Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636218

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636218

Global Gear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

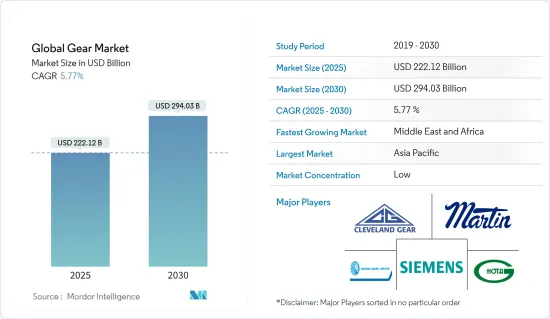

The Global Gear Market size is estimated at USD 222.12 billion in 2025, and is expected to reach USD 294.03 billion by 2030, at a CAGR of 5.77% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising industrial automation and the growing global wind energy installation are expected to be among the most significant drivers for the global gear market during the forecast period.

- High production costs for gears are expected to threaten the global gear market during the forecast period.

- However, continued efforts are being made to manufacture customized gears to effectively meet the client's demand. This factor is expected to create several opportunities for the market in the future.

- Asia-Pacific is expected to grow significantly and register the highest annual growth rate during the forecast period. This is due to the region's growing manufacturing industry and focus on wind energy installations.

Global Gear Market Trends

The Oilfield Equipment Segment to Witness Growth

- The oilfield equipment segment represents a significant portion of the global gear market, encompassing a wide range of applications across the entire oil and gas value chain. This segment utilizes gears in critical machinery such as drilling rigs, pumps, compressors, and other equipment essential for the exploration, extraction, processing, and transportation of oil and gas resources.

- The upstream segment, or the exploration and production (E&P) segment, is a significant consumer of gears in the oilfield equipment segment. Gears play a crucial role in various equipment such as drilling rigs, mud pumps, drawworks, and wellhead systems. The demand for gears in the upstream segment is primarily driven by global oil and gas prices, technological advancements in exploration techniques (e.g., seismic imaging and horizontal drilling), and the increasing focus on deepwater and ultra-deepwater exploration.

- Crude oil production has witnessed significant growth in recent years due to the rising demand for crude oil due to expanding economies in Asia-Pacific and Africa. Additionally, due to sanctions on Russia, oil production has increased to meet the rising demand.

- According to the Energy Institute Statistical Review of World Energy, crude oil production witnessed a significant growth of 2% between 2022 and 2023. Similarly, the average annual growth rate over the past decade has been more than 1.1%, indicating an increasing growth in crude oil. This growth drives the demand for equipment, which fuels the demand for gear in the industry.

- The midstream segment includes pipelines, trucking fleets, tanker ships, and storage facilities. Gears are essential in pumps, compressors, and other equipment used in this segment, particularly in pipeline operations and LNG processing plants. The primary driving factors for gear demand in the midstream segment include the expansion of pipeline infrastructure, increasing global trade of liquefied natural gas (LNG), and the need for more efficient transportation and storage solutions.

- For instance, in June 2024, India's State-owned Oil and Natural Gas Corporation (ONGC) and Indian Oil Corporation (IOC) inked a deal to establish a compact liquefied natural gas (LNG) facility adjacent to the Hatta gas field in Madhya Pradesh. The plant, leveraging advanced technology, is poised to churn out LNG, heralded as a greener substitute to conventional fossil fuels. This increased demand for LNG will drive growth in the gears market, as specialized gears are essential for operating and maintaining LNG plants. This development is expected to stimulate innovation and investment in gear manufacturing technologies.

- The downstream segment is another critical end user of gears in the oilfield equipment market. Gears are used in various equipment within refineries and processing plants, such as pumps, compressors, mixers, and conveyor systems. The driving factors for gear demand in the downstream segment include the increasing global demand for refined petroleum products, the need for more efficient and environmentally friendly refining processes, and the growth of the petrochemical industry.

- Therefore, as per the above points, the oil and gas equipment end-user industry is expected to grow during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is a pivotal segment in the global gear market. With a burgeoning population and robustly growing economies, nations such as India, China, South Korea, and those in the ASEAN region are actively strengthening their industrial and manufacturing industries. This concerted effort creates a favorable market environment for the gears market.

- The automotive industry is one of the primary end users of gears in Asia-Pacific, with countries like Japan, South Korea, China, and India being major automotive manufacturing hubs. The segment's demand for gears spans a wide range, from transmission systems and differentials to steering mechanisms and engine components.

- According to the International Organization of Motor Vehicle Manufacturers, automobile manufacturing in Asia-Pacific significantly rose between 2022 and 2023. In 2023, the region manufactured 5,51,15,837 automobiles, resuming a 10% growth rate. The annual average growth rate between 2019 and 2023 was over 12%, signifying the rising demand for gears in the region.

- Similarly, the industrial segment is experiencing significant growth in the area, and the demand for gears is increasing with the expanding industrial segment. Gears are crucial in various applications, such as machine tools, material handling equipment, and heavy machinery used in construction and mining. The rapid industrialization across Asia-Pacific, particularly in countries like China, India, and Southeast Asia, has driven substantial demand for industrial gear.

- For instance, in the financial year 2023, India's manufacturing exports hit a record high, reaching USD 447.46 billion, marking a 6.03% growth from the previous year's (FY22) USD 422 billion. The manufacturing industry, contributing to 17% of India's GDP and employing over 27.3 million workers, is pivotal in the nation's economy. With various initiatives and policies, the Indian government aims to elevate manufacturing's market share to 25% by 2025.

- Additionally, the aerospace and defense industry represents another significant end user of gears in Asia-Pacific. Countries such as Japan, South Korea, China, and India are expanding their aerospace manufacturing capabilities. This expansion drives the demand for high-precision gears in aircraft engines, landing gear systems, and various control mechanisms.

- Therefore, as mentioned above, Asia-Pacific is expected to dominate the market during the forecast period.

Global Gear Industry Overview

The global gear market is fragmented. Some key players in this market (in no particular order) are Cleveland Gear Co., Siemens AG, Martin Sprocket & Gear Inc., Hota Industrial Mfg. Co. Ltd, and Bharat Gears Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003481

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Focus on Industrial Automation

- 4.5.1.2 Growing Wind Energy Installation

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Gear Type

- 5.1.1 Spur Gear

- 5.1.2 Helical Gear

- 5.1.3 Planetary Gear

- 5.1.4 Rack and Pinion Gear

- 5.1.5 Worm Gear

- 5.1.6 Bevel Gear

- 5.1.7 Other Gear Types

- 5.2 End-user Industry

- 5.2.1 Oilfield Equipment

- 5.2.2 Mining Equipment

- 5.2.3 Industrial Machinery

- 5.2.4 Power Plants

- 5.2.5 Construction Machinery

- 5.2.6 Other End-user Industries

- 5.3 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 NORDIC

- 5.3.2.7 Russia

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 South Korea

- 5.3.3.6 Malaysia

- 5.3.3.7 Thailand

- 5.3.3.8 Indonesia

- 5.3.3.9 Vietnam

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 Nigeria

- 5.3.4.4 Egypt

- 5.3.4.5 Qatar

- 5.3.4.6 South Africa

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Cleveland Gear Co.

- 6.3.2 Siemens AG

- 6.3.3 Martin Sprocket & Gear Inc.

- 6.3.4 Hota Industrial Mfg. Co. Ltd

- 6.3.5 OKUBO GEAR Co. Ltd

- 6.3.6 Bharat Gears Ltd

- 6.3.7 Elecon Engineering Company Limited

- 6.3.8 Precipart

- 6.3.9 Kohara Gear Industry Co. Ltd

- 6.3.10 Aero Gear Inc.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Customization Offerings

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.