PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1626337

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1626337

North America Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

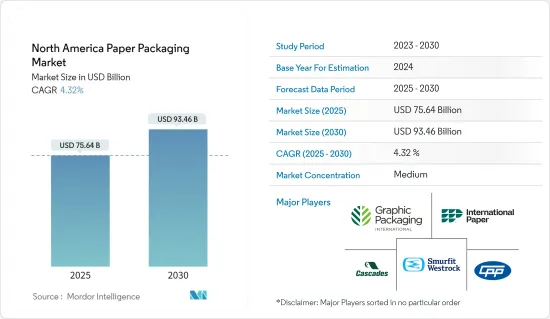

The North America Paper Packaging Market size is estimated at USD 75.64 billion in 2025, and is expected to reach USD 93.46 billion by 2030, at a CAGR of 4.32% during the forecast period (2025-2030).

Key Highlights

- Paper packaging stands out as a leading choice among eco-friendly packaging solutions. Its versatility allows it to be produced in various sizes while maintaining a compact footprint, making it an ideal fit for nearly every end-user industry, especially when compared to bulkier alternatives.

- According to the US Census Bureau, in 2024, pulp mills are expected to generate a revenue of USD 6.11 billion. Also, paperboard mills are expected to generate a revenue of USD 34.02 billion, and paper mills are expected to generate a revenue of USD 39.55 billion in the same year. With e-commerce evolving as an increasingly critical element of retail, paper packaging stands to benefit substantially.

- Moreover, the region emerges as one of the largest markets for corrugated packaging as the area has several foodservices and packaged food companies, including ready-to-eat, convenience, and ready-to-make meals. The high demand for out-of-home food due to busy work-life schedules and convenience is also a key factor driving the market growth. According to the International Franchise Association, the number of quick-service restaurants (QSRs) in the United States is estimated to reach 199,808 units by the end of 2024.

- Consumers are increasingly aware of the environmental risks associated with packaging, leading them to favor more eco-friendly purchasing choices. This shift is further amplified by pressures from consumers, the government, and the media on manufacturers to adopt greener practices in their products, packaging, and processes. Notably, consumers are willing to pay a premium for eco-friendly packaging. As a result of these trends, the paper packaging market is poised for growth.

- However, deforestation poses significant challenges to the paper packaging industry, including supply chain risks, environmental concerns, regulatory pressures, and the need for sustainable innovation. Addressing deforestation requires collaboration among stakeholders, including governments, companies, consumers, and environmental organizations, to promote responsible forest management and sustainable sourcing practices in the paper packaging industry.

North America Paper Packaging Market Trends

Environmental Concerns Creating Demand for Paper Packaging

- Over the decades, due to numerous government initiatives and increasingly stringent regulations, there has been growing awareness regarding the environmental hazards related to the disposal and recycling of packaging materials. The American Forest and Paper Association reported that the recycling rate for paper and paperboard in the United States reached approximately 68% in 2022.

- Notably, cardboard, often referred to as corrugated in the industry, stands out as the top recycled packaging material in the United States. In fact, around 34 million tons of cardboard were recovered for recycling. Moreover, about 50% of the material used nationwide for producing new boxes is sourced from recycled paper.

- In recent years, there has been a significant push for more ecological packaging of common things, particularly food and beverages. This has mostly taken the form of campaigns to drastically restrict the use of single-use plastics, a subject that has gathered massive public support in the previous five years.

- Consumers are using their purchasing power more readily to force major foodservice brands to change, choosing brands with sustainable commitments and even being willing to pay more for sustainable choices. Major foodservice brands are moving away from plastics and toward alternatives like recyclable fiber and paper packaging. North American governments are enacting plastic-free regulations, which is causing merchants and consumer brands to reconsider their supply chains and packaging options.

- The most evident trends in the packaging industry revolve around a circular economy. Currently, the packaging industry is dominated by paperboards that are 100% recyclable, which caters to environmental safety and standards to eliminate pollution. The liquid packaging market is expected to grow at a higher rate owing to the surge in demand for various beverages, such as organic drinks, fruit juices, tender coconut water, energy drinks, and non-dairy drinks (almond and soy milk).

The Expanding E-commerce and Pharmaceutical Industries Creating Demand for Various Paper Packaging Types

- As more consumers shift toward online shopping, there is a corresponding increase in the need for packaging materials to deliver these products to customers safely. Corrugated and folding carton packaging are among the primary materials used for packaging goods in the e-commerce industry due to their versatility, durability, and cost-effectiveness.

- The increasing demand for e-commerce is driving the growth of the North American paper packaging market by necessitating packaging materials suitable for online retail, customizable, sustainable, and optimized for efficient logistics and fulfillment operations. According to the US Census Bureau, in the second quarter of 2024, retail e-commerce sales in the United States amounted to roughly USD 291.6 billion, marking an increase compared to the previous quarter.

- With higher demand for prescription drugs, there will be a corresponding increase in the requirement for secondary and tertiary packaging solutions to store, transport, and display these medications safely. This increased demand for packaging materials is expected to benefit companies in the North American paper packaging market, as they play a crucial role in providing packaging solutions for the pharmaceutical industry.

- According to the Canadian Institute for Health Information (CIHI), in 2023, the total expenditure on non-prescription drugs in Canada amounted to CAD 6.7 billion (USD 4.9 billion), while spending on prescription drugs increased to CAD 41.1 billion (USD 30.27 billion). According to the same source, in 2020, the expenditure on prescription drugs was recorded at CAD 35.3 billion (USD 26 billion).

North America Paper Packaging Industry Overview

The North American paper packaging market is competitive with several influential players. Some of these important players in terms of market share are currently leading the market. These influential players with significant market shares are focused on expanding their customer base abroad. Some of the key players in the market include International Paper, Smurfit Westrock, Graphic Packaging International, Cascades Inc., and Canadian Paper and Packaging Co. Ltd.

- March 2024: ProAmpac, a global leader in flexible packaging and material science, acquired UP Paper, a leading producer of recycled kraft paper. Established in 2016, UP Paper swiftly became a top North American producer of 100% unbleached recycled kraft paper, serving diverse packaging needs. Leveraging their expertise in fiber and film-based material science, ProAmpac and UP Paper are set to innovate and deliver eco-friendly flexible packaging solutions.

- February 2024: Graphic Packaging divested its bleached paperboard manufacturing facility in Augusta, United States, selling it to Clearwater Paper for USD 700 million. Clearwater Paper perceives this acquisition as a strategic move to bolster its presence in the paperboard manufacturing industry. With an Adjusted EBITDA valuation of approximately USD 100 million, the deal underscores Graphic Packaging's commitment to refining its portfolio.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Growth of E-commerce Creating Demand for Various Paper Packaging Types

- 5.1.2 Regulations on Plastic-based Packaging Products Contributes to Higher Demand

- 5.2 Market Restraints

- 5.2.1 Effects of Deforestation on Paper Packaging

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Folding Cartons

- 6.1.2 Corrugated Boxes

- 6.1.3 Other Product Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Personal Care and Household Care

- 6.2.5 E-commerce

- 6.2.6 Electrical Products

- 6.2.7 Other End-user Industries

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Paper Company

- 7.1.2 Smurfit Westrock

- 7.1.3 Cascades Inc.

- 7.1.4 Packaging Corporation of America

- 7.1.5 Graphic Packaging International Inc.

- 7.1.6 Mondi PLC

- 7.1.7 DS Smith PLC

- 7.1.8 Sealed Air Corporation

- 7.1.9 ProAmpac Holdings Inc.

- 7.1.10 Canadian Paper and Packaging Co. Ltd

- 7.1.11 Clearwater Paper Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET