PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640469

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640469

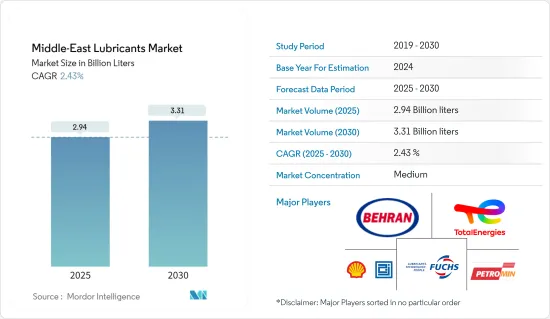

Middle-East Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Middle-East Lubricants Market size is estimated at 2.94 billion liters in 2025, and is expected to reach 3.31 billion liters by 2030, at a CAGR of 2.43% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, the manufacturing industry was severely affected, and this resulted in a decrease in the use of lubricants in 2020. However, with the recovery of many construction projects and other industrial activities, the market saw a recovery phase in the year 2021. It is expected to see a positive trend in the forecasted years. An increase in automotive sales and engineering goods has been leading the market recovery over the last two years.

The industrial growth in Saudi Arabia, Iran, and the United Arab Emirates and the growing usage of high-performance lubricants are the major driving factors augmenting the growth of the market studied.

On the flip side, costlier high-performance lubricants are expected to hinder the growth of the market.

Developments in synthetic and bio-based lubricants are projected to act as an opportunity for the market in the future.

Saudi Arabia emerged as the largest market for lubricants and is expected to register the highest CAGR during the forecast period.

Middle East Lubricants Market Trends

Automotive Sector to Dominate the Market

- Lubricants are typically used for applications such as wear reduction, corrosion protection, and ensuring smooth operation of the engine internals.

- High-mileage engine oils are experiencing great demand owing to specific properties, such as oil leak prevention and reduction in oil burn-off.

- Most light and heavy vehicle diesel and gasoline engines use 10W40 and 15W40 viscosity grade oils, while multi-grade oils, such as 15W50 and 20W50, are commonly used for aircraft engines.

- The average vehicle age has been increasing at a constant rate over the years, which is an opportunity in terms of the aftermarket refill market. The increasing average age of passenger cars and the growing urban population in developing countries is expected to drive the market for lubricants in transportation.

- The automotive industry is essential to the country's socio-economic development. According to some local automotive industry experts, despite the growing electric vehicle sales worldwide, Saudi Arabia expects internal combustible engines (ICE) vehicles to make up the majority of cars driven in for the next 15-20 years.

- Some of the major players controlling the automotive industry in the country include Toyota, with a 30% share, followed by Hyundai and KIA, with 26%, and Renault-Nissan-Mitsubishi, with 9%. General Motors, Ford, and Fiat Chrysler Automobiles comprise the remaining share.

- Saudi Arabia aims to localize the automotive sector and increase investment opportunities to achieve the national strategy's objectives for the industry in developing local manufacturing capabilities in line with the goals of the Kingdom's Vision 2030.

- The Iran automotive market has witnessed a rise over the historic period, with demand for production increasing in the country. For instance, according to the OICA, car manufacturing in Iran increased by 19% in 2022, as the country manufactured 1.064 million vehicles in 2022, while the passenger vehicles produced were around 894,000 units in 2021.

- The International Organization of Motor Vehicle Manufacturers (known as OICA) ranked Iran sixth in the world in terms of car manufacturing growth in 2022.

- Also, as per the European Automobile Manufacturers' Association (ACEA), the organization ranked Iran as the world's 11th largest automaker in 2022.

- The United Arab Emirates automotive market has been experiencing a rise in vehicle registrations over the current period, with demand in production and sales increasing in the country.

- As per industry sources, the country's automotive vehicle registration in the period January to September 2023 stood at 193,698, up 20.2% in comparison to the same period in the previous year.

- Moreover, in 2022, the country's car market sold over 400,000 new cars, representing a 10% increase over the previous year. This growth is expected to continue in the coming years, driven by the country's growing population and rising incomes.

- Thus, the factors above are expected to augment the growth of the market studied in the region during the forecast period.

Saudi Arabia is Expected to Experience a Surge in Growth

- Saudi Arabia is the largest economy in the Middle East region. Saudi Arabia's economy is mainly dependent on the oil industry.

- Saudi Arabia is one of the largest automotive markets in the GCC. Passenger cars account for approximately 80% of the region's automotive market.

- Saudi Arabia is enhancing the capacity of its power sector (electricity generation, transmission, distribution, and smart grid) to meet increasing demand efficiently from residential and commercial consumers for electricity and to support the diversification of its domestic energy mix.

- According to the Ministry of Energy, Saudi Arabia's spending on power and renewable energy projects is expected to reach USD 293 billion by 2030. Additionally, in December 2021, Saudi Arabia's Energy Minister announced the country's plan to spend USD 38 billion on energy distribution by 2030.

- Saudi Arabia emerged as a rapidly growing energy consumer. With the increasing demand for electricity in the country, the power generation infrastructure has been growing. It is estimated that the country is required to increase its power generation capacity to 160 GW by 2040 to fulfill its increasing demand. To achieve this, the government is planning to make an annual investment of around USD 5 billion in generation and USD 4 billion in distribution (D&T). The National Renewable Energy Program in the country aims to increase the generation of renewable energy to 9.5 GW by 2023.

- Consistent lubrication is vital to the life of bearings, gears, and chains. Like any mechanical system, moving parts in a food and beverage plant need proper lubrication to function optimally. Contamination, moisture, high temperatures, and humidity are all threats to bearing, chain, and gear service life. Saudi Arabia is heavily investing in metal industries. According to the World Steel Association, Saudi Arabia's crude steel production in 2023 observed an increase of about 0.8% as compared to 2022 and produced approximately 9.9 million metric tons of steel.

- In December 2023, the Saudi Arabian government announced to investment of about USD 12 billion in steel projects to increase steel production and meet the significant growth in domestic demand. The project is planned to have a total production capacity of about 6.2 million tons.

- Nestle has announced an initial investment of SAR 375 million (USD 99.72 million) with the establishment of a manufacturing plant in 2025, followed by a regional center with a research and development program and its first business incubator for small and medium-sized companies and start-ups.

- A significant amount of lubricants are used in oil and gas exploration. These factors are expected to drive the market slowly over the forecast period in the United Arab Emirates.

Middle East Lubricants Industry Overview

The Middle-East lubricants market is fragmented. The major companies (in no particular order) include TotalEnergies, Petromin, Aljomaih, Shell Lubricating Oil Company (JOSLOC), Behran Oil Co., and FUCHS, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Industrial Growth in Saudi Arabia, Iran, and the United Arab Emirates

- 4.1.2 Growing Usage of High-performance Lubricants

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Costlier High Performance Lubricants

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Group

- 5.1.1 Group I

- 5.1.2 Group II

- 5.1.3 Group III

- 5.1.4 Group IV (PAO)

- 5.1.5 Naphthenics

- 5.2 Base Stock

- 5.2.1 Bio-based Lubricant

- 5.2.2 Mineral Oil Lubricant

- 5.2.3 Synthetic Lubricant

- 5.2.4 Semi-synthetic Lubricant

- 5.3 Product Type

- 5.3.1 Engine Oil

- 5.3.2 Transmission and Hydraulic Fluid

- 5.3.3 Metalworking Fluid

- 5.3.4 General Industrial Oil

- 5.3.5 Gear Oil

- 5.3.6 Greases

- 5.3.7 Process oils

- 5.3.8 Other Product Types (Turbine oils, Refrigeration oils, Aviation oils, Marine oils, and Transformer oils)

- 5.4 End-user Industry

- 5.4.1 Power Generation

- 5.4.2 Automotive and Other Transportation

- 5.4.3 Heavy Equipment

- 5.4.4 Food and Beverage

- 5.4.5 Metallurgy and Metalworking

- 5.4.6 Chemical Manufacturing

- 5.4.7 Other End-user Industries (Marine, Textiles, Manufacturing, and Oil and gas)

- 5.5 Geography

- 5.5.1 Saudi Arabia

- 5.5.2 Iran

- 5.5.3 Iraq

- 5.5.4 United Arab Emirates

- 5.5.5 Kuwait

- 5.5.6 Rest of Middle-East

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aljomaih And Shell Lubricating Oil Company Limited

- 6.4.2 AMSOIL INC.

- 6.4.3 Behran Oil Co.

- 6.4.4 Emarat

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 FUCHS

- 6.4.7 GP Global MAG LLC

- 6.4.8 GULF OIL Middle East Limited (Gulf Oil International Ltd.)

- 6.4.9 Idemitsu Kosan Co., Ltd.

- 6.4.10 IRANOL (LLP)

- 6.4.11 Lubrex FZC

- 6.4.12 Pars Oil Company

- 6.4.13 Petromin

- 6.4.14 Saudi Arabian Oil Co.

- 6.4.15 Sepahan Oil Company

- 6.4.16 TotalEnergies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments in Synthetic and Bio-based Lubricants

- 7.2 Other Opportunities