PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636422

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636422

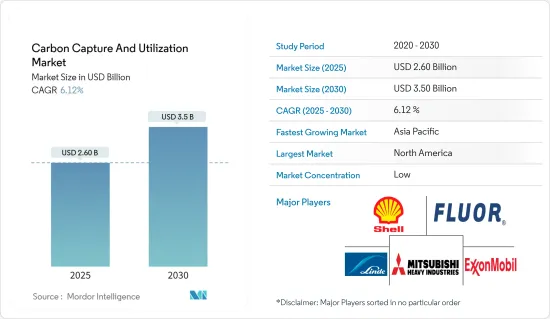

Carbon Capture And Utilization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Carbon Capture And Utilization Market size is estimated at USD 2.60 billion in 2025, and is expected to reach USD 3.50 billion by 2030, at a CAGR of 6.12% during the forecast period (2025-2030).

The carbon capture and utilization (CCU) sector is swiftly advancing, centered on capturing carbon dioxide (CO2) emissions from industrial processes or the atmosphere, and repurposing them into valuable commodities. These technologies play a pivotal role in curbing greenhouse gas emissions, combating climate change, and simultaneously generating economic benefits.

The CCU market is driven by several factors, including increasing awareness of climate change, stringent government regulations to reduce emissions, and the growing demand for sustainable products. CCU technologies offer a way to reduce CO2 emissions while producing valuable products, such as chemicals, fuels, and building materials, thereby creating a circular economy approach.

The CCU market is poised for significant growth as governments, industries, and consumers increasingly prioritize sustainable solutions to combat climate change. Continued innovation and collaboration among stakeholders will be vital to unlocking the full potential of CCU technologies and achieving global climate goals.

Carbon Capture And Utilization Market Trends

Oil & Gas Industry was the Major End User in Market

The oil and gas industry stands out as a significant adopter of carbon capture and utilization (CCU) technologies, driven by its substantial carbon dioxide (CO2) emissions, notably in fossil fuel production and refining.

Originally pioneered in the oil and gas domain, CCUS technologies sequester CO2 in deep geological formations, both onshore and offshore. While CO2 is typically immiscible with oil, its injection into reservoirs boosts pressure, aiding in oil movement towards production wells.

CCU technologies empower the oil and gas industry to not only capture but also repurpose CO2 emissions, thereby lessening their environmental impact. The repurposed CO2 finds diverse applications, from enhancing oil recovery (EOR) and serving as a feedstock for chemical and fuel production to being utilized in concrete carbonation for construction. Through the adoption of CCU technologies, the oil and gas industry not only reduces its carbon footprint but also broadens its revenue streams, thereby fostering a more sustainable energy landscape.

North America Holds Largest Share in Carbon Capture and Utilization Market

North America holds the largest carbon capture and utilization (CCU) market share, driven by several factors, including strong government support, technological advancements, and a well-established industrial base. The region has been at the forefront of developing and implementing CCU technologies, with the United States and Canada leading in the research, development, and deployment of these technologies.

The United States, in particular, has many CCU projects and initiatives supported by federal funding and incentives. The country's vast industrial sector, including the oil and gas industry, provides ample opportunities for CCU implementation. Moreover, the mounting emphasis on curbing carbon emissions and addressing climate change has hastened the uptake of CCU technologies in North America.

North America is poised to lead the CCU market, propelled by technological strides, favorable governmental measures, and a growing recognition of the imperative for sustainable climate change solutions.

Carbon Capture And Utilization Industry Overview

The carbon capture and utilization market is fragmented and consists of many players. Carbon capture and utilization (CCU) companies are adopting various strategies to drive growth and innovation in the market. One key strategy is to develop cost-effective and scalable CCU technologies that can capture and utilize carbon dioxide (CO2) emissions from industrial processes or the atmosphere. The key players include Royal Dutch Shell PLC, Fluor Corporation, Mitsubishi Heavy Industries Ltd, Linde PLC, and Exxon Mobil Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Environmental Regulations and Climate Change Goal

- 4.2.2 Growing Focuse on Reducing Co2 Emission

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs

- 4.3.2 Limited Storage Capacity

- 4.4 Market Opportunties

- 4.4.1 Research and Development Efforts in CCUS Technologies

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness: Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Advancements in the Industry

- 4.8 Insights on Various Regulatory Trends Shaping the Market

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Capture

- 5.1.2 Transportation

- 5.1.3 Utilization

- 5.1.4 Storage

- 5.2 By Technology

- 5.2.1 Pre-combustion Capture

- 5.2.2 Oxy-fuel Combustion Capture

- 5.2.3 Post-combustion Capture

- 5.3 By End User

- 5.3.1 Oil and Gas

- 5.3.2 Power Generation

- 5.3.3 Iron and Steel

- 5.3.4 Chemical and Petrochemical

- 5.3.5 Cement

- 5.3.6 Other End Users

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 India

- 5.4.1.2 China

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 Rest of Asia- Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Rest of North America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.3 ExxonMobil Corporation

- 6.4 Royal Dutch Shell PLC

- 6.5 Chevron Corporation

- 6.6 TotalEnergies SE

- 6.7 BP plc

- 6.8 Equinor ASA

- 6.9 Mitsubishi Heavy Industries Ltd

- 6.10 Air Products and Chemicals Inc.

- 6.11 Aker Solutions ASA

- 6.12 Schlumberger Limited

7 MARKET FUTURE TRENDS

8 DISCLAIMER AND ABOUT US