PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550484

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550484

France Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

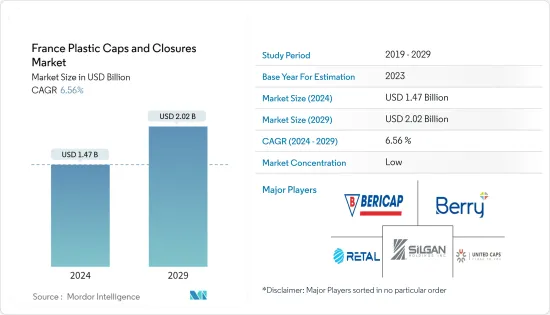

The France Plastic Caps And Closures Market size is estimated at USD 1.47 billion in 2024, and is expected to reach USD 2.02 billion by 2029, growing at a CAGR of 6.56% during the forecast period (2024-2029). In terms of production volume, the market is expected to grow from 37.77 billion units in 2024 to 57.35 billion units by 2029, at a CAGR of 8.71% during the forecast period (2024-2029).

In France, the plastic packaging market thrives on innovation and sustainability. Its solutions serve various industries and emphasize product integrity, convenience, and environmental consciousness.

Key Highlights

- France's packaging industry's growth is poised to be significantly shaped by evolving demographics and social dynamics. A robust employment rate and a sizable populace influence consumer spending and preferences. This, in turn, fuels the demand for innovative packaging solutions, including convenient formats, value-driven options, and compact single-serve variants. Key drivers of this demand encompass evolving consumer preferences, ranging from enhanced mobility and resealability to a growing appetite for premium offerings.

- Renowned for its innovation and luxury brands, France's cosmetics market appreciates a global reputation for superiority. This sector's emphasis on elegance, functionality, and sustainability fuels an ongoing demand for premium packaging solutions. Caps and closures might witness growth in the personal care and cosmetics industry.

- With its strong focus on exports, the cosmetics market in France is a crucial driver for the rising demand for plastic bottles. As per the French Federation for Beauty Companies (FEBEA), French perfumes and cosmetics exports have shown consistent growth despite notable market slowdowns in China and the United States. Following an 18.8% surge in 2022, these exports rose by 10.8% in 2023, surpassing the milestone of EUR 20 billion (USD 21.65 billion). Plastic bottles and jars, known for their design versatility, lightweight nature, and compatibility with diverse formulations, play a pivotal role in the caps and closures market.

- In September 2023, TotalEnergies, situated at its Grandpuits site southeast of Paris, unveiled plans for a new mechanical recycling unit dedicated to plastic waste. This initiative, set to commence operations in 2026, is a part of the company's broader commitment to bolster its low-carbon energy portfolio and advance the principles of a circular economy. The new recycling unit is projected to yield 30,000 tons annually, featuring high-value compounds with up to 50% recycled plastic content. Such plants would further push the country's market for plastic caps and closures.

- Plastic is one of the major pollutants that results in environmental degradation. Owing to this, the country has been implementing regulations to reduce plastic usage. The market is anticipated to be hampered by changes in dynamic regulatory standards, primarily due to rising environmental concerns. Packaging abides by strict regulations due to its broad range of applications in food, beverage, and other industries. The fundamental objective of these regulations is to ensure the safety and quality of packaged products and protect the environment.

France Plastic Caps and Closures Market Trends

Polyethylene Terephthalate (PET) is Expected to Witness Growth

- Lifestyle changes and consumer reliance on packaged beverages drive sales of PET bottle packaging products, including caps and closures. This trend drives the sale of products characterized by superior barrier properties and high-quality printability. Growing consumer demand for packaged drinking water provides durability, ease of use, and better protection of products from potential spoilage than other packaging alternatives.

- Moreover, the demand for sustainable and recyclable packaging materials is high. The European packaging industry announced its Circular Packaging Vision 2030, promising that by 2025, all packaging will be 100% recyclable, and PET plastic material products will contain 50% recycled content.

- The country is actively promoting the recycling of PET products, notably bottles. PET plastic bottles are gaining traction over traditional glass bottles, particularly for beverages like mineral water and non-alcoholic drinks. This shift is fueled by PET's reusability, facilitating more efficient transportation. PET's versatility is evident in its ability to be molded into various shapes, its inherent clarity, and its CO2 barrier.

- According to Eurostat, the revenue from the manufacture of plastic products in France in 2020 was valued at 30.65 billion and is expected to reach USD 36.36 billion in 2024. The increasing emphasis on mobility and convenience is a crucial factor shaping the demand for plastic products in the food and beverage packaging industries. This trend is particularly evident in the growing preference for on-the-go consumption and portion control.

- Further, in November 2023, Aloxe launched its latest venture, a recycled PET plastic manufacturing facility in Messein in the Meurthe-et-Moselle region. The Messein site has gradually increased operations, with two cutting-edge EREMA VACUNITE production lines situated on a repurposed brownfield. By December 2023, Aloxe plans to relocate its older lines from the Vezelise facility to Messein, effectively quadrupling its PET recycling capacity in France from 12.5 kt to 50 kt annually.

The Beverage Industry is Expected to Witness Robust Growth

- French consumers are pursuing healthier beverage choices, with a growing interest in non-alcoholic options. This shift is primarily motivated by a desire to moderate alcohol intake. Despite this trend, taste remains paramount for those opting for alcoholic beverages. On the flip side, the surge in non-alcoholic drink consumption is fueled by factors like brand awareness, product quality, cost, freshness, and claims of tradition.

- Bottled water consumption within the soft drinks segment is climbing, driven by its perceived health benefits. Energy drinks are also witnessing increased consumption. In energy drinks, promotional activities hold particular sway over French consumers.

- According to Eurostat, revenue from beverage manufacturing in 2020 was USD 24.06 billion and will reach USD 30.03 billion in 2023. The demand for beverages is pushing the country's market for PET bottles, caps, and closures. A growing public consciousness regarding the significance of clean drinking water further fuels this uptrend. Bottled water, known for its convenience, is a favored beverage.

- Significant companies in the country are actively pursuing innovative strategies to bolster their market presence. Take Nestle Waters France, for example, which made headlines by unveiling its latest eco-friendly initiative. The company declared that its VITTEL, HEPAR, and CONTREX brands' bottles, tailored for flavored and on-the-go ranges, are crafted entirely from 100% recycled plastic (rPET). Nestle Waters is swiftly transitioning its natural mineral water lines to embrace rPET bottles, marking a pivotal move in its overarching ambition to achieve carbon neutrality across its entire brand spectrum by 2025.

- Techniques, like utilizing recycled plastic for manufacturing plastic bottles, have been adopted by the government. These recycled plastic bottles are often more cost-effective than virgin plastic ones. This move aims to foster a circular economy and elevate the recycling rate. Such initiatives are poised to spur recycling giants like Veolia and Suez to scale nationwide PET bottle recycling efforts. Given the rising demand in France's FMCG sector, the plastic bottles market is projected to grow significantly in the coming years. Such efforts would further drive the country's demand for caps and closures.

France Plastic Caps and Closures Industry Overview

France's Plastic Caps and Closures market is fragmented, with many domestic and significant players, such as Berry Global, Inc., Bericap GmbH & Co. KG, Silgan Holdings Inc., United Caps, Retal Industries Ltd, and more. Companies operating in the region are focused on expanding their business through innovations, collaborations, acquisitions, mergers, etc.

- February 2024: Bericap and TotalEnergies collaborated to introduce a novel can cap crafted from recycled materials. The cap, designed for 20-liter lubricant containers, boasts a 50% post-consumer recycled plastic (PCR) composition and adheres to the stringent DIN 60 lubricant standards. These eco-conscious caps will be used for the TotalEnergies Lubrifiants' 20-liter premium lubricant cans produced in France and Belgium. This strategic move reiterates the commitment of these enterprises toward fostering a circular economy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Beverage Industry to Push the Market Demand

- 5.1.2 Demand for Recycled Plastics Such as rPET to Witness Growth

- 5.2 Market Restraints

- 5.2.1 Dynamic Nature of Regulatory Changes and Environmental Concerns

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGMENTATION

- 7.1 By Resin

- 7.1.1 Polyethylene (PE)

- 7.1.2 Polyethylene Terephthalate (PET)

- 7.1.3 Polypropylene (PP)

- 7.1.4 Other Plastic Materials (Polystyrene, PVC, Polycarbonate, etc.)

- 7.2 By Product Type

- 7.2.1 Threaded (Screw Caps, Vacuum, etc.)

- 7.2.2 Dispensing

- 7.2.3 Unthreaded (Overcaps, Lids, Aerosol-based Closures)

- 7.2.4 Child-resistant

- 7.3 By End-user Industry

- 7.3.1 Food

- 7.3.2 Beverage

- 7.3.2.1 Bottled Water

- 7.3.2.2 Carbonated Soft Drinks

- 7.3.2.3 Alcoholic Beverages

- 7.3.2.4 Juices & Energy Drinks

- 7.3.2.5 Other Beverages

- 7.3.3 Personal Care & Cosmetics

- 7.3.4 Household Chemicals

- 7.3.5 Other End-user Industries

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Retal Industries Ltd

- 8.1.2 Bericap Holding GmbH

- 8.1.3 Berry Global, Inc.

- 8.1.4 Silgan Holdings Inc.

- 8.1.5 United Caps

- 8.1.6 Tri-Sure Closures Australia Pty.Ltd (Grief Inc.)

- 8.1.7 Aptar Group

- 8.1.8 Jokey Group

- 8.1.9 Berlin Packaging

9 INVESTMENT ANALYSIS

10 MARKET FUTURE OUTLOOK