PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636253

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636253

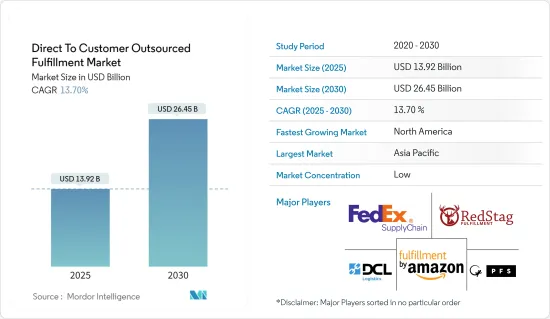

Direct To Customer Outsourced Fulfillment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Direct To Customer Outsourced Fulfillment Market size is estimated at USD 13.92 billion in 2025, and is expected to reach USD 26.45 billion by 2030, at a CAGR of 13.7% during the forecast period (2025-2030).

Companies often turn to outsourcing fulfillment as a key strategy for handling D2C orders. This approach entails enlisting a third-party logistics provider (3PL) to oversee warehouse, inventory, and shipping tasks. Outsourcing fulfillment appeals to firms lacking the in-house resources or expertise to manage these operations. By partnering with a 3PL, companies tap into their expertise and infrastructure, streamlining the fulfillment process. While this strategy helps cut fixed costs-like those associated with setting up and staffing a warehouse-it also allows companies to sharpen their focus on core competencies. Yet, relinquishing some control over the fulfillment process can potentially impact the overall customer experience.

In January 2024, Apollo Supply Chain, the logistics arm of Apollo Group, unveiled a new, all-encompassing e-commerce fulfillment and shipping service tailored for D2C brands. Industry insiders predict that India's D2C landscape, already bustling, could burgeon into a USD 60 billion industry by 2027.

Moreover, in June 2023, Alaiko, a prominent direct-to-consumer e-commerce fulfillment entity in Europe, made a strategic move by venturing into the United Kingdom. Alaiko forged a partnership with a cutting-edge fulfillment center in the north of London to cater to the local market. Setting itself apart, Alaiko prides itself on being a technology-centric fulfillment service. Its proprietary platform, Alaiko Logistics Operating System, coupled with advanced warehouse tech and robotics, empowers businesses to handle their e-commerce operations seamlessly.

This move offers UK e-commerce ventures a distinctive fulfillment avenue and positions them for smooth scalability domestically and across Europe. Opting for Alaiko translates to swifter deliveries and simplified returns, thanks to its expanding network of fulfillment hubs across Europe. By storing products within the European Union and facilitating direct shipping, Alaiko ensures rapid national and cross-border deliveries, sidestepping potential customs hurdles.

The D2C outsourced fulfillment market teems with competition as a multitude of providers vies, each boasting distinct service quality, pricing structures, and expertise, often specializing in niche product categories like fashion, electronics, or health and beauty.

Direct To Customer Outsourced Fulfillment Market Trends

Warehousing and Storage Segment to Drive Market Growth in the Near Future

- The surge in online shopping is transforming how warehouses operate. As online shopping gains traction among consumers, e-commerce companies are increasingly challenged to optimize inventory and fulfill orders efficiently. This has led to a significant uptick in demand for warehouse space. By 2024, global retail e-commerce sales were projected to surpass USD 6.3 trillion, with further growth anticipated in the subsequent years.

- The need for efficient inventory management is one of the primary drivers of demand for warehousing in the e-commerce era. E-commerce businesses must maintain large and diverse inventories to cater to customer demands. Warehouses are the central hubs for storing, organizing, and processing these inventories, ensuring timely order fulfillment.

- The growth of direct-to-consumer (D2C) brands has also contributed to the surge in warehousing demand. D2C brands bypassing traditional retail channels and selling directly to customers require dedicated warehousing space to store their products and fulfill orders efficiently.

North America is Set to Lead in Market Share

- The North American market for outsourced fulfillment services is witnessing robust growth, propelled by the surge in e-commerce and direct-to-consumer (DTC) business models. With e-commerce sales in North America on a steady rise, the demand for streamlined fulfillment solutions is escalating.

- US online sales hit approximately USD 1.119 trillion in 2023, up from USD 1.040 trillion in 2022, marking a growth rate of 7.6%. In comparison, total retail sales in the United States climbed to about USD 5.088 trillion in 2023 from roughly USD 4.904 trillion in 2022, reflecting a growth rate of about 3.8%.

- Factoring in all retail and food-service sales, US e-commerce made up 15.6% of the total sales in Q4 2023, as reported by the Commerce Department. The unadjusted figures revealed that US e-commerce sales represented 17.1% of the total sales. The Commerce Department's estimates suggested that the total US e-commerce sales for the year surpassed USD 1.118 trillion.

- There is a noticeable trend toward larger warehouses in the United States driven by evolving consumer behaviors and technological advancements. Businesses - from e-commerce giants to third-party logistics firms - are significantly expanding their warehouse footprints. Understanding these dynamics and aligning strategies with market demands is becoming increasingly crucial for businesses.

- With businesses increasingly adopting advanced technologies like automation, the landscape of fulfillment processes is evolving. The shift toward larger warehouses underscores the necessity for modern supply chain management to be agile and efficient, reflecting changes in how goods are stored, transported, and fulfilled.

Direct To Customer Outsourced Fulfillment Industry Overview

The direct-to-customer (D2C) outsourced fulfillment market boasts a diverse and fiercely competitive landscape, featuring key players like FedEx Fulfillment, Red Stag Fulfillment, PFS Commerce, FBA (Fulfillment by Amazon), and DCL Logistics. These industry leaders have leveraged mergers, acquisitions, partnerships, and expansions to bolster their market presence and broaden their service portfolios.

Amazon stands out as a market behemoth, credited to its robust logistics and vast customer base. On the other hand, Walmart Fulfillment has been strategically enhancing its offerings through key partnerships in the e-commerce and omnichannel realm.

In January 2024, FedEx Corp. unveiled 'fdx,' a pioneering data-centric commerce platform. This innovative tool seamlessly links every step of the customer's journey, empowering businesses to boost demand, enhance conversion rates, fine-tune fulfillment, and simplify returns. Notably, FedEx stands out as the sole logistics firm providing comprehensive e-commerce solutions, catering to businesses of all scales, all within a unified platform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption

- 1.2 Market Definition

- 1.3 Scope of the Study

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Government Initiatives

- 4.4 Value Chain and Supply Chain Analysis

- 4.5 Insights on Returns Processing

- 4.6 Spotlight on Outsourced Fulfillment Prices

- 4.7 Impact on COVID-19 and Other Geopolitical Events on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The rapid expansion of e-commerce globally driving the market

- 5.1.2 Increasing technological advancements in warehousing automation and inventory management

- 5.2 Market Restraints/Challenges

- 5.2.1 Operational complexity hindering the market

- 5.2.2 Regulatory compliances affecting the market

- 5.3 Market Opportunities

- 5.3.1 Expansions into New Markets driving the market

- 5.3.2 Sustainability Initiatives driving the market

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes Products and Services

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Warehousing and Storage

- 6.1.2 Distribution

- 6.1.3 Value-Added Services

- 6.2 By Application

- 6.2.1 Fashion and Apparel

- 6.2.2 Consumer Electronics

- 6.2.3 Home Appliances

- 6.2.4 Furniture

- 6.2.5 Beauty and Personal Care Products

- 6.2.6 Other Applications (Toys, Food Products, Etc.)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Singapore

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Middle East and Africa

- 6.3.4.1 Saudi Arabia

- 6.3.4.2 United Arab Emirates

- 6.3.4.3 Oman

- 6.3.4.4 Egypt

- 6.3.4.5 South Africa

- 6.3.4.6 Rest of Middle East and Africa

- 6.3.5 South America

- 6.3.5.1 Brazil

- 6.3.5.2 Mexico

- 6.3.5.3 Rest of South America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Company profiles

- 7.2.1 FedEx Fulfillment

- 7.2.2 Red Stag Fulfillment

- 7.2.3 PFS Commerce

- 7.2.4 FBA (Fulfillment by Amazon)

- 7.2.5 DCL Logistics

- 7.2.6 Sekel Tech

- 7.2.7 WareIQ

- 7.2.8 Ship Network (Formerly Rakuten Super Logistics)

- 7.2.9 DHL Fulfillment

- 7.2.10 ShipMonk

- 7.2.11 Whiplash (A Part of Ryder System Inc.)*

- 7.3 Other companies

8 FUTURE OF THE MARKET

9 APPENDIX

- 9.1 Macroeconomic Indicators

- 9.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 9.3 E-commerce and Consumer Spending-related Statistics

- 9.4 External Trade Statistics