PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639500

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639500

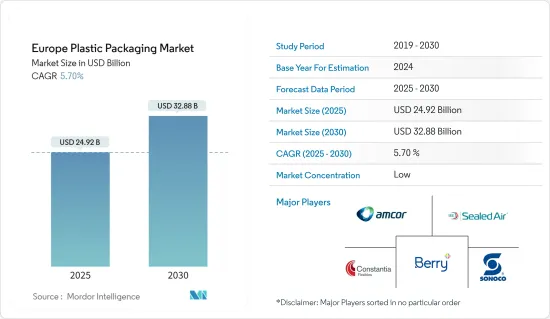

Europe Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe Plastic Packaging Market size is estimated at USD 24.92 billion in 2025, and is expected to reach USD 32.88 billion by 2030, at a CAGR of 5.7% during the forecast period (2025-2030).

The increasing technological advancements and end-user industry packaging applications are the significant factors driving the market growth studied.

Key Highlights

- In most European countries, the population is growing, and the use of packaging per person is increasing. It is due to consumer behavior trends, such as the growth in the use of convenience products and the increasing use of plastic as a substitute for other packaging materials.

- The market is driven by several reasons, with different effects over the short, medium, and long-term periods. These causes include a consistent increase in the demand for processed foods and the adoption of lightweight flexibles. Additionally, there is a rise in demand for frozen food packaging due to customer appreciation of the quality of local products. The need for frozen food packaging has expanded in Europe due to the expansion of the economy and shifting lifestyles, and the market is anticipated to grow profitably over the next years.

- The demand for plastic packaging continues to rise in Europe even though serious concerns are being raised about its impact on the environment. However, the market also faces challenges due to the government regulations in Europe and increasing consumer demand that pushes manufacturers to look for plastic packaging solutions that are biodegradable or derived from sustainable sources.

- The market is expected to face significant challenges due to dynamic changes in regulatory standards, mainly due to growing environmental concerns. The region's government has responded to public concern about plastic packaging waste, especially plastic packaging waste, by introducing regulations to minimize environmental waste and improve waste management processes.

- The European Plastics Converters (EuPC) is composed of 50,000 SMEs, and it is currently working to mitigate the effects of the coronavirus crisis. Industries and authorities are directing their full attention to the management of the crisis, and they have put on hold all inessential activities to concentrate on the health and safety of the European citizens.

Europe Plastic Packaging Market Trends

Flexible Packaging to Grow Significantly

- The retail industry is expanding due to rising demand for packaged food and non-food items across Europe. It creates a one-of-a-kind demand for flexible packaging solutions, which is expected to accelerate the growth of the plastic packaging market significantly.

- Flexible packaging increases product sustainability by increasing shelf life and enabling the introduction of new products, such as frozen food, which can realize through flexible packaging. Food production experienced an unprecedented surge at the pandemic's start, while some fast-moving consumer goods (FMCG) manufacturers repurposed production lines.

- Various vendors have been focusing on strengthening their position in flexible packaging, broadening their portfolio of sustainable solutions, and expanding their regional reach. In May 2022, FlexCollect, one of the most significant collaborative projects to support the collection and recycling of flexible plastic packaging in the United Kingdom, launched UK Research and Innovation (UKRI) support. FlexCollect would also help organizations understand how to incorporate flexible plastic packaging into existing household collection services across various geographies and demographics to maximize recovery and recycling.

- In March 2022, UK Research and Innovation's (UKRI) Smart Sustainable Plastic Packaging (SSPP) Challenge announced GBP 30 million (USD 39 million) in funding for 18 collaborative projects that support the achievement of the UK Plastics Pact and have the potential to alter the UK's relationship with and management of, plastic packaging. The SSPP Challenge represents one of the largest government investments in sustainable plastic packaging and waste management. The results of the two funding competitions witness 5 large-scale demonstrator projects, and 13 business-led research and development projects benefit from this backing.

- Further, due to many improvements in Germany by solution providers and various end users, flexible plastic packaging solutions are increasingly being adopted. The usual customer view of "Made in Germany" products has given the area's local, flexible packaging businesses an ideal performance environment. The German government has enacted several strict laws for the country's plastic packaging sector. The German package Law mandates using recyclable and renewable materials and package design for recycling and recyclability. By 2022, the government wanted to recycle 63 percent more plastic packaging than in 2018, up from 40 percent. Such actions are anticipated to significantly influence the target market in the expected time frame.

Beverage Segment is Expected to Witness Significant Growth

- The beverage industry plays an essential role in the European region. The primary factors driving the region's growth in the beverage industry include steadily increasing population, per capita income, and changing lifestyles. Furthermore, factors such as high disposable income, ease of availability, improved living standards, a diverse product offering, and the presence of domestic and international players in the market fuel the beverage industry in the region.

- Many of the leading brands in Europe have a variety of fruit and sweet-flavored non-alcoholic beverages, and these are the most popular products. Besides, the EMA has introduced an initiative encouraging manufacturers to cut salt, sugar, and fat content in food and beverages. Companies that have pledged to follow this include Mars and Nestle.

- Furthermore, it is anticipated that Europeans would prioritize off-premise consumption over on-premise consumption when alcohol consumption rises steadily once the lockdown limitations are relaxed. Alcohol consumption outside licensed establishments is beneficial for expanding the flexible packaging industry. In the industry under study, alcoholic beverages sold in single-serve pouches are only a few significant examples of products becoming increasingly popular.

- Suntory, the beverage company in the region, has pledged to eliminate virgin plastics, such as fossil-fuel-based plastics, from its packaging portfolio by 2030. Such initiatives from other industry players may limit the market's growth during the forecast period.

- Moreover, the companies are investing in beverage manufacturing capacity expansion. For instance, in May 2022, Ecotone, a specialized player in organic and plant-based alternatives in Europe, announced a EUR 20 million (USD 21.5 million) investment in its plant-based beverage production site in Badia Polesine, Northern Italy. The significant investment has enabled the creation of a new production line, making it one of the key players in European plant-based drinks producers. This new site and production line will allow the multinational food company to produce an additional 27 million liters of plant-based beverages per year, a 30 percent increase in production capacity.

- The Economic Association of Non-Alcoholic Beverages estimates that the typical German used 6.6 liters of energy and mineral drinks in 2022 and 6.4 liters in the previous year. To accommodate the rising number of goods, there will likely be a more significant demand for packaging materials as mineral and energy drink consumption rise. This may increase the need for plastic bottles, caps, and other packaging elements, especially for these drinks.

Europe Plastic Packaging Industry Overview

The Europe Plastic Packaging Market is fragmented, owing to multiple players in the market. The major players are adopting strategies like product innovation, mergers and acquisitions, and expansion to stay competitive in the region. Some of the major players in the market are Amcor PLC, Sealed Air Corporation, and Berry Global Inc., among others.

- January 2024 -Berry Global Group, Inc. showcased high-performance alternatives to PVC cling films. According to the packaging giant, the new film represents a 'high-quality' alternative solution to hard-to-recycle PVC films for private label manufacturers, offering usability and clarity while lowering packaging weights for improved yields and delivering adequate product protection and maximum on-shelf appeal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight-packaging Methods

- 5.1.2 High Demand from the Skin Care Segment

- 5.2 Market Restraints

- 5.2.1 High Price of Raw Material

6 Trade Analysis and Current Supply Chain Scenario in Europe

7 MARKET SEGMENTATION

- 7.1 Type

- 7.1.1 Rigid Plastic Packaging

- 7.1.2 Flexible Plastic Packaging

- 7.2 Material Type

- 7.2.1 PE (Polyethylene)

- 7.2.2 PP (Polypropylene)

- 7.2.3 PVC (Polyvinyl Chloride)

- 7.2.4 PET (Polyethylene Terephthalate)

- 7.2.5 Other Material Types

- 7.3 End-user Industry

- 7.3.1 Food

- 7.3.2 Healthcare and Pharmaceutical (includes OTC)

- 7.3.3 Beverage

- 7.3.4 Cosmetics and Personal Care

- 7.3.5 Other End-user Industries

- 7.4 Country

- 7.4.1 United Kingdom

- 7.4.2 Germany

- 7.4.3 France

- 7.4.4 Spain

- 7.4.5 Italy

- 7.4.6 Poland

- 7.4.7 Rest of Europe

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Amcor PLC

- 8.1.2 Coveris Holdings

- 8.1.3 Sealed Air Corporation

- 8.1.4 Berry Global Inc.

- 8.1.5 Constantia Flexibles GmbH

- 8.1.6 Sonoco Products Company

- 8.1.7 Berry Global Inc.

- 8.1.8 Huhtamaki Group

- 8.1.9 Albea SA

- 8.1.10 Quadpack Industries SA

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET