PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550334

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550334

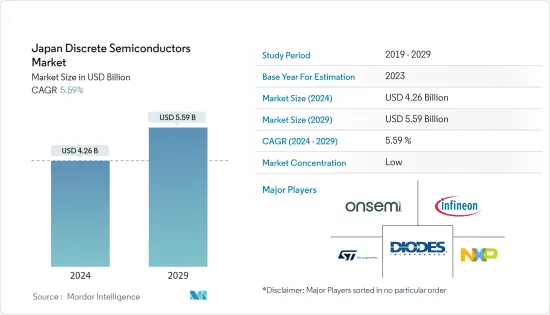

Japan Discrete Semiconductors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Japan Discrete Semiconductors Market size is estimated at USD 4.26 billion in 2024, and is expected to reach USD 5.59 billion by 2029, growing at a CAGR of 5.59% during the forecast period (2024-2029).

Discrete semiconductors are crucial in technological advancements, especially in automotive electronics, renewable energy systems, and consumer electronics. Emerging trends like IoT, electric vehicles, and smart devices fuel the demand for specialized discrete semiconductors. Moreover, given that manufacturers of these semiconductors have a global presence, they often source materials and conduct sales in various currencies. Consequently, fluctuations in exchange rates can significantly affect their profitability and competitive edge.

Key Highlights

- Discrete semiconductors, or discrete components or devices, are individual electronic components designed to carry out specific functions within electronic circuits that operate independently, without integration. Common examples of discrete semiconductors include diodes, transistors, and thyristors. These components are typically housed in packages featuring two or more leads (pins) for circuit connections. Discrete semiconductors find extensive applications across electronics, from power supplies and amplifiers to control circuits and signal processing.

- Discrete semiconductors provide significant advantages over integrated circuits, including enhanced flexibility, customization, and superior power handling capabilities. They enable designers to precisely control circuit design and performance precisely, accommodating higher voltage and current levels. However, discrete components may necessitate more board space and additional assembly steps compared to integrated circuits.

- Furthermore, fluctuations in commodity prices, particularly in raw materials like metals, silicon, and rare earth elements, directly influence the manufacturing costs of discrete semiconductors. These fluctuations can significantly impact profit margins and necessitate adjustments in pricing strategies.

- Efficient power management is one of the significant driving factors in discrete semiconductors. Advanced system architectures are enhancing the efficiency of AC-DC power adapters while reducing their size and component count. Furthermore, updated power-over-ethernet (PoE) standards now support higher power transfers, facilitating the development of innovative devices such as connected lighting.

- Wearable devices, from their fundamental physics to the end-user experience, are crucial in driving consumer adoption. Discrete semiconductor companies can benefit significantly by closely monitoring market trends and challenges during product design, ensuring they maintain a competitive edge. The adoption of semiconductors with enhanced mobility and critical breakdown fields, particularly Silicon Carbide (SiC), is gaining traction. This trend is especially notable in the transistor range and extends to power electronics devices, including Schottky barrier diodes (SBDs), junction field effect transistors (JFETs), and MOSFET transistors.

- Geopolitical challenges, including the Russian invasion of Ukraine, China-US competition, elections, and the war in Israel, significantly impact the global supply chain, especially critical raw materials vital for traditional industries, defense, high-tech sectors, aerospace, and green energy. The Russia-Ukraine war and economic slowdown caused significant disruption in the semiconductor industry. The increased inflation and interest rates reduced consumer spending, hampered the industry's demand, and led to slow growth in the discrete semiconductor market.

Japan Discrete Semiconductors Market Trends

Power Transistors are Expected to Hold a Significant Market Share

- MOSFETs are semiconductor devices used primarily for switching and amplifying electronic signals in various applications. They belong to the family of field-effect transistors (FETs) and are known for their ability for controlling the flow of current between the two terminals using an electric field. They function at low voltages while providing quick switching and maximum efficiency.

- The power loss in conventional power amplifiers creates demand for RF high-power MOSFET modules that offer a built-in input or output impedance-matching circuit and verified output power performance. Key vendors, such as Mitsubishi Electric, plan to expand the frequency range by launching a 900 MHz module equipped with the new MOSFET in the coming year. According to the company, the model with 50 W power output in the 763 MHz to 870 MHz band and a total efficiency of 40% is projected to help reduce power consumption and increase radio communication range.

- The electronics industry is witnessing a surge in the demand for different electronic devices such as smartphones, tablets, laptops, smart wearables, and IoT devices. These devices require power transistors for various functions. The expanding consumer base and the continuous introduction of new electronic devices drive the demand for power transistors.

- The consumer electronic segment would contribute significantly to the market's growth, supported by the country's large manufacturing landscape and the established consumer electronic companies, including Sony and Panasonic, among others. This would fuel the demand for discrete semiconductor growth in the manufacturing of electronic components used in the consumer electronic segments, which would drive the market growth in Japan.

- Furthermore, in 2023, the electronics industry in Japan witnessed electronic components and devices contributing to a total production value of approximately JPY 6.97 trillion (USD 0.497 trillion), as reported by METI (Japan). The overall production value of the Japanese electronics industry during that period reached around JPY 10.7 trillion (USD 0.076 trillion).

Automotive Industry is Expected to Have a Significant Market Growth

- Discrete semiconductors, tailored for distinct electronic functions and inseparable, are pivotal in transforming automotive electronics. Unlike integrated circuits (ICs), which combine functions, discrete semiconductors, like diodes, transistors, and thyristors, operate autonomously, bolstering automotive capabilities, safety, and connectivity. This shift heralds a new age of technological progress, elevating benchmarks for automotive performance and features.

- Automotive demands are primarily fueling the market for discrete components, particularly power transistors and rectifiers. While traditional vehicles have relied on 12-V battery systems for decades, they are now struggling to support the increased electronic demands of modern cars, highlighting the necessity for more energy-efficient solutions.

- By 2050, the Japanese government has set a target to have all newly sold cars in Japan be electric or hybrid. The country intends to provide subsidies to the private sector to expedite the advancement of batteries and motors for electric-powered vehicles. In an effort to decrease its carbon emissions, the Government of Japan is actively promoting the use of electric vehicles (EVs), leading to significant investments in EV infrastructure development. As a result of government subsidies for EV buyers, Japan has experienced a surge in the number of EV charging stations to accommodate the growing number of electric vehicles.

- Moreover, as per the data released by the Japan Automobile Dealers Association and the Japan Light Motor Vehicle and Motorcycle Association, the year 2023 witnessed the sale of 43,991 standard-size electric vehicles (EVs) and 44,544 electric variants of Japan's renowned lightweight keiminicars.

Japan Discrete Semiconductors Industry Overview

The Japan Discrete Semiconductors Market is consolidated and features key players like STMicroelectronics, Infineon Technologies, NXP Semiconductor, and Diodes Incorporated, among others. Market participants strategically leverage partnerships and acquisitions to bolster their product portfolios and establish a sustainable competitive edge.

- June 2024: Mitsubishi Electric Corporation has announced plans to introduce a web-based service. This service will offer crucial data on the design and validation of the new inverter. The inverter is distinctive, featuring a module housing three LV100 insulated gate bipolar transistors (IGBTs). The primary goal is to assist customers in expediting the development of high-power inverters, specifically for applications like photovoltaic power-generation systems. Notably, the prototype inverter boasts a module that houses three parallel LV100 industrial IGBTs, all within a compact 100mm x 140mm frame, a standard size for high-power inverter systems.

- March 2024: Infineon Technologies introduced its latest product, the IAUCN08S7N013, marking the debut of its new OptiMOS 7 80 V power MOSFET technology. This new offering boasts a notable uptick in power density and comes housed in the resilient and high-current SSO8 5 x 6 mm2 SMD package. Designed for the burgeoning 48 V board net applications, the OptiMOS 7 80 V is primed for the automotive sector. It's engineered to meet the exacting standards of automotive DC-DC converters in EVs, 48 V motor control - including applications like electric power steering (EPS), 48 V battery switches, and electric two- and three-wheelers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for High-energy and Power-efficient Devices in the Automotive and Electronics Segment

- 5.1.2 Increasing Demand for Green Energy Power Generation Drives the Market

- 5.2 Market Challenges

- 5.2.1 Rising Demand for Integrated Circuits

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistor

- 6.1.3 Power Transistor

- 6.1.3.1 MOSFET Power Transistor

- 6.1.3.2 IGBT Power Transistor

- 6.1.3.3 Other Power Transistor

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Communication

- 6.2.4 Industrial

- 6.2.5 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 On Semiconductor Corporation

- 7.1.2 Infineon Technologies AG

- 7.1.3 STMicroelectronics NV

- 7.1.4 NXP Semiconductors NV

- 7.1.5 Diodes Incorporated

- 7.1.6 Toshiba Electronic Devices & Storage Corporation

- 7.1.7 ABB Ltd.

- 7.1.8 Nexperia BV

- 7.1.9 Semikron Danfoss Holding A/S (Danfoss A/S)

- 7.1.10 Eaton Corporation PLC

- 7.1.11 Hitachi Energy Ltd. (Hitachi Ltd.)

- 7.1.12 Mitsubishi Electric Corp.

- 7.1.13 Fuji Electric Co Ltd

- 7.1.14 Analog Devices, Inc.

- 7.1.15 Vishay Intertechnology Inc.

- 7.1.16 Renesas Electronics Corporation

- 7.1.17 ROHM Co. Ltd

- 7.1.18 Microchip Technology

- 7.1.19 Qorvo Inc.

- 7.1.20 Wolfspeed Inc.

- 7.1.21 Texas Instruments Inc.

- 7.1.22 Littelfuse Inc

- 7.1.23 WeEn Semiconductors

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET