Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636234

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636234

Global Power Factor Correction Units - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

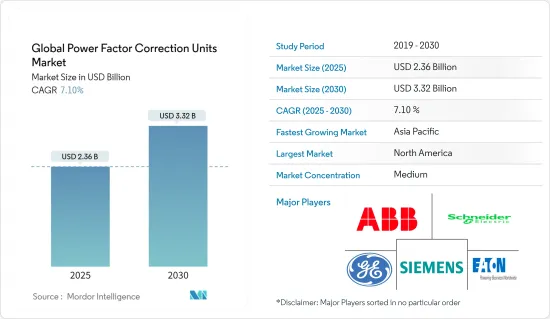

The Global Power Factor Correction Units Market size is estimated at USD 2.36 billion in 2025, and is expected to reach USD 3.32 billion by 2030, at a CAGR of 7.1% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rapid industrialization, growing stringent regulations, and standards over energy efficiency are expected to be among the most significant drivers for the global power factor correction units market during the forecast period.

- Complicated maintenance and technical challenges are associated with these units, posing a threat to the global power factor correction units market during the forecast period.

- However, continued efforts are being made toward smart grid deployments, which require efficient power management. This factor is expected to create several opportunities for the market in the future.

- Asia-Pacific is expected to witness significant growth and register the highest annual growth rate during the forecast period. This is due to the region's growing manufacturing industry and focus on wind energy installations.

Global Power Factor Correction Units Market Trends

The Industrial Segment to Witness Growth

- The global industrial landscape has experienced massive growth and expansion in recent years due to the confluence of factors such as technological advancements, increasing automation, and a growing emphasis on efficiency and productivity. This industrial growth has a positive impact on the compressed air pipe market, strengthening its demand and driving its growth trajectory.

- According to the data released by the United Nations Industrial Development Organization, the global manufacturing output has observed consistent growth since 2022 owing to the growing emphasis on increasing the manufacturing industry in developing economies like India, China, Malaysia, South Africa, and various others. This has led to an increase of 1.4% between the first and fourth quarters of 2023, signifying the growing manufacturing output globally.

- The industrial segment comprises energy-intensive industries such as steel manufacturing, petrochemicals, cement production, and pulp and paper mills. These industries operate large-scale equipment with significant reactive power demands, making them prime candidates for power factor improvement technologies.

- By installing power factor correction units, these facilities can substantially reduce their electricity bills, as many utility companies impose penalties for low power factors. Moreover, improved power factor leads to enhanced voltage stability and reduced stress on electrical infrastructure, potentially extending the lifespan of expensive industrial equipment and minimizing downtime due to electrical issues.

- The growing emphasis on innovation has ushered in a new era of automation and digitalization in the manufacturing industry. Automated systems and robotic technologies have become increasingly prevalent, enabling higher production rates and enhanced operational efficiency. This complexity often results in power factor degradation, prompting manufacturers to invest in comprehensive power quality solutions.

- For instance, in June 2023, ABB India secured a contract to provide electrification and automation systems for ArcelorMittal Nippon Steel India's advanced steel cold rolling mill (CRM) in Hazira, Gujarat. The project includes supplying the ABB Ability System 800xA distributed control system (DCS) and associated machinery and supplies.

- As industrial processes become increasingly digitized and automated under the paradigm of Industry 4.0, the demand for sophisticated power factor correction solutions has grown. Modern industrial facilities are integrating smart power factor correction units with real-time monitoring, adaptive correction, and seamless integration with broader energy management systems.

- Therefore, as mentioned above, the industrial segment is expected to grow significantly during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is a pivotal market in the global landscape for power factor correction units. It is characterized by rapid industrialization, burgeoning energy demands, and an increasing focus on energy efficiency. This vast and diverse region, encompassing various rapidly evolving economies, presents a favorable market scenario for the power factor correction industry.

- Industrialization is the primary driver for adopting power factor correction units across Asia-Pacific. The region's position as a global manufacturing powerhouse, spanning automotive, electronics, textiles, and heavy industries, necessitates sophisticated power management solutions. With these countries' rapidly rising industrial segment, the demand for power correction factor units is expected to increase significantly.

- For instance, in the financial year 2023, India's manufacturing exports hit a record high, reaching USD 447.46 billion, marking a 6.03% growth from the previous year's (FY22) USD 422 billion. The manufacturing industry, contributing to 17% of India's GDP and employing over 27.3 million workers, is pivotal in the nation's economy. With various initiatives and policies, the Indian government aims to elevate manufacturing's market share to 25% by 2025.

- With their substantial reactive power demands, these energy-intensive industries are increasingly turning to power factor correction technologies to optimize their electrical systems, reduce operational costs, and comply with stringent energy efficiency regulations. The push for industrial upgrades and the adoption of advanced manufacturing technologies further accentuate the need for reliable power factor correction solutions.

- Urbanization and infrastructure development across Asia-Pacific have significantly contributed to the growing demand for power factor correction units. Rapid city expansion and the establishment of industrial parks and special economic zones have placed unprecedented strain on existing power infrastructures. This has led to a heightened focus on power quality improvement and grid stability, with power factor correction playing a crucial role in mitigating transmission losses and enhancing overall electrical system efficiency.

- For instance, in October 2023, the Malaysian government unveiled plans to invest substantially in the establishment of four new industrial parks in Perak. A standout among these is the Automotive High-Tech Valley (AHTV) in Tanjung Malim, designed as a pivotal move to rejuvenate Malaysia's automotive industry. Forecasts suggest this venture will draw in a staggering USD 6.7 billion in investments over the coming decade. Not only will this initiative create thousands of job opportunities, but it also aims to position Malaysia as a leader in the regional production of state-of-the-art vehicles.

- Moreover, the concept of smart cities, gaining traction across the region, incorporates advanced power management systems, including intelligent power factor correction units, as integral components of urban electrical infrastructure.

- Therefore, as mentioned above, Asia-Pacific is expected to dominate the market during the forecast period.

Global Power Factor Correction Units Industry Overview

The global power factor correction units market is semi-fragmented. Some of the key players in this market (in no particular order) are ABB Ltd, Siemens AG, General Electric Company, Schneider Electric SE, and Eaton Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003502

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rapid Industrial Growth

- 4.5.1.2 Stringent Regulatory Standards

- 4.5.2 Restraints

- 4.5.2.1 Maintenance abd Technical Challenges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Active Power Factor Correction Unit

- 5.1.2 Passive Power Factor Correction Unit

- 5.1.3 Hybrid Power Factor Correction Unit

- 5.2 End Users

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.3 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 NORDIC

- 5.3.2.7 Russia

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 South Korea

- 5.3.3.6 Malaysia

- 5.3.3.7 Thailand

- 5.3.3.8 Indonesia

- 5.3.3.9 Vietnam

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 Nigeria

- 5.3.4.4 Egypt

- 5.3.4.5 Qatar

- 5.3.4.6 South Africa

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Schneider Electric SE

- 6.3.3 Eaton Corporation

- 6.3.4 Siemens AG

- 6.3.5 General Electric Company

- 6.3.6 Emerson Electric Co.

- 6.3.7 Mitsubishi Electric Corporation

- 6.3.8 Toshiba Electronic Devices & Storage Corporation

- 6.3.9 Crompton Greaves Limited

- 6.3.10 L&T Electrical & Automation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Smart Grid Development

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.