PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907258

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907258

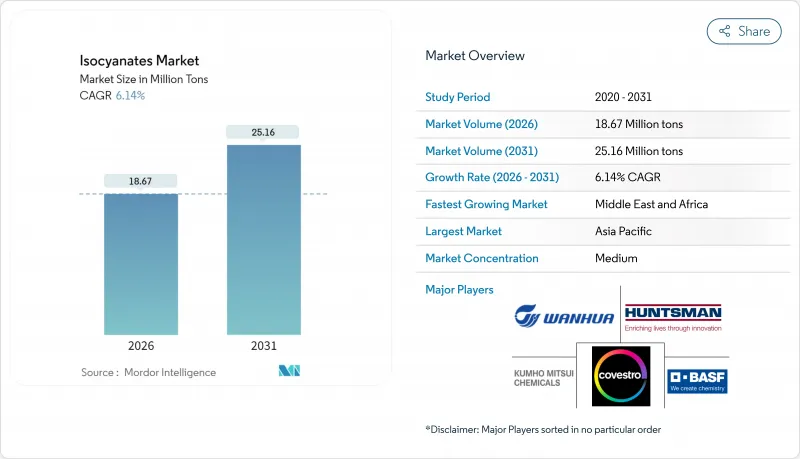

Isocyanates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Isocyanates market size in 2026 is estimated at 18.67 million tons, growing from 2025 value of 17.59 million tons with 2031 projections showing 25.16 million tons, growing at 6.14% CAGR over 2026-2031.

This trajectory reflects escalating adoption of high-performance polyurethane systems, supply-side consolidation, and tightening environmental regulations that reward vertically integrated producers. Rigid foam maintains momentum as efficiency standards raise thermal-insulation baselines, while automotive lightweighting broadens specialized demand beyond strictly construction uses. Integrated feedstock strategies, trade-policy shifts, and a pivot toward premium aliphatic chemistries further shape competitive positioning within the isocyanates market.

Global Isocyanates Market Trends and Insights

Surging Demand for Rigid PU Foam in Building Insulation

Revisions to the 2024 International Building Code mandate NFPA 285 fire testing for exterior wall assemblies that contain combustible insulation, making proven isocyanate-based systems the low-risk route for specifiers. Polyisocyanurate boards offer thermal conductivity as low as 0.018 W/m*K, allowing for thinner wall assemblies compared to mineral wool in retrofit settings where space is limited. State energy codes now cite ASHRAE 90.1 more frequently, pushing builders to higher R-values that rigid polyurethane can achieve within existing envelopes. The isocyanates market, therefore, benefits from retro-demand as older structures upgrade to meet net-zero targets. Global green-building certifications also favor materials with established life-cycle data, giving MDI-based foams a further compliance edge.

Rapid Industrialization and Urbanization in APAC

Southeast Asian economies are scaling manufacturing bases beyond China, creating new intra-regional demand pools for MDI and TDI. Producers with units in Vietnam, Thailand, and Indonesia can meet the rising local consumption while mitigating geopolitical-driven supply-chain risks. Tosoh's 130,000-tpy MDI plant in Vietnam exemplifies this diversification strategy. Large-scale urban housing and transportation projects across ASEAN are driving demand for insulation, sealants, and composite panels, all of which rely on isocyanate chemistries. As income levels rise, consumption of durable goods-especially mattresses and appliances-drives steady demand for flexible foam. These structural shifts keep the isocyanates market on a multi-year growth path, irrespective of export softness elsewhere.

Volatile Benzene and Nitro-Benzene Feedstock Pricing

Benzene is the primary aromatic precursor for both MDI and TDI, so any spike in crude-linked naphtha values cascades directly into isocyanate manufacturing costs. Spot benzene in Asia swung, forcing producers to issue monthly price-adjustment clauses that eroded buyer visibility. Margins compress fastest for non-integrated converters that lack backward links to aromatics, encouraging vertical integration or long-term offtake contracts. Inventory strategies are evolving toward hedged positions that cover at least three months of demand to cushion volatility; however, this ties up working capital and raises carrying costs. The net result is a dampening effect on short-term consumption growth as formulators delay orders when the feedstock price direction is unclear.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Vehicle Trend Driving PU Composites Adoption

- Cold-Chain and E-Commerce Packaging Growth

- EU REACH Training and Classification Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MDI held a 58.75% market share of the isocyanates market in 2025, backed by its versatility in rigid foam and composite formulations that serve high-volume construction and industrial applications. At the same time, aliphatic isocyanates are tracking a 6.72% CAGR that outpaces the overall isocyanates market, with UV-stable HDI and IPDI penetrating automotive clearcoat and wind-blade resin systems where long-term durability commands premium prices. TDI demand remains resilient in bedding and furniture, but growth is slower as the segment reaches maturity and competitive pressure from viscoelastic MDI systems intensifies. Specialty blocked and pre-polymer variants, while low volume, offer elevated margins by targeting electronics encapsulation, marine coatings, and aerospace composites.

The isocyanates market size for aliphatic grades is set to climb steadily as OEM specifications in both automotive and renewable-energy sectors pivot to durability metrics that aromatic chemistries struggle to meet. Producers are investing in additional HDI monomer loops to shorten supply chains for downstream polyisocyanate production, anticipating regional content rules in North America and Europe. Meanwhile, MDI suppliers are adding capacity to address bottlenecks to retain cost leadership, highlighting a dual-track investment landscape that balances commodity scale with specialty value capture.

The Isocyanates Market Report is Segmented by Type (MDI, TDI, Aliphatic, and Other Types), Application (Rigid Foam, Flexible Foam, Paints and Coatings, Adhesives and Sealants, and More), End-User Industry (Building and Construction, Automotive, Healthcare, Furniture, and Other End-Users), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 46.85% of the isocyanates market share in 2025, a lead secured by China's benzene-advantaged MDI complexes and Southeast Asia's emerging manufacturing corridors that shorten delivery times to regional converters. The consolidation of smaller Chinese plants under stricter emissions regulations is driving volume toward large operators that can leverage economies of scale while meeting environmental targets. Vietnamese and Indonesian downstream clusters are also scaling rigid-foam and footwear production, reinforcing a self-sustaining demand loop that cushions the region from export swings.

North America holds a significant position, benefiting from shale-advantaged feedstock and proximity to the automotive and construction sectors, which anchor polyurethane consumption. BASF's ongoing expansion at Geismar, Louisiana, will lift regional MDI nameplate capacity to roughly 600,000 t/y in 2026, ensuring supply sufficiency as electric-vehicle output scales. Trade-policy uncertainty, exemplified by the 2025 USITC antidumping probe into Chinese MDI, encourages dual sourcing and supports domestic plant utilization. Europe, while technologically advanced, contends with REACH training costs that nudge smaller converters toward offshore sourcing, modestly softening local growth prospects despite continued retro-insulation activity.

The Middle-East and Africa are projected to experience the fastest regional expansion at a 6.25% CAGR to 2031, as governments fund mega-infrastructure projects and petrochemical self-sufficiency programs. State-backed players leverage low-cost propane dehydrogenation and benzene extraction to feed integrated MDI and TDI units. The construction of smart cities and healthcare complexes-particularly in the Gulf Cooperation Council-drives demand for high-performance insulation and sealants, further amplifying the regional isocyanates market size trajectory. Producers with assets in Oman and Saudi Arabia can also back-integrate into basic aromatics, enhancing margin capture under volatile global benzene pricing.

- Anderson Development Company

- Asahi Kasei Chemicals

- BASF SE

- BorsodChem

- Chemtura Corp.

- China National Bluestar (Group) Co. Ltd.

- Covestro AG

- Dow Inc.

- Evonik Industries

- Huntsman Corporation LLC

- Kemipex

- Korea Fine Chemical Co. Ltd.

- Kumho

- MITSUI CHEMICALS AMERICA INC.

- Perstorp

- Tosoh Corporation

- Vencorex

- Wanhua Chemical Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for rigid PU foam in building insulation

- 4.2.2 Rapid industrialization and urbanization in APAC

- 4.2.3 Lightweight vehicle trend driving PU composites adoption

- 4.2.4 Cold-chain and e-commerce packaging growth

- 4.2.5 Wind-turbine blade production using isocyanate composites

- 4.3 Market Restraints

- 4.3.1 Volatile benzene and nitro-benzene feedstock pricing

- 4.3.2 EU REACH training and classification hurdles

- 4.3.3 Supply tightness from China environmental shutdowns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Price Trend

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 MDI

- 5.1.2 TDI

- 5.1.3 Aliphatic (e.g., HDI, IPDI)

- 5.1.4 Other Types

- 5.2 By Application

- 5.2.1 Rigid Foam

- 5.2.2 Flexible Foam

- 5.2.3 Paints and Coatings

- 5.2.4 Adhesives and Sealants

- 5.2.5 Elastomers

- 5.2.6 Binders

- 5.2.7 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Healthcare

- 5.3.4 Furniture

- 5.3.5 Other End-users (Aerospace, Electronics, Marine)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Turkey

- 5.4.5.5 Egypt

- 5.4.5.6 Nigeria

- 5.4.5.7 South Africa

- 5.4.5.8 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Anderson Development Company

- 6.4.2 Asahi Kasei Chemicals

- 6.4.3 BASF SE

- 6.4.4 BorsodChem

- 6.4.5 Chemtura Corp.

- 6.4.6 China National Bluestar (Group) Co. Ltd.

- 6.4.7 Covestro AG

- 6.4.8 Dow Inc.

- 6.4.9 Evonik Industries

- 6.4.10 Huntsman Corporation LLC

- 6.4.11 Kemipex

- 6.4.12 Korea Fine Chemical Co. Ltd.

- 6.4.13 Kumho

- 6.4.14 MITSUI CHEMICALS AMERICA INC.

- 6.4.15 Perstorp

- 6.4.16 Tosoh Corporation

- 6.4.17 Vencorex

- 6.4.18 Wanhua Chemical Group Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment