PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1628708

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1628708

Japan Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

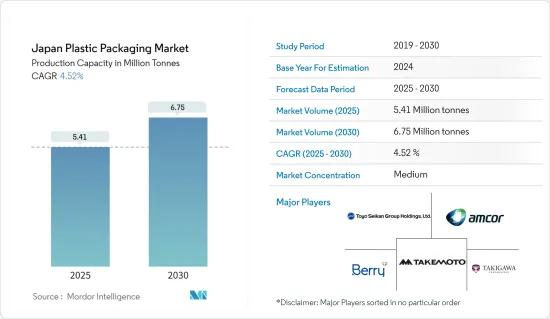

The Japan Plastic Packaging Market size in terms of production capacity is expected to grow from 5.41 million tonnes in 2025 to 6.75 million tonnes by 2030, at a CAGR of 4.52% during the forecast period (2025-2030).

The food and beverage industry drives the plastic packaging market in Japan. Consumers favor plastic packaging for its lightweight and unbreakable nature, enhancing ease of handling.

Key Highlights

- In Japan, consumers favor plastic packaging for its durability, flexibility, and cost-effectiveness. This packaging form employs plastic films, containers, and other polymer-based materials, creating a barrier against external elements. This versatility makes it a lightweight solution for packaging various goods. Industries such as beverage, food, cosmetics, and pharmaceuticals increasingly rely on plastic container packaging, which drives the product demand.

- Japanese manufacturers of plastic packaging are poised for substantial growth by focusing on the development of both rigid and flexible packaging solutions tailored to diverse end-use industries. In October 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., has successfully created a recycled BOPP film primed for mass production. Starting October 2024, these companies will commence the distribution of samples for this innovative film.

- New filling technologies and the advent of heat-resistant PET bottles have broadened market possibilities in the country. In response to rising demand, beverage manufacturers are ramping up PET bottle production in Japan.

- In September 2024, Coca-Cola Bottlers Japan Inc. (CCBJI) unveiled a new aseptic production line at its Tokai Plant in Aichi Prefecture. This line boasts a production capacity of around 600 small PET bottles per minute, bolstering CCBJI's ability to meet surging demand.

- However, a surge in plastic waste has led Japanese consumers to gravitate towards eco-friendlier packaging materials such as glass and metal. The region has seen a notable uptick in the adoption of aluminum and glass, celebrated for their recyclability and eco-friendly attributes. This shift away from plastic could pose challenges for product demand in the future.

Japan Plastic Packaging Market Trends

Bottles and Jars Segment is Expected to Dominate the Market

- The lightweight nature of plastics fuels their rising demand. In Japan, the food and beverage sector's increasing reliance on plastic bottles and jars propels the need for plastic packaging.

- Plastic bottles extend their utility beyond beverages, finding prominence in Japan's cosmetics and pharmaceuticals sectors. Market dynamics are evolving with innovations like advanced filling technologies and the launch of heat-resistant PET bottles. While PET bottles lead in various sectors, polyethylene (PE) bottles are the preferred choice for beverages, cosmetics, sanitary items, and household items such as detergents.

- Japanese companies are increasingly producing PET bottles for beverages, a trend poised to fuel market growth. In March 2024, Otsuka Foods Co., Ltd., a prominent player based in Japan, unveiled its plans to launch two new products in its MATCH line of carbonated vitamin drinks: MATCH Pineapple Soda in a 500-ml PET bottle and MATCH Jelly in a 260-gram PET bottle in the Japanese market.

- The Japan Soft Drink Association has set an ambitious goal of achieving 50% bottle-to-bottle recycling by 2030. Industry players are lightening the weight of PET bottles to reduce the amount of PET resin used. Data from the Japan Soft Drink Association (JSDA) highlights that PET bottles have overtaken steel and glass in the country's non-alcoholic beverage sector. Furthermore, stringent government regulations have positioned Japan as a global leader in PET bottle collection and recycling, a factor poised to stimulate market growth.

- As reported by the Ministry of Economy, Trade and Industry (METI) Japan, the country's plastic packaging production saw a dip of 0.1 million tons (-9.01 percent) in 2023 compared to the prior year. However, projections indicate a rebound to 1.09 million tons in 2024, signaling potential market growth.

Beverage Industry Set for Significant Growth

- Japan's beverage industry is expanding significantly, fueled by a rising demand for health-oriented drinks. Consumers are increasingly gravitating towards beverages that promise health benefits, including immunity enhancement, better digestion, and sharper cognitive functions. This trend is especially evident among the elderly and those facing health challenges linked to their lifestyles.

- In Japan, rigid plastic packaging, commonly found in plastic bottles and containers, is widely favored for food and beverage applications. The demand for these products is notably driven by the use of HDPE and PET bottles for packaging juices, carbonated soft drinks, and other beverages. Notably, manufacturers such as Toyo Seikan Co. Ltd. are producing heat and pressure-resistant PET bottles tailored specifically for beverage applications.

- Innovations are reshaping Japan's beverage landscape, with a focus on merging natural ingredients and scientific advancements. In 2024, segments such as soft drinks, sports drinks, and energy drinks are poised to showcase the varied consumer preferences for functional beverages. By prioritizing innovation, targeted marketing, and sustainability, companies can cement their foothold in Japan's burgeoning functional beverage arena.

- Additionally, data from the US Department of Agriculture (USDA) reveals that Japan's non-alcoholic beverage market was valued at approximately USD 40 billion in 2023, with imports accounting for about USD 1 billion. The U.S. stands as Japan's chief supplier of non-alcoholic drinks, with exports predominantly comprising mineral water and juices. Healthy beverages and non-alcoholic beers are emerging as leading consumer trends, significantly influencing the demand for plastic packaging.

- Japan's surging appetite for non-alcoholic drinks is bolstering its plastic packaging sector. As reported by Asahi Group Holdings, a prominent Japanese firm, Ready-to-Drink (RTD) tea led the soft drinks segment in 2023, capturing roughly 30% of sales. The diverse range of non-alcoholic beverages in Japan is driving a heightened demand for both rigid and flexible packaging solutions in the nation.

Japan Plastic Packaging Industry Overview

The Japanese plastic packaging market is moderately consolidated with the presence of global and domestic players such as Amcor Group, Takemoto Yohki Co. Ltd, Toyo Seikan Group Holdings Ltd, Berry Global Inc. and Takigawa Corporation. These companies are actively pursuing strategies such as product innovations, collaborations, mergers and acquisitions, and investments to expand their business and capture a larger market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand of Plastic Packaging Solutions for Multiple End-User Industries in Japan

- 5.1.2 Rising Popularity of Plastic Bottles for Beverage Industry in Japan

- 5.2 Market Challenges

- 5.2.1 Increasing Environmental Concerns Regarding Plastic Packaging Recycling in Japan

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGEMENTATION

- 7.1 By Packaging Type

- 7.1.1 Flexible Plastic Packaging

- 7.1.2 Rigid Plastic Packaging

- 7.2 By Product Type

- 7.2.1 Bottles and Jars

- 7.2.2 Trays and containers

- 7.2.3 Pouches

- 7.2.4 Bags

- 7.2.5 Films and Wraps

- 7.2.6 Other Product Types

- 7.3 By End-User Vertical

- 7.3.1 Food

- 7.3.2 Beverage

- 7.3.3 Healthcare

- 7.3.4 Personal Care and Household

- 7.3.5 Other End-Users

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Amcor Group

- 8.1.2 Takemoto Yohki Co. Ltd.

- 8.1.3 Berry Global

- 8.1.4 Takigawa Corporation

- 8.1.5 Toyo Seiken Group Holdings Ltd.

- 8.1.6 Sonoco Products Company

- 8.1.7 Sealed Air Corporation

- 8.1.8 Hosokawa Yoko Co. ltd.

- 8.1.9 Toppan Inc.

- 8.1.10 Kodama Plastics Co. Ltd.

- 8.2 Heat Map Analysis

- 8.3 Competitor Analysis - Emerging vs. Established Players

9 INVESTMENT ANLAYSIS

10 FUTURE OF THE MARKET