PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550337

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550337

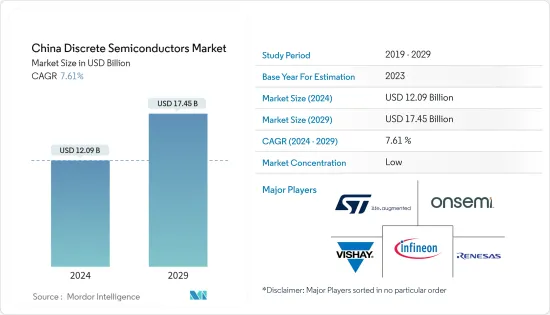

China Discrete Semiconductors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The China Discrete Semiconductors Market size is estimated at USD 12.09 billion in 2024, and is expected to reach USD 17.45 billion by 2029, growing at a CAGR of 7.61% during the forecast period (2024-2029).

Key Highlights

- The Chinese discrete semiconductor market is witnessing substantial growth, propelled by the country's expanding industrial landscape and a strategic pivot toward automation to boost ROI (return on investment). China boasts the largest manufacturing industry globally, contributing significantly to market demand. Manufacturing companies in China prioritize adopting 4.0 solutions to optimize operations, propelling market expansion.

- China has emerged as a prominent player in the global implementation of 5G technology. The MIIT projected that China would reach 592.01 million 5G users by February 2023, with expectations of surpassing 1 billion users by 2025. Significant efforts are underway to enhance the necessary infrastructure to support this advancement. For instance, as of October 2023, China had approximately 3.22 million 5G base stations, representing 28.1% of all cellular base stations. With 5G rapidly establishing itself as a crucial component of the communication sector, facilitating data transfer among various elements of the manufacturing ecosystem, these developments are poised to drive growth in the market within the country.

- Rising expenditures on developing data centers in the country may increase the demand for more electrical components, which is likely to boost the demand for discrete semiconductors in China during the forecast period. For instance, CloudScene highlighted China's significance in the Asia-Pacific data center landscape in September 2023. China boasted 448 data centers, the highest in the region. Globally, China secured the fourth spot in total data center count that month.

- Silicon carbide, gallium nitride, and other materials are used to manufacture discrete semiconductors. However, these raw materials are linked to high expenses, a significant market expansion obstacle. As a result, the elevated costs of raw materials necessary for producing discrete semiconductors are impeding the market's growth.

- Macroeconomic factors like China's economic growth directly affect industrial output and semiconductor demand. A slowdown may reduce investment and consumer spending, impacting semiconductor demand. International trade policies, tariffs, and sanctions impact the import and export of semiconductors and raw materials, affecting supply chain and market dynamics.

China Discrete Semiconductors Market Trends

Consumer Electronics is Expected to Witness a Significant Growth

- China's consumer electronics market is witnessing a surge, positioning the country as a significant player on the global stage. This growth is propelled by several factors: the expanding reach of e-commerce, a steady uptick in Chinese consumers' disposable incomes, ongoing product innovations, technological advancements, and, crucially, government backing. In addition, China's consumer electronics market is poised for continued expansion in the coming years, driven by rising demand for smart homes, augmented and virtual reality technologies advancements, and the rollout of 5G networks.

- China leads the global 5G market, with projections indicating that 5G will surpass 4G as the primary mobile technology in the country by 2024. GSMA forecasts that by 2025, China will boast the highest number of 5G connections globally, with an estimated 1 billion users. China unveiled the Layout Plan for the Construction of Digital China, a strategic roadmap aligning with its 'Digital China 2035' vision. This initiative aims to propel China into a significant global digital innovation player by 2035.

- Players in the market are launching discrete semiconductors for consumer electronics, further supporting the market growth. For instance, in February 2024, Vishay Intertechnology introduced a highly versatile 30 V n-channel Trench FETGen V power MOSFET. This MOSFET provides enhanced power density and high thermal efficiency, making it suitable for various applications across various sectors such as computer, consumer, and telecom. The compact 3.3 mm by 3.3 mm PowerPAK1212-F package houses the Vishay SiliconixSiSD5300DN, incorporating advanced source flip technology.

- The growth of governmental initiatives in strengthening the country's semiconductor ecosystem and the country's emergence as a global producer of consumer electronic sectors would support the market growth. China's household appliance industry has burgeoned into a multi-billion dollar sector. Data from the National Bureau of Statistics of China reveals that in April 2024, the retail sales value of household appliances and consumer electronics in China surpassed CNY 64 billion (USD 8.96 billion).

Power Transistors is Expected to Hold Significant Market Share

- An insulated gate bipolar transistor is a three-terminal semiconductor switching device that can be applied to many electronic devices for quick and efficient switching. These devices are typically used in amplifiers for switching/processing complex wave patterns with pulse width modulation (PWM). It comes in both Discrete and Modular varieties. Power semiconductors are being deployed quickly and widely, which has led to severe reliability concerns due to the scant field data and potential uncertainties. In this sense, the market for IGBTs is expanding significantly.

- The industrial sector is one of the major end-users of the IGBT power transistor. The rapidly advancing trend of Industry 4.0 in China with initiatives like "Made in China 2025" to enhance its manufacturing prowess and nurture high-tech sectors has created a stream of opportunities for market participants, which is one of the factors driving the need for IGBTs in motor drive applications. Many businesses continue replacing conventional motors with advanced motor drives to simplify operations and improve output.

- The automotive industry heavily relies on silicon MOSFET discrete semiconductors for various applications. MOSFETs are used in electronic control units (ECUs), battery management, motor control, and automotive lighting systems. Given their capacity to manage high currents, voltages, and durability, these components are the top choice for demanding automotive settings. MOSFET power transistors are crucial in efficiently functioning electric vehicles (EVs). They are employed in motor drive systems, DC-DC converters for auxiliary systems, etc. The robust growth of EVs is likely to drive the development of the studied market.

- As battery capacity rises, the energy savings from SiC MOSFETs also grow. Initially, these MOSFETs were exclusive to mid to high-end EVs with larger batteries. However, with the emergence of mainstream and budget vehicles like the Chevrolet Bolt EV, Volvo EX40, Kia Niro EV, and Nissan Leaf Plus EV, all boasting battery capacities exceeding 50kWh, SiC MOSFETs are poised to make inroads into China's mainstream passenger vehicle market, thus driving the market demand studied.

China Discrete Semiconductors Industry Overview

The Chinese discrete semiconductors market is fragmented, with the presence of major players like STMicroelectronics NV, On Semiconductor Corporation, Vishay Intertechnology Inc., Infineon Technologies AG, Renesas Electronics Corporation, and Texas Instrument Inc. Key players in the Chinese discrete semiconductors market are adopting strategies such as mergers, innovations, partnerships, investments, and acquisitions to enhance product offerings and gain sustainable competitive advantage.

- In January 2024, STMicroelectronics and Li Auto inked a strategic, long-term supply agreement centered around silicon carbide (SiC). Li Auto, a key figure in China's burgeoning new energy vehicle landscape, focuses on crafting, producing, and marketing upscale electric vehicles (EVs). In this collaboration, STMicroelectronics (ST) would provide Li Auto with SiCMOSFETs. These components are set to fortify Li Auto's endeavors in high-voltage battery electric vehicles (BEVs) spanning various market segments.

- In January 2024, Infineon Technologies partnered with Sinexcel Electric, an energy storage company. Infineon would supply Sinexcel with its latest 1,200 V CoolSiC MOSFET semiconductor devices in this collaboration. These will be complemented by Infineon's EiceDRIVER compact 1,200 V single-channel isolated gate drive ICs, which aim to enhance the efficiency of energy storage systems. The SiC power solution is pivotal in upcoming green energy production and storage applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Advancements in 5G Technology

- 5.1.2 Rising Demand for High-Energy and Power-Efficient Devices in the Automotive and Electronics Segment

- 5.1.3 Rising Demand for Electronic Components

- 5.2 Market Challenges

- 5.2.1 Rising Demand for Integrated Circuits

- 5.2.2 High Cost of Raw Materials

- 5.2.3 Increasing Design Complexity Due to Miniaturization

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistor

- 6.1.3 Power Transistor

- 6.1.3.1 MOSFET Power Transistor

- 6.1.3.2 IGBT Power Transistor

- 6.1.3.3 Other Power Transistors

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Communication

- 6.2.4 Industrial

- 6.2.5 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.2 On Semiconductor Corporation

- 7.1.3 Vishay Intertechnology Inc.

- 7.1.4 Infineon Technologies AG

- 7.1.5 Renesas Electronics Corporation

- 7.1.6 Texas Instrument Inc.

- 7.1.7 Qorvo Inc.

- 7.1.8 Microchip Technology Inc.

- 7.1.9 Diodes Incorporated

- 7.1.10 Wolfspeed Inc.

- 7.1.11 Rohm Co., Ltd.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET