PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1630163

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1630163

Healthcare Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

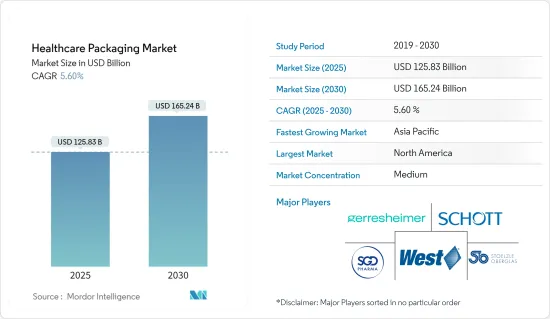

The Healthcare Packaging Market size is estimated at USD 125.83 billion in 2025, and is expected to reach USD 165.24 billion by 2030, at a CAGR of 5.6% during the forecast period (2025-2030).

Key Highlights

- Healthcare packaging includes materials specifically designed to transfer and store healthcare equipment and pharmaceutical drugs safely. These materials are chosen based on the product characteristics to safeguard, identify, and preserve the integrity of the enclosed items. The packaging process protects drugs from external threats like contamination, physical damage, and environmental factors, which could jeopardize their efficacy and safety.

- An increase in surgeries globally is significantly boosting the demand for medical device packaging. With elective and non-elective procedures on the rise, there is a heightened need for premium packaging solutions to ensure the sterility and safety of surgical instruments.

- Furthermore, the surge in cosmetic surgical procedures in the United States is amplifying the demand for medical device packaging. As more individuals seek cosmetic enhancements, the requirement for specialized packaging solutions for these devices intensifies. According to a June 2024 article by the American Society of Plastic Surgeons, plastic surgeries saw a 5% uptick, while minimally invasive procedures rose by 7% in 2023 compared to the prior year. In total, 1.6 million cosmetic surgical procedures and nearly 25.4 million cosmetic minimally invasive procedures were conducted in 2023.

- Heightened emphasis on infection control, driven by the uptick in surgeries, appliances, and instruments, has spurred demand for sterilized packaging in healthcare settings. Such packaging is vital in warding off contaminants that could lead to infections, a concern magnified in surgical settings due to the risk of surgical site infections (SSIs). This pressing need for dependable sterilization has catalyzed the evolution and adoption of advanced packaging materials and technologies, ensuring superior protection and sustained sterility throughout a device's lifecycle.

- In February 2024, Amcor Group GmbH, based in Oshkosh, Wisconsin, and recognized as one of the world's leading sterile barrier medical packaging facilities, unveiled plans for a major investment in new thermoforming equipment. This strategic decision directly addresses the rising demand in North America. The newly added thermoforming equipment, designated for the facility's Class 7 cleanroom, is anticipated to commence operations by December 2024.

- Additionally, in September 2023, Sudpack, a German packaging solutions provider, announced plans to enhance production at its Coulmer facility in France under its medical technology division, Sudpack Medica. This expansion will double the cleanroom production area to meet ISO 7 standards, reinforcing Sudpack's presence in the pharmaceutical arena. The Coulmer plant is broadening its portfolio to include header bags. These bags, designed for high-volume medical technology products undergoing ethylene oxide sterilization, cater to diverse medical requirements, ranging from syringe nests to surgical sets.

Healthcare Packaging Market Trends

Blister Packs are Expected to Witness Significant Growth

- Blister packs are one of the popular and convenient dosage formats. Companies operating in the healthcare packaging industry are economical alternatives to those offered in traditional markets where healthcare and pharmaceutical companies meet sustainability goals and shelf life requirements. Blister packs are used in medical devices and instruments such as catheters and subcutaneous syringes. However, blister packs are less useful in packaging medical devices than in pharmaceutical packaging.

- The occurrence of new diseases focused on population health management, the emergence of informed customers, and the growth of OTC (over-the-counter) drugs have augmented the growth of blister packaging in the pharmaceutical industry. Also, blister packaging has gained popularity to protect medication from moisture. In response to these trends, companies like Burgopak and Ecobliss have developed innovative blister packaging that is child-proof.

- Market vendors are making significant first-mover initiatives catering to material use. For instance, in June 2024, Keystone Folding Box, a specialist in paperboard packaging, introduced the Push-Pak, a paperboard blister wallet designed for medicine tablets. This innovative solution features a straightforward push-through opening system, eliminating the necessity for complex opening instructions. Additionally, its compact blister arrangement minimizes the overall size of the package.

- Moreover, in February 2024, Boots, the pharmacy chain, announced that it would broaden its recycling initiative for medicine and vitamin blister packs across its outlets. Due to their complex nature, blister packs cannot be recycled through local authority curbside collections, leading to their common disposal in landfills or incineration.

- In 2023, the Consumer Healthcare Products Association (CHPA) reported that OTC sales in the United States surpassed USD 43 billion, marking a substantial rise from approximately USD 28 billion in 2011. Leading the charge in sales, categories such as vitamins, cold/allergy sinus tablets, and internal analgesics dominated the US OTC market. This surge in OTC medicine sales has, in turn, spurred a heightened demand for blister packs.

North America is Expected to Dominate the Market

- In North America, the United States and Canada are countries with booming economies, aging population segments, well-developed healthcare delivery systems, gross domestic product (GDP) levels, and health insurance. However, the United States is one of the largest geographic markets for healthcare packaged products due to its advanced primary care community, extensive healthcare and life sciences research activities, high healthcare cost concentration, and large pharmaceuticals.

- Moreover, the rise in chronic diseases among the aging population further drives the need for effective medical device packaging. Devices for managing chronic conditions, such as insulin pumps, must be securely packaged to ensure their functionality and reliability. As the prevalence of chronic diseases rises, packaging innovations are expected to focus on enhancing device protection, ease of use, and patient safety, addressing the unique needs of an aging population.

- The medical technology sector stands out as a beacon of success in manufacturing in the United States, blending swift innovation with precise product development and global distribution. Offerings span advanced tools like nanotechnology and advanced imaging to everyday essentials like bandages and thermometers. The sector leads the world and boasts robust domestic R&D, manufacturing hubs in communities of all sizes, and a significant export footprint for American products.

- According to the Advanced Medical Technology Association, the United States is one of the largest medical device markets across the world, accounting for more than 40% of its total value. Industry leaders are driving growth through strategies like innovating products, expanding into new markets, and forming strategic alliances, consequently driving the demand for medical device packaging.

- Canada is witnessing a robust surge in ophthalmic interventions. According to the Conference Board of Canada, not only is the frequency of these interventions on the rise, but the number of individuals undergoing at least one ophthalmic procedure is set to double in the upcoming decades.

- Since ophthalmic packaging is vital for safeguarding the safety, sterility, and effectiveness of eye-related products, ranging from eye drops and ointments to surgical instruments, the surge in the number of interventions would escalate the demand for medical device packaging.

- As per the UN Comtrade Trade Map, in 2023, the United States emerged as the top global exporter of health equipment, with exports valued at approximately USD 36.6 billion. Germany secured the second position, exporting health equipment worth about USD 19 billion. Given the United States' significant export capabilities in health equipment, there is an increased demand for robust healthcare packaging.

Healthcare Packaging Industry Overview

The healthcare packaging market is moderately fragmented. A small number of significant players dominate the market in terms of market share, which include Gerresheimer AG, Corning Incorporated, Nipro Corporation, West Pharmaceutical Services, and SGD SA. These major players dominate the market and concentrate on growing their clientele across numerous nations. These businesses use tactical joint ventures to raise their market share and profitability.

- August 2024: Oliver Healthcare Packaging joined hands with the Healthcare Plastics Recycling Council in August 2024. In 2023, Oliver Healthcare Packaging announced the construction of a 122,000 sq. ft manufacturing facility in Johor, Malaysia. As Oliver's largest manufacturing site in the region, it positions the company to tap into the swiftly expanding Asia-Pacific healthcare packaging market. Malaysia is a pivotal hub for numerous pharmaceutical and medical device companies across Southeast Asia.

- October 2023: Stoelzle Pharma, a manufacturer of premium glass packaging, unveiled its latest offering: the PharmaCos Line. Tailored specifically for wellness and healthcare products, the PharmaCos Line features an extensive selection of glass jars. These jars, designed with a screw neck, come in amber color and span sizes from 5 ml to 500 ml. Furthermore, the lineup showcases flat shoulder bottles, available in amber and flint glass, with capacities ranging from 20 ml to 150 ml.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Demand for Diagnostic Substances and Self Care Medical Devices Creates Uptick in Medical Device Packaging Products

- 5.1.2 Rise in Medicine Counterfeiting Leading to Advanced Packaging and Labeling

- 5.2 Market Challenges

- 5.2.1 Raw Material Price Fluctuation Influences the Market's Growth

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Glass

- 6.1.2 Plastic

- 6.1.3 Other Materials (Paper and Metal)

- 6.2 By Product Type

- 6.2.1 Bottles and Containers

- 6.2.2 Vials and Ampoules

- 6.2.3 Cartridges and Prefilled Syringes

- 6.2.4 Pouches and Bags

- 6.2.5 Blister Packs

- 6.2.6 Tubes

- 6.2.7 Paper Board Boxes

- 6.2.8 Caps and Closures

- 6.2.9 Labels

- 6.2.10 Other Product Types

- 6.3 By End-use Vertical

- 6.3.1 Pharmaceutical

- 6.3.2 Medical Devices

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Spain

- 6.4.2.4 Italy

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Mexico

- 6.4.4.2 Brazil

- 6.4.5 Middle East and Africa

- 6.4.5.1 South Africa

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 United Arab Emirates

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Gerresheimer AG

- 7.1.2 Corning Incorporated

- 7.1.3 Nipro Corporation

- 7.1.4 SGD SA

- 7.1.5 Stolze-Oberglas GmbH

- 7.1.6 Bormioli Pharma SRL

- 7.1.7 Schott AG

- 7.1.8 Shandong Medicinal Glass Co. Ltd

- 7.1.9 Beatson Clark PLC

- 7.1.10 Arab Pharmaceutical Glass Co

- 7.1.11 Piramal Glass Pvt Ltd

- 7.1.12 Sisecam Group

- 7.1.13 Oliver Healthcare Packaging

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging vs. Established Players

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK