PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1632058

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1632058

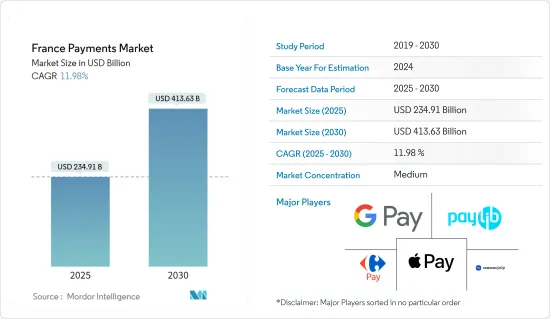

France Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The France Payments Market size is estimated at USD 234.91 billion in 2025, and is expected to reach USD 413.63 billion by 2030, at a CAGR of 11.98% during the forecast period (2025-2030).

Key Highlights

- E-commerce has been a significant factor driving the French payments market. The increasing popularity of online shopping has led to a surge in digital transactions, prompting a shift from traditional card payments to alternative methods. E-wallets and digital payment platforms have gained traction as consumers seek convenient and secure ways to make online purchases. Furthermore, the emergence of buy now, pay later (BNPL) services has added flexibility to payment options, particularly among younger demographics.

- Consumers shopping online increased significantly in Europe. According to a survey, mobile transactions contributed 50% of the total online sales in Europe. Digital wallets are the most preferred payment option, and nearly 44% of Europeans would rather pay using e-wallet apps. Merchants also favor digital wallets as they follow the Payment Services Directive rule (PSD2) that guarantees safe payments. Also, these are quick to set up and cost-effective.

- The payment industry in France is constantly evolving. As part of its National Retail Payments Strategy (2019-2024), Banque de France has devised several initiatives that commercial banks and payment service providers are implementing to minimize reliance on cash and move the country closer to a cashless society.

- The Bank de France has developed several initiatives that commercial banks and payment service providers are implementing as part of its National Retail Payments Plan (2019-2024) to reduce dependency on cash and bring the nation closer to a cashless society. These schemes will accelerate the growth of digital payments in the country.

- Carrefour launched a WhatsApp feature for customers to order through the platform. The consumers could place orders on Carrefour Father Christmas bot on WhatsApp, and for payment and delivery slots, they were directed to the company website for final checkout. This strategy allowed the company to manage orders from social media platforms outside the e-commerce website.

- Further, COVID-19 triggered a massive increase in online purchasing, and the current levels were maintained. This surge in online payments increased the demand for contactless or digital payments. According to a survey, 83% of consumers worried about touching a credit card payment reader and took to pay apps for making payments.

France Payment Market Trends

E-Commerce is Observing Significant Growth

- E-commerce in France was estimated at over 50 million in 2022. In France, 85% of online purchases are paid using debit cards tied to their bank account. The quick rise in consumer preference for digital payments, the sharp rise in cross-border transactions, and the introduction of the EU Digital Identity Wallet are the critical drivers for the increasing demand for e-commerce in Europe.

- Worldline introduced passengers Express Transit for Apple Pay to enable travelers to tap their iPhone or Apple Watch on the transit readers and go. So passengers boarding the bus or train will become fast, have fewer problems securing cash, credit cards, or tickets, and enjoy greater security because they don't have to open their wallets or phones to tap on the system.

- Merchants are trying to attract customers by offering lucrative promotional offers for digital payment methods. Alipay+ rolled out various promotions and deals with local merchants in France, including retail store Printemps, to reward shoppers. The Printemps Haussmann store in France also gave e-wallet customers a special 5% off-store-wide discount and a free bubble tea ticket.

- Worldline collaborated with Alipay to enhance its payment offering for in-store and E-Commerce merchants across Europe. The fully integrated POS and e-Commerce solution from Worldline can be upgraded to enable Alipay+ acceptance with simple software upgrades at no additional cost. Businesses may profit from many industries, including retail, F&B, and hospitality.

Retail Sector is a key Factor for Market Growth

- France is the 2nd largest e-commerce market in Europe, with 41.8 million French people making purchases on the internet. There was a decline of 2.90 % annually in January 2023 in retail sales in France. The rising inflation has impacted the retail industry due to increased prices for fuel and energy because of the Russia-Ukraine war. To face this challenge, French Govt. made a deal with major retailers to cap many food prices.

- The European Govt. passed two laws, the Digital Markets Act (DMA) and the Digital Services Act (DSA), which will support the growth of digitization in the retail markets. Some retailers have already adopted the digitalization of point of sale for faster processing of orders.

- France is an essential hub for investment in Europe. At least four foreign investment projects target France every day. Lower corporate taxes and fewer employment tribunal cases have allowed companies to invest in the country.

- Everli and Carrefour signed an agreement for business expansion across ten cities in France. In several cities, the platform of Everli will make the supermarkets and hypermarkets of Carrefour accessible. Customers in these cities can order up to 25,000 items from more than 140 nearby retailers, and orders will be delivered the same day.

France Payment Industry Overview

The France Payments market is semi-consolidated, and start-ups are trying to disrupt the Payments industry using attractive promotions and building user-friendly payment gateways. However, the market is dominated by global players such as Apple Pay, Samsung Pay, Google Pay, Carrefour Pay, PayLib, and more. These businesses' primary growth tactics to survive the fierce competition include product releases, substantial investment in research and development, collaborations, and acquisitions.

In November 2023, FrenchSys, a division of CB-Investissements (CBI), and JCB International announced a partnership to streamline the JCB certification process for payment terminals throughout France. With an integrated certification procedure managed by FrenchSys, this partnership assists banks, terminal manufacturers, and merchant partners in accepting JCB Cards. By enabling merchant partners to allow JCB's over 154 million card members to use their cards in-store, the partnership accelerates the implementation of payment terminals and gives them a competitive advantage.

In April 2023, Worldline and Credit Agricole, a French lender, partnered to establish a joint payments operation. According to the payments company, France is an attractive and strategic Worldline market. According to the release, the alliance combines Credit Agricole's robust distribution networks through its bank system with Worldline's in-store and online capabilities for retailers. According to the statement, the planned joint venture will leverage Worldline's global acceptance and acquiring platform to deliver a full-service offering to the major accounts in France, including the local Cartes Bancaires scheme.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in the country

- 4.5 Key market trends pertaining to the growth of cashless transaction in the country

- 4.6 Impact of COVID-19 on the payments market in the country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Proliferation of E-commerce, including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power

- 5.1.2 Bank Transfers is a Popular Payment Method for High Ticket Items

- 5.1.3 SMBs are Using Different Payment Methods to Stabilize Sales

- 5.2 Market Challenges

- 5.2.1 Cyber Security Challenges

- 5.3 Market Opportunities

- 5.3.1 Move towards Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of key demographic trends and patterns related to payments industry in the country (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

- 5.7 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in the country

- 5.8 Analysis of cash displacement and rise of contactless payment modes in the country

6 Market Segmentation

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Others (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Apple Pay

- 7.1.2 PayLib

- 7.1.3 Samsung Pay

- 7.1.4 Carrefour Pay

- 7.1.5 Google Pay

- 7.1.6 Lydia

- 7.1.7 Lyf pay

- 7.1.8 Pumpkin

- 7.1.9 Mastercard

- 7.1.10 Visa

8 Investment Analysis

9 Future Outlook of the Market