Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640604

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640604

APAC Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 100 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

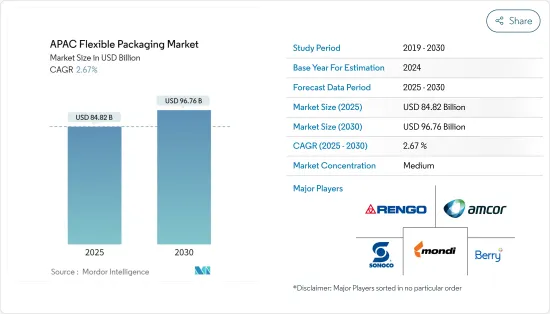

The APAC Flexible Packaging Market size is estimated at USD 84.82 billion in 2025, and is expected to reach USD 96.76 billion by 2030, at a CAGR of 2.67% during the forecast period (2025-2030).

Key Highlights

- Flexible packaging in Asia-Pacific is expected to witness a stable growth rate during the forecast period. Some of the prominent vendors in the region are focusing on the ever-growing concern regarding environmental sustainability by adopting efficient manufacturing techniques throughout the three stages of the packaging life cycle: manufacturing, transportation, and disposal.

- As retail sales surge, markets tend to expand, introducing new products and broadening the reach of existing ones. Diverse industries, ranging from food and beverages to pharmaceuticals and personal care, utilize flexible packaging due to its versatility across various product categories. Consequently, a rise in retail sales stands to bolster various segments of the flexible packaging market. In 2023, Japan's retail industry achieved sales of approximately JPY 163 trillion, marking its highest value over the previous 15 years, as reported by METI (Japan).

- There is a considerable increase in domestic demand for flexible packaging in Asia-Pacific, owing to the rapid urbanization across emerging economies, such as China and India. Healthy growth across end users in the region is further driving the need for flexible packaging products, primarily in the wraps and pouches segment, majorly to address the small quantity retailing needs of the rising middle-income population in the region.

- The demand for flexible packaging products is mainly driven by millennial consumers in the region, as they have an avid preference for single-serving and on-the-go style food and beverage products. As these products are generally designed to be portable, durable, and lightweight, flexible packaging is a popular option. The fastest-growing areas of snack foods, both in terms of fresh items and processed foods, are expected to govern the demand for flexible packaging from the food and beverage industry. In 2023, Bingo and Kurkure had the highest market share of over 10% each among the puffed snacks companies in India. This was followed by Taka Tak, with a 6% market share during the same period.

- The beverage industry offers potential growth opportunities for flexible packaging across the region. Food companies are expanding their businesses in terms of geography and product lines to cater to this rising demand. For instance, Shou Quan Zhai, founded in 1760 and one of the oldest food companies in China, expanded into the beverage industry with a new line of ready-to-drink products.

- In January 2024, Chinese beverage brands made strides in international markets, embedding themselves into local communities by offering consistent quality products and services. Mixue Group, hailing from Zhengzhou in Henan province and boasting a network of over 36,000 stores globally, took a significant step by filing for an initial public offering in Hong Kong. Such expansion in the beverage industry may further propel market growth.

- The Russia-Ukraine War caused fluctuations in global oil prices, directly impacting the cost of raw materials used in flexible packaging, such as plastics, polyethylene, polypropylene, and other petrochemical derivatives. These materials are essential for producing films, pouches, and wraps used in flexible packaging. The increased cost of petroleum-based products raised the production costs for flexible packaging manufacturers in the region, leading to price increases for end products.

APAC Flexible Packaging Market Trends

Expanding Food Industry Expected to Drive Market Growth

- Flexible packaging is commonly used for food products such as smoothies, snacks, dairy, confectionery, etc. Typical flexible food packaging applications include films, pouches, aluminum lids, and paper bags to package cheeses, meats, bread, and vegetables. This flexible packaging can be used as primary packaging as well as secondary packaging in some cases.

- The packaged food industry has been witnessing growth owing to innovations in food processing techniques and changes in consumer lifestyles. These trends are anticipated to eventually boost product demand, propelling the growth of the market during the forecast period. For instance, in February 2024, PepsiCo India introduced a new sub-brand, Lay's Shapez, to its potato chips lineup. The innovative product showcases heart-shaped pellets made from potatoes.

- Also, in August 2024, Uswatte Confectionery Works Pvt. Ltd, Sri Lanka's oldest confectionery manufacturer, announced the revival of its famous potato chip brand, Chirpy Chips. The company had previously discontinued the brand due to government policies restricting the import of high-quality potatoes into the country. This re-entry of potato snacks by confectionery manufacturers in Sri Lanka is expected to support market growth.

- Flexible packaging materials, such as multilayer films and laminates, provide significant barrier properties that protect food from moisture, oxygen, and contaminants. This helps to extend the shelf life of perishable items like dairy products, meat, and baked goods. Consumers and food manufacturers alike seek packaging solutions that maintain product freshness while also ensuring food safety, making flexible packaging a preferred choice.

- In 2023, online retail sales of soft drinks in Japan amounted to around USD 2.6 billion, making it the largest segment within the food-based e-commerce industry. According to the National Bureau of Statistics of China, in 2023, the annual revenue of the foodservice industry in China amounted to around CNY 5.3 trillion. This indicated an increase in revenue of approximately 20% compared to the previous year. Such expansion of e-commerce and food delivery services has accelerated the need for lightweight, durable, and protective packaging that can withstand the rigors of shipping. Flexible packaging fits these needs by being cost-effective and adaptable for both dry and liquid food products.

India Is Expected to Witness Significant Market Growth

- India is playing a significant role in driving the growth of the flexible packaging market due to its rapidly evolving economic, social, and industrial landscape. With a population of over 1.4 billion, India is one of the largest consumer markets in the world. Rapid urbanization is leading to lifestyle changes, with more people moving to cities and a higher demand for packaged goods. According to Bikaji, the market value of packaged food is likely to surpass INR 5 trillion by 2026.

- India's food and beverage industry is experiencing significant growth, driven by changing consumer preferences and increasing spending on processed and packaged foods. This industry is the largest end user of flexible packaging in the country. In 2023, the retail sales value of naturally healthy beverages in India was the highest for hot drinks at over USD 1.1 billion. Furthermore, the retail sales value of the naturally healthy beverages surpassed USD 1.6 billion that same year.

- The snacks market has been expanding in emerging economies, including India, creating a growth opportunity for market vendors due to the application of flexible packaging in making snack pouches, wraps, bags, and others. Additionally, Bikaji, a snack brand in India, reported that the savory snacks market in India witnessed growth in July 2023.

- India is a significant player in the global pharmaceutical industry, and the demand for flexible packaging is growing. Flexible packaging offers tamper-evident, moisture-resistant, and protective solutions for pharmaceutical products, including tablets, capsules, and syrups. As the healthcare sector expands, especially with the increasing focus on hygiene and safety post-COVID-19, flexible packaging plays an increasingly crucial role in ensuring product integrity and safety.

- There is growing awareness among Indian consumers and companies about the importance of sustainability and reducing plastic waste. This has led to improved demand for eco-friendly and recyclable flexible packaging materials. The Indian government has introduced policies such as the ban on single-use plastics and initiatives promoting sustainable practices. These regulations are pushing manufacturers toward innovative packaging solutions like biodegradable and compostable flexible packaging.

APAC Flexible Packaging Industry Overview

The APAC flexible packaging market is fragmented, with the presence of significant companies like Amcor Ltd, Berry Plastics Corporation, Mondi Group, Sonoco Products Company, and Rengo Co. Ltd. The companies continuously invest in strategic collaborations and product developments to gain market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 55595

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of Key Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Convenient Packaging

- 5.1.2 Demand for Longer Shelf Life and Innovative Packaging

- 5.2 Market Restraints

- 5.2.1 Concerns About the Environment and Recycling of Packaging Material

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Pouches

- 6.1.2 Bags

- 6.1.3 Wraps

- 6.1.4 Other Types

- 6.2 By Material

- 6.2.1 Plastic

- 6.2.2 Paper

- 6.2.3 Aluminum/Composites

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.3 Pharmaceutical and Medical

- 6.3.4 Household and Personal Care

- 6.3.5 Other End-user Industries

- 6.4 By Country

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 Australia

- 6.4.5 Rest of Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Ltd

- 7.1.2 Berry Plastics Corporation

- 7.1.3 Mondi Group

- 7.1.4 Sonoco Products Company

- 7.1.5 Rengo Co. Ltd

- 7.1.6 Sealed Air Corporation

- 7.1.7 Formosa Flexible Packaging Corp

- 7.1.8 Wapo Corporation Ltd

- 7.1.9 Chuan Peng Enterprise Co. Ltd

- 7.1.10 TCPL Packaging Ltd

- 7.1.11 Ester Industries Ltd (Wilemina Finance Corporation)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.