Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636181

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636181

Global Lead-Acid Battery Separator For SLI Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

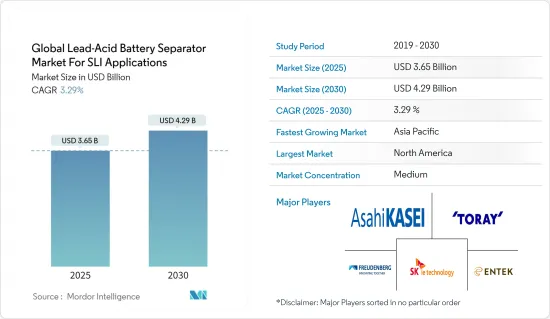

The Global Lead-Acid Battery Separator Market For SLI Applications Industry is expected to grow from USD 3.65 billion in 2025 to USD 4.29 billion by 2030, at a CAGR of 3.29% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in the automation sector and the cost-effectiveness of lead-acid batteries are expected to be among the most significant drivers for the global lead-acid battery separator market for SLI applications during the forecast period.

- On the other hand, complex supply chain constraints for manufacturing battery separators threaten the market studied during the forecast period.

- Nevertheless, continued efforts are being made to develop enhanced battery separator materials. This factor is expected to create several opportunities for SLI applications in the global lead-acid battery separator market in the future.

- Asia-Pacific is expected to witness significant growth and will likely register the highest CAGR during the forecast period. This is due to the region's considerable battery and associated equipment and materials manufacturing industry.

Global Lead-Acid Battery Separator Market Trends

Polypropylene Segment to Witness Significant Growth

- Polypropylene has become essential in the global lead-acid battery separator market, especially for Starting, Lighting, and Ignition (SLI) applications in recent years. This versatile thermoplastic polymer offers optimal properties, including excellent chemical resistance, high mechanical strength, and good electrical insulation.

- Polypropylene's versatility allows for incorporating various additives and surface treatments, enhancing its performance characteristics and extending battery life. This adaptability has made it an attractive option for battery manufacturers looking to improve their products' efficiency and durability. As the automotive industry faces increasing pressure to produce more efficient and environmentally friendly vehicles, the demand for high-performance SLI batteries has grown, further solidifying polypropylene's position in the separator market.

- As global automobile manufacturing escalates, the demand for batteries in SLI applications is set to surge, consequently boosting the need for polypropylene in battery separator materials. This increase is driven by the growing production of electric and hybrid vehicles requiring efficient and durable battery components. Additionally, advancements in battery technology are further propelling the demand for high-quality polypropylene separators.

- According to the International Organization of Motor Vehicle Manufacturers, global automobile manufacturing has surpassed the pre-pandemic level. It is expected to continue on a similar growth trend in the coming years. For instance, between 2019 and 2023, the annual production capacity increased by more than 2%, whereas the growth rate between 2022 and 2023 was over 10%, signifying the growing production of automobiles.

- Ongoing research and development efforts are focused on improving polypropylene separator technology. Areas of exploration include developing nanocomposite materials and advanced surface modifications to enhance polypropylene separators' already impressive capabilities. These innovations aim to improve battery performance, longevity, and safety, meeting the evolving needs of the automotive industry and other sectors reliant on lead-acid battery technology.

- For instance, in February 2024, Scientists at Incheon National University pioneered a method to enhance battery separators' stability and properties. Their approach involves applying a layer of silicon dioxide and other specialized molecules. The findings, detailed in a publication in Energy Storage Materials, showcase the effective graft polymerization on a polypropylene (PP) separator, introducing a consistent layer of silicon dioxide (SiO2).

- Therefore, as per the above points, the polypropylene separator material segment is expected to grow during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific region has emerged as a dominant force in the global lead-acid battery separator market, particularly in the polypropylene segment for SLI applications. This growth is primarily driven by the region's booming automotive industry, rapid industrialization, and increasing energy storage needs.

- According to the International Organization of Motor Vehicle Manufacturers, automobile manufacturing in Asia-Pacific significantly rose between 2022 and 2023. In 2023, the region manufactured 55,115,837 automobiles, resuming a 10% growth rate. The annual average growth rate between 2019 and 2023 was over 12%, signifying the rising demand for gears in the region.

- China, Japan, South Korea, and India are at the forefront of this market expansion. Their robust manufacturing sectors and growing domestic vehicle demand contribute significantly to the uptake of polypropylene battery separators.

- China, in particular, plays a crucial role in shaping the regional market dynamics. As the world's largest automobile market and a significant producer of lead-acid batteries, China's demand for high-quality polypropylene separators has surged in recent years. The country's push toward electric vehicles and hybrid technologies has paradoxically bolstered the SLI battery market, as these vehicles still require traditional lead-acid batteries for their 12V systems.

- Japan and South Korea, known for their technological prowess, have driven innovations in polypropylene separator manufacturing. Companies in these countries have focused on developing separator materials with enhanced performance characteristics, such as improved puncture resistance and reduced electrical resistance. These advancements have served their domestic markets and positioned them as key exporters of high-quality separators to other countries in the region and beyond.

- For instance, in January 2024, Incheon National University scientists in South Korea pioneered a technique to enhance separator stability and characteristics. By incorporating a layer of silicon dioxide and other specialized molecules, batteries utilizing these separators showcased enhanced performance and curbed the growth of intrusive root-like structures. This breakthrough sets the stage for developing high-safety batteries, which are crucial for the widespread acceptance of electric vehicles and cutting-edge energy storage solutions.

- Therefore, as mentioned above, the Asia-Pacific region is expected to dominate the market during the forecast period.

Global Lead-Acid Battery Separator Industry Overview

The global lead-acid battery separator market for SLI applications is semi-fragmented. Some key players in this market (in no particular order) are Asahi Kasei Corporation, Toray Battery Separator Film Co. Ltd, Freudenberg Performance Materials, SK ie Technology Corporation Ltd, and Entek International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002590

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Automotive Industry

- 4.5.1.2 Cost Effectiveness

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Constraints

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Others

- 5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 NORDIC

- 5.2.2.7 Russia

- 5.2.2.8 Turkey

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Australia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Vietnam

- 5.2.3.10 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 United Arab Emirates

- 5.2.4.3 Nigeria

- 5.2.4.4 Egypt

- 5.2.4.5 Qatar

- 5.2.4.6 South Africa

- 5.2.4.7 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Asahi Kasei Corporation

- 6.3.2 Toray Battery Separator Film Co. Ltd

- 6.3.3 Freudenberg Performance Materials

- 6.3.4 SK ie Technology Corporation Ltd

- 6.3.5 Entek International

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 Ube Maxell Co. Ltd

- 6.3.8 W-Scope Corporation

- 6.3.9 Daramic

- 6.3.10 Amer SIL

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Enhanced Separator Materials

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.