PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1630370

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1630370

Europe Data Center Interconnect - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

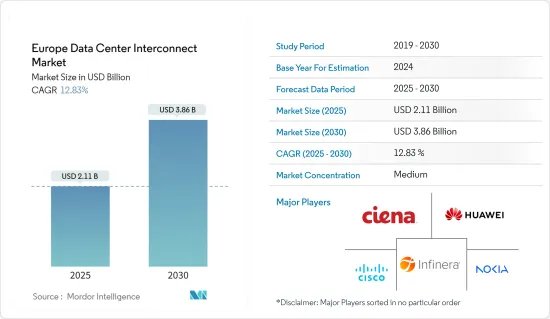

The Europe Data Center Interconnect Market size is estimated at USD 2.11 billion in 2025, and is expected to reach USD 3.86 billion by 2030, at a CAGR of 12.83% during the forecast period (2025-2030).

With the proliferation of data and expansion of technologies like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Factors such as throughput, latency, simplified operations, maintenance, intelligence, and security are becoming significant priorities for data center vendors. This is one of the major factors driving the adoption of data center interconnect (DCI) technology, owing to its ability to boost inter-data center bandwidth, reduce latency, and eliminate packet loss.

Key Highlights

- Government agencies offer tax breaks and other benefits to attract the maximum number of investors to construct a hyperscale data center market in Western Europe & the Nordics. Due to vast resources of renewable energy, low power prices, favorable climate conditions, good infrastructure, and a skilled workforce, Nordic countries are well suited for data centers and, therefore, for DCI and have resulted in a surge of foreign investments over the years.

- The market studied is expanding due to the growing cloud computing industry and the recent increase in OTT service use due to a nationwide shutdown. Furthermore, introducing 5G services may broaden the scope of interconnected data center solutions. Autonomous cars, smart cities, digital twins, virtual reality, AI virtual assistants, video surveillance and monitoring, and gaming are fueling market demand.

- Cloud computing is one sector estimated to be a significant driver of the data center interconnect market. Cloud computing has been increasing over the past few years, owing to lower operational expenses faced by enterprises. Combining colocation with the cloud can reduce latency, increase security, and create cloud interconnection opportunities. Cloud provider companies require high bandwidth and resiliency private networks and support from a robust data center provider.

- The major challenge, especially for small and medium-sized businesses, is the cost of data center connectivity services. A new data center necessitates a significant investment in both construction and maintenance. Furthermore, the distance between data centers is important since it might reduce a data center's efficiency, limiting the growth of the data center interconnect industry.

- The fast growth of online activity has raised the demand for data center interconnection, particularly in recent years, as the COVID-19 pandemic made access to internet applications a requirement. With more people relying on the Internet for work, social networking, e-commerce, banking, and entertainment, the demand for almost limitless uptime and interconnection is growing.

Europe Data Center Interconnect Market Trends

Ongoing Trend Toward Cloud Migration is Expected to Drive the Market

- The growing demand from domestic and international enterprises and cloud computing customers has pushed companies to expand data center facilities. Public cloud services dominate the data center market in Europe. The use of private cloud services by government agencies is growing as they plan to make greater use of cloud services in public administration during the forecast period. However, hybrid cloud services have more substantial growth potential than private and public cloud services. The growth in cloud technology is, in turn, a growing market for data center interconnect technology in the region.

- Moreover, the growing adoption of cloud computing (which further escalated due to the COVID-19 pandemic), increasing penetration of foreign cloud vendors across Europe, governmental rules and regulations for local data security, and the increasing investments by domestic European players are some of the major factors that are driving the demand for interconnected data centers in the region.

- Furthermore, Microsoft Corporation has invested in multiple data center locations in Norway, while Google LLC has expanded its operations in Finland. It is not just the cloud enterprise players; enterprises and interconnection providers are also increasingly investing in the Nordics. This is expected to boost the growth of the data center interconnect market in the region over the forecast period.

- In July 2022, the US communications infrastructure provider Zayo announced that it had launched the Zeus subsea route that connects the United Kingdom and continental Europe as cloud service providers seek faster internet connections. Currently, undersea cables transmit nearly all the world's internet data traffic, and many technology companies, including Alphabet's Google and Meta, have also invested in building their subsea cables.

- The demand for data centers is growing with the popularity of cloud solutions and industry applications, such as AI, 5G, and edge computing. In return, it is anticipated to give immense opportunities to the data center interconnect market. According to Cloudscene, as of February 2024, there are 522 data centers located in Germany, the most in any European nation. Data centers are buildings that house computer systems and centralize organizations' shared information technology (IT) operations.

Germany to Hold a Significant Market Share

- The growing number of data centers, increasing investment in cloud technologies, and expanding end-user markets are major factors driving the German data centers' investment in the interconnect market. The stringent regional laws, like GDPR and Personal Data Protection Initiatives (Gaia-X), further boost the region's local data center construction and development.

- With the development of edge computing solutions, there has been an increase in the demand for high-capacity networks. The German economy has increased the need for edge computing solutions due to disruptive technologies like autonomous vehicles, cloud computing, IoT, and advanced robotics. Higher bandwidths and better processing speeds are now necessary due to the expanding use of these technologies.

- Low latency is crucial to overcoming these obstacles, raising the demand for colocation in data centers. Cloud service providers can offer high bandwidth and low latency by colocating their network design close to the users. The development of 5G has allowed interconnection service providers to deliver these services with better connections across remote German locations, fueling the market's expansion.

- The development of 5G and immersive technologies like augmented reality, virtual reality, and AI has also increased the demand for more bandwidth to be set aside for data sharing across businesses. The bandwidth capacity of Europe's interconnections is growing quickly, and this trend is expected to continue. The telecommunications industry has the most significant market share because of the rising need for high-speed connectivity to improve client experiences. In addition, the region's interconnection service providers benefit from expanding demand for enhanced connectivity and decreased data transfer latency due to the rapid uptake of smart devices.

- Over the past few years, data center workloads have increased due to the development of 5G networks and other disruptive technologies like AI and the Internet of Things. Along with managing high workloads, the rising use of cloud computing and As-a-Service models within businesses has boosted the demand for specialized skill sets. According to Ericsson, the number of mobile 5G subscriptions in Central and Eastern Europe is expected to reach 229.40 million by 2028. Germany, being one of the most developed countries in Central Europe, is expected to witness a significant growth in the number of mobile 5G subscriptions.

Europe Data Center Interconnect Industry Overview

The European data center interconnect market is semi-consolidated with the presence of major players like Huawei Technologies, Ciena Corporation, Cisco Systems Inc., Infinera Corporation, and Nokia Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- In 2023, Germany was Europe's second-largest colocation market. Over the past five years, the growth of the data center market in Germany has been driven by the digital transformation strategies adopted by enterprises, the introduction of cloud computing, the Internet of Things (IoT), AI, and the implementation of the GDPR. About 80% of the organizations in Germany use cloud services for one or more services, which has increased and is projected to register a CAGR of 3-5% over the next 3-5 years. Given the high growth rate of service data as well as the high cost of the network operation, German data center service provider aixit announced that it has decided to create connectivity for non-blocking the data flow and seamless expansion across the data centers in the next decade. aixit announced that it would build its own DCI network with Huawei's DC OptiX.

- In October 2022, Nokia announced an expanded partnership with NL-ix, Europe's largest distributed internet exchange provider. Nokia would supply its advanced 7750 SR-s platforms powered by its ground-breaking routing silicon, FP5. With this deployment, NL-ix can provide 400GE and 800GE access and interconnection services to its national research and education network (NREN) and cloud provider clients.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Ongoing Trend Toward Cloud Migration

- 5.1.1 Recent Changes in Network Consumption Coupled with Anticipated Adoption of 5G to Drive Market Growth

- 5.2 Market Challenges

- 5.2.1 Capacity and Installation Related Challenges

6 MARKET SEGMENTATION

- 6.1 By Country

- 6.1.1 Germany

- 6.1.2 United Kingdom

- 6.1.3 France

- 6.1.4 Ireland

- 6.1.5 Spain

- 6.1.6 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Huawei Technologies

- 7.1.2 Ciena Corporation

- 7.1.3 Cisco Systems Inc.

- 7.1.4 Infinera Corporation

- 7.1.5 Nokia Corporation

- 7.1.6 ZTE Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS