture within the product and the ripening process.

- French consumers are increasingly aware of the environmental implications of packaging. They are on the lookout for packaging solutions that strike a balance between functionality and eco-friendliness. According to the French Union of Carboard, Paper and Cellulose Industries (COPACEL), the distribution of paper and paperboard production in France for packaging, in 2020 was 64.3% and it has increased to 70% in 2023.

- Therefore, this shift in consumer preference has led to a heightened demand for sustainable and recyclable flexible packaging materials. In response, manufacturers of flexible packaging are pivoting towards these evolving demands, crafting innovative solutions that prioritize environmental consciousness.

Food Segment Expected to Dominate the Market

- France's rapidly growing food and food service industry drives the country's packaging market. As a result of these changes, new packaging styles, such as multi-packs and more miniature and more convenient single-serve packs, are becoming increasingly necessary. Flexible packaging and rigid plastics are the most popular materials in the French packaging market.

- French manufacturers are focusing on expanding paper manufacturing facilities to cater to the region's increasing demand for paper packaging. In May 2024, DS Smith, a British multinational company, announced an investment of EUR 6 million (USD 6.45 million) in its La Chevroliere facility in France.

- According to Agence Bio, the French Agency for the Development and Promotion of Organic Agriculture, the annual turnover of the organic food market in France, excluding restaurants and other food service facilities, was EUR 11.4 billion (USD 12.33 billion) in 2019 and reached EUR 12.08 billion (USD 13.07 billion) in 2023. The rise in the organic food market also promotes the packaging industry market across the country.

- French consumers have a penchant for clean, attractive designs that exude quality. Packaging that marries functionality with aesthetic appeal captures attention. This trend leans towards minimalism, advocating for less clutter on labels and emphasizing premium materials.

- Consumers are more curious than ever about their food's origins and production methods. Brands adopt packaging solutions that underscore traceability, featuring ingredient labels and sourcing details, including single-serve packages, resealable bags, and products designed for portion control.

France Packaging Industry Overview

The competitive landscape of the French packaging market is fragmented, with major players such as DS Smith PLC, AR Packaging Group AB, Smurfit Kappa Group PLC, and Tetra Pak International SA vying for larger market share. Moreover, the competition level among these vendors is high due to the various innovations and investments made by the companies. Companies are also undergoing acquisitions to strengthen their product portfolios and increase their market shares.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Macroeconomic Factors, such as Demographic Changes and Changing Consumer Preferences

- 4.2.2 Increasing Tourism in the Industry

- 4.3 Market Challenges

- 4.3.1 Increasing Regulations in the Country against the Use of Plastic

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Plastic

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Other Materials

- 5.2 Packaging Type

- 5.2.1 Flexible Packaging

- 5.2.2 Rigid Packaging

- 5.3 End-user Verticals

- 5.3.1 Food

- 5.3.2 Beverages

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Beauty and Personal Care

- 5.3.5 Other End-user Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AR Packaging Group AB

- 6.1.2 DS Smith PLC

- 6.1.3 Smurfit Kappa Group PLC

- 6.1.4 Tetra Pak International SA

- 6.1.5 Amcor PLC

- 6.1.6 Ball Corporation (Rexam PLC )

- 6.1.7 RPC Group PLC

- 6.1.8 Owens Illinois Inc.

- 6.1.9 Ardagh Group

- 6.1.10 Mondi PLC

- 6.1.11 Ametek Inc.

- 6.1.12 Crown Holding Inc.

- 6.1.13 Constantia Flexibles GmbH

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS