PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636191

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636191

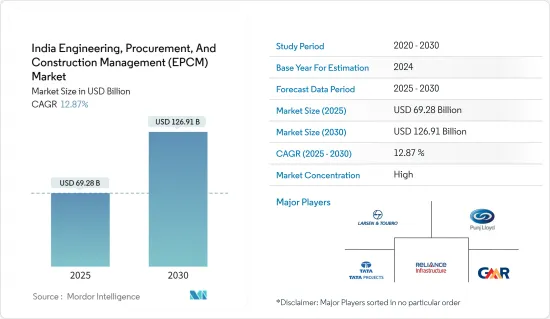

India Engineering, Procurement, And Construction Management (EPCM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The India Engineering, Procurement, And Construction Management Market size is estimated at USD 69.28 billion in 2025, and is expected to reach USD 126.91 billion by 2030, at a CAGR of 12.87% during the forecast period (2025-2030).

Key Highlights

- India's engineering, procurement, and construction (EPC) market is pivotal in the nation's infrastructure landscape. This market presents a spectrum of trends, challenges, and opportunities spanning diverse industries. India's EPC market has grown robustly and is fueled by ambitious infrastructure blueprints and industrial advancements. Bolstered by governmental impetus and private investments, the market's compound annual growth rate (CAGR) is poised to maintain its vigor in the coming years. Noteworthy investments are channeled into the Bharatmala project for road construction, the modernization of the railway network, and initiatives like the Smart Cities Mission. In addition, there is a notable surge in renewable energy projects, spanning solar, wind, and other avenues.

- The nation is also witnessing the development and expansion of thermal, hydroelectric, and nuclear power plants alongside a bolstered power transmission network. Key initiatives such as the Smart Cities Mission, AMRUT, and Bharatmala underscore India's commitment to infrastructure growth. Furthermore, the nation's rapid industrialization and urbanization fuel an escalating demand for enhanced infrastructure. Lastly, the liberalization of FDI policies is drawing in international EPC players, who are also embracing cutting-edge construction technologies and project management tools.

India Engineering, Procurement, And Construction Management (EPCM) Market Trends

Infrastructure Development Driving Demand For EPC Services

The Indian government has embarked on ambitious infrastructure programs, notably the Smart Cities Mission, Bharatmala Pariyojana for highways, and the Sagarmala Project for ports. The Smart Cities Mission aims to elevate cities by enhancing core infrastructure, ensuring a high quality of life, fostering a clean and sustainable environment, and implementing 'Smart' Solutions. Emphasizing sustainable and inclusive growth, the mission focuses on compact areas, aiming to create a replicable model to guide other cities. This initiative is not just about transforming individual cities but about catalyzing a nationwide movement toward smarter urban centers.

These initiatives underscore India's commitment to infrastructure development, presenting significant opportunities for EPCM services. With urbanization surging, there is a critical need for upgraded urban infrastructure, from metro rail systems to airports and smart city projects. In tandem, the "Make in India" campaign, aimed at bolstering manufacturing, is spurring the construction of new plants and industrial facilities, further driving the demand for EPCM services.

The global launch of the "Make in India" initiative marked India's renewed focus on manufacturing. The primary goal of this initiative is to position India as the top choice for global manufacturing. Since its inception, the Indian government has spearheaded numerous reforms to bolster manufacturing, design, innovation, and startups. Amidst a globally subdued economic landscape, India has emerged as the fastest-growing economy, boasting a growth rate of 7.5% that continues to accelerate. Initiatives like "Make in India," "Digital India," "100 Smart Cities," and "Skill India" have played a pivotal role in driving this growth.

"Make in India" specifically targets integrating India into the global supply chain, emphasizing the need for Indian companies to excel on a global stage. India has significantly liberalized its economy, opening sectors like defense, railways, construction, insurance, pension funds, and medical devices to foreign direct investment (FDI). This move has positioned India as one of the most open economies worldwide. To further enhance the business environment, the Indian government has prioritized improving the ease of doing business. The focus is on simplifying regulations to foster a conducive environment for businesses. Leveraging technology, the government has integrated 14 services into the eBiz portal, streamlining clearances from various government agencies. The impact of "Make in India" is already evident.

Overall, India is witnessing tangible outcomes from its "Make in India" initiative, with economic indicators on the rise, foreign investments increasing, and the manufacturing sector expanding. The concerted efforts of the Smart Cities Mission, Bharatmala Pariyojana, Sagarmala Project, and Make in India are reshaping India's infrastructure. This ambitious agenda bolsters urban and industrial capabilities and opens up significant avenues for engineering, procurement, and construction management services. With India's deepening integration into global supply chains and ongoing efforts to improve its business environment, the nation is on track to emerge as a pivotal manufacturing and infrastructure hub, setting the stage for sustained economic growth and development.

India's Energy And Utilities Segment Experiencing Surge in Demand, Driven by Increased Investments and Initiatives

India still grapples with an unreliable power grid, leaving a significant portion of its populace unconnected and facing daily power outages. The country's power sector stands out globally for its diverse energy sources. India harnesses traditional avenues like coal, natural gas, oil, and nuclear power alongside newer options such as wind, solar, hydropower, municipal waste, and biomass. Driven by a commitment to transition to clean energy, the Indian government is spearheading a substantial industry overhaul. This includes revamping infrastructure and channeling investments into green energy, notably wind and solar power.

Recognizing the pivotal role of private investment, the Indian government has rolled out several incentive schemes to bolster the sector. Setting ambitious targets, India aims to slash carbon emissions by 45% by the end of the decade, source 50% of its electricity from renewables by 2030, and ultimately achieve carbon neutrality by 2070. These targets and India's robust and consistent economic growth present lucrative prospects for energy companies.

India's vision for 2030 includes a 500 GW clean energy capacity, with a significant 280 GW from solar power. As of February 2023, India's total generation capacity stood at 412.21 GW, with approximately 100 GW attributed to clean sources. Notably, India boasts the second-highest wind power capacity in Asia, trailing only China. It also holds the title of the world's fifth-fastest-growing solar energy market and the most cost-efficient producer of solar power.

On the global stage, India ranks fourth in renewable energy generation. The government has earmarked a substantial USD 42 billion over the next five years to foster innovation and scale up the energy sector. India's commitment to enhancing its energy landscape is underscored by its impressive score of 89.4 in the World Bank's 2019 Ease of Doing Business - Getting Electricity survey. This score evaluates the ease of connecting to the grid, supply reliability, tariff transparency, and electricity pricing. For context, Denmark secured a slightly higher score of 90.2.

Looking ahead, India has laid out ambitious plans for offshore wind energy, aiming to establish 5 GW of projects by 2022 and a substantial 30 GW by 2030. The "Grid Connected Solar Rooftop Program" is set on achieving a 40 GW capacity for rooftop solar (RTS) projects by 2022. The key focus is on research, development, and demonstration (RD&D) to bolster the adoption of new and renewable energy. The Ministry of New and Renewable Energy (MNRE) actively promotes R&D to advance energy technologies, materials, and local production capabilities.

Overall, India's power sector is undergoing a significant transformation, a diverse energy mix, and a notable focus on clean energy. This shift is spurring substantial infrastructure enhancements and drawing in considerable investments. With clear targets to slash carbon emissions, ramp up renewable energy capacity, and ultimately achieve carbon neutrality, India emerges as an attractive prospect for energy firms. The government's proactive steps bolstered this appeal, such as generous funding and supportive policies, which nurture innovation and foster sectoral growth. As India fortifies its energy landscape and embraces more renewables, the country is on track to cement its position as a global frontrunner in sustainable energy. This promises a more dependable power supply for its citizens and underscores India's commitment to worldwide environmental objectives.

India Engineering, Procurement, And Construction Management (EPCM) Industry Overview

The Indian engineering, procurement, and construction management (EPCM) market features a fragmented landscape, hosting numerous players. Although dominant players exist, the market is fragmented, with many small to mid-sized companies actively participating, especially in specialized sectors or regional markets. Prominent entities in this sector include Larsen & Toubro (L&T), Tata Projects Limited, Punj Lloyd Group, Reliance Infrastructure Limited, and GMR Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renewable Energy Projects

- 4.2.2 Government Initiatives

- 4.3 Market Restraints

- 4.3.1 Regulatory and Bureaucratic Hurdles

- 4.3.2 Increase in Cost of Construction Material

- 4.4 Market Opportunities

- 4.4.1 Adoption of Smart Infrastructure Technologies

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

- 4.8 Insights into Technology Innovation in the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Engineering

- 5.1.2 Procurement

- 5.1.3 Construction

- 5.1.4 Other Services

- 5.2 By Sectors

- 5.2.1 Residential Industrial, Infrastructure (Transportation), and Energy and Utilities

- 5.2.2 Industrial

- 5.2.3 Infrastructure (Transportation)

- 5.2.4 Energy and Utilities

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 Larsen & Toubro (L&T)

- 6.2.2 Tata Projects Limited

- 6.2.3 Punj Lloyd Group

- 6.2.4 Reliance Infrastructure Limited

- 6.2.5 GMR Group

- 6.2.6 Afcons Infrastructure Limited

- 6.2.7 Hindustan Construction Company (HCC)

- 6.2.8 NCC Limited (Nagarjuna Construction Company)

- 6.2.9 IVRCL Limited

- 6.2.10 KEC International

- 6.2.11 Gammon India Limited

- 6.2.12 Simplex Infrastructures Limited

- 6.2.13 Rays Power Infra Limited

- 6.2.14 Megha Engineering & Infrastructures Ltd

- 6.2.15 Salasar Techno Engineering Ltd (STEL)

7 FUTURE TRENDS